Accessing working capital solutions is crucial for growth corporates — often referred to as middle market firms — around the world.

However, the choices available to companies vary depending on their geographical location.

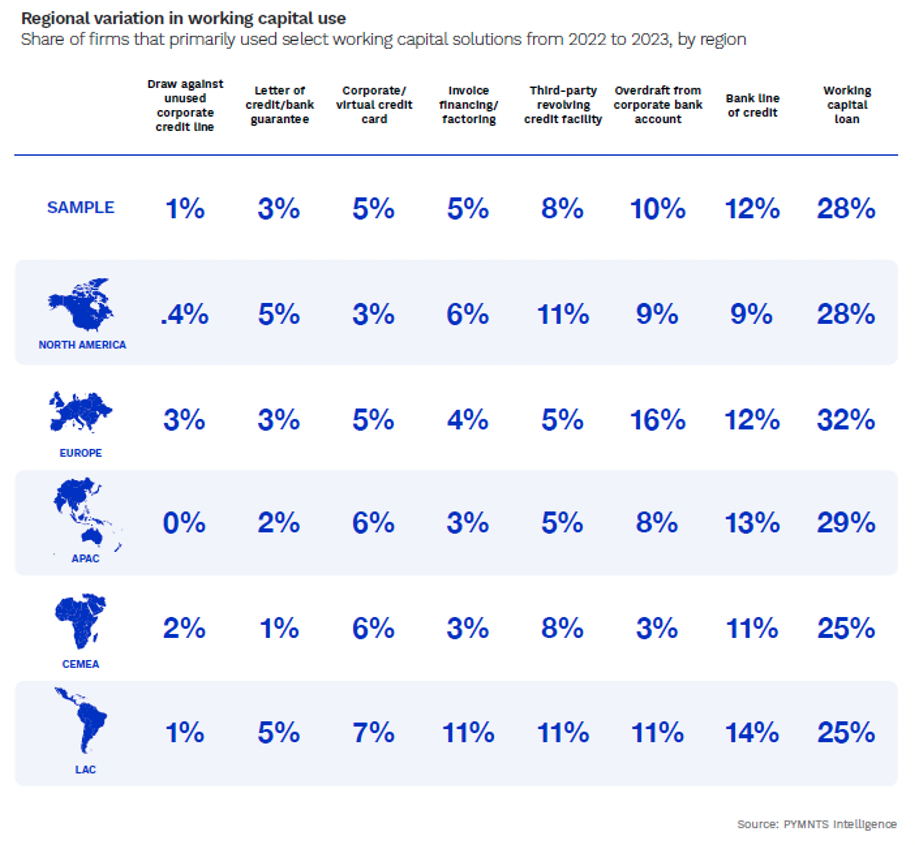

In Europe, for example, working capital loans and overdrafts from corporate bank accounts are the go-to options for nearly 50% of firms. Despite being potentially expensive, these traditional banking products remain popular due to their accessibility and familiarity among European businesses.

In contrast, growth corporates in Latin America and the Caribbean (LAC) rely more on trade finance instruments such as letters of credit and invoice factoring as their primary working capital solutions. Letters of credit assure both buyers and sellers in international trade transactions, while invoice factoring allows companies to access immediate funds by selling their accounts receivable at a discount.

These are some of the findings detailed in the study “The 2023-2024 Growth Corporates Working Capital Index,” a PYMNTS Intelligence and Visa collaboration. The study examined the business conditions and working capital requirements of over 870 chief financial officers and treasurers across five industry segments, five global regions and 23 countries.

The study revealed that the choice of working capital solutions also varies based on the size of the companies. In Europe, firms generating annual revenues between $250 million and $750 million tend to heavily rely on working capital loans. Meanwhile, European companies in the $750 million to $1 billion revenue bracket prefer bank lines of credit, overdrafts and corporate or virtual card solutions, which provide more flexibility and convenience for their specific needs.

In LAC, companies in the $50 million to $250 million revenue range have the highest utilization of bank lines of credit, invoice financing/factoring and third-party revolving credit facilities, which enable these companies to bridge their working capital gaps and maintain their operations.

Overall, the regional differences in working capital solutions for growth corporates can be attributed to various factors in banking systems, regulatory environments and the availability of alternative financing options. Additionally, cultural and historical factors may also influence the preferences of businesses in different regions.

As a result, growth corporates must understand these regional differences in working capital solutions to effectively manage their cash flow needs. For instance, companies expanding into new markets should consider the local financial landscape and explore the available financing options that best suit their specific requirements. By doing so, they can optimize their working capital management and ensure sustainable growth on a global scale.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More