Embedded lending tools enable potential borrowers to apply for credit directly from the merchant or provider’s platform — often while paying for a product or a service. For instance, while finalizing a purchase, a shopper can be prompted to apply for a new credit card or pay via buy now, pay later (BNPL) installments. If the borrower takes advantage of the offer, they can even use the credit for their purchase.

And although embedded lending comes in many flavors, PYMNTS Intelligence data shows that — worldwide — only about half of consumers are happy with the availability of the embedded lending options they now encounter.

That’s is just one takeaway revealed in PYMNTS Intelligence’s “The Embedded Lending Opportunity,” which was commissioned by Visa and surveyed more than 8,300 consumers in six different countries to explore consumer sentiment around embedded borrowing.

Lenders in both developed and emerging markets currently offer a wide range of embedded lending products, yet we found that a high percentage of consumers — particularly those most in need of flexible lending options — say the variety of financing options they see fall short of their expectations.

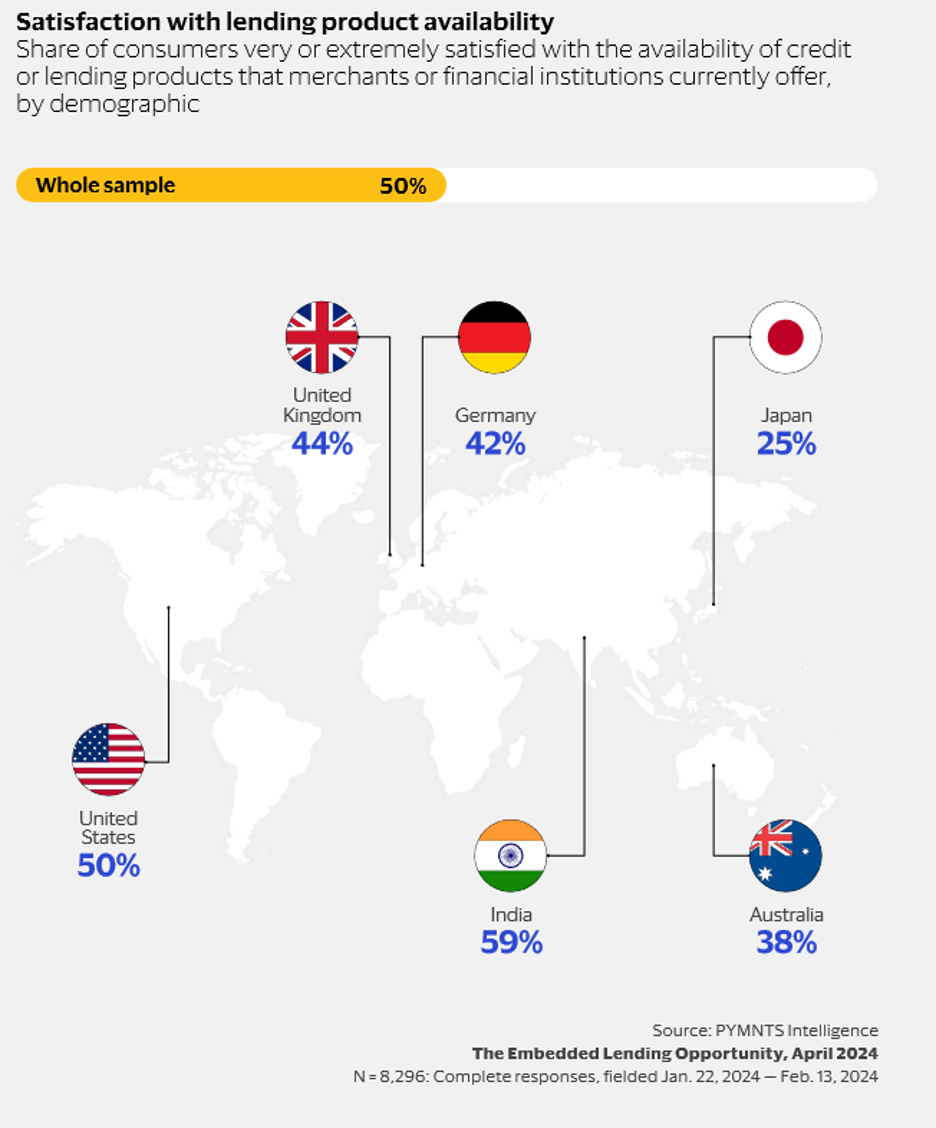

We surveyed consumers in Australia, Germany, India, Japan, the United Kingdom and the U.S., and only 50% said they are highly satisfied with the availability of the embedded lending offers that come their way.

As the accompanying figure illustrates, while nearly 6 in 10 shoppers in India are pleased with the embedded offers they encounter when making a purchase, that’s true for less than half of those in the U.K. and Germany. Meanwhile, only 38% of shoppers in Australia and 25% of those in Japan express enthusiasm for availability of the borrowing offers they encounter when shopping.

Why are consumers so dissatisfied with the current crop of embedded lending options? Their reasons vary depending on age and locations, but several patterns are evident. For instance, 37% of embedded lending users say the low credit limits are a pain point. Another 21% say the fees and interest rates are too high.

This could be seen as bad news for merchants and lenders, because PYMNTS Intelligence determined there is a significant unmet demand in the consumer credit market that embedded lending could address. Fifty-six percent of Gen Z respondents and 55% of millennials say they would be highly interested in using embedded lending under the right circumstances.

PYMNTS Intelligence’s analysis determined that consumers with frequent cash flow gaps across income groups — those with the greatest need for credit — are particularly underserved, and better embedded lending availability can offer significant potential to meet their needs.