Nonrecurring or ad hoc payments remain a significant part of the monthly revenues of small to mid-sized businesses (SMBs). One way that SMBs streamline the accounts receivable (AR) process is with the help of instant payment methods. Instant payments, which provide quick access to the funds essential to running businesses, are especially helpful to the smallest or micro SMBs relying primarily on ad hoc receipts.

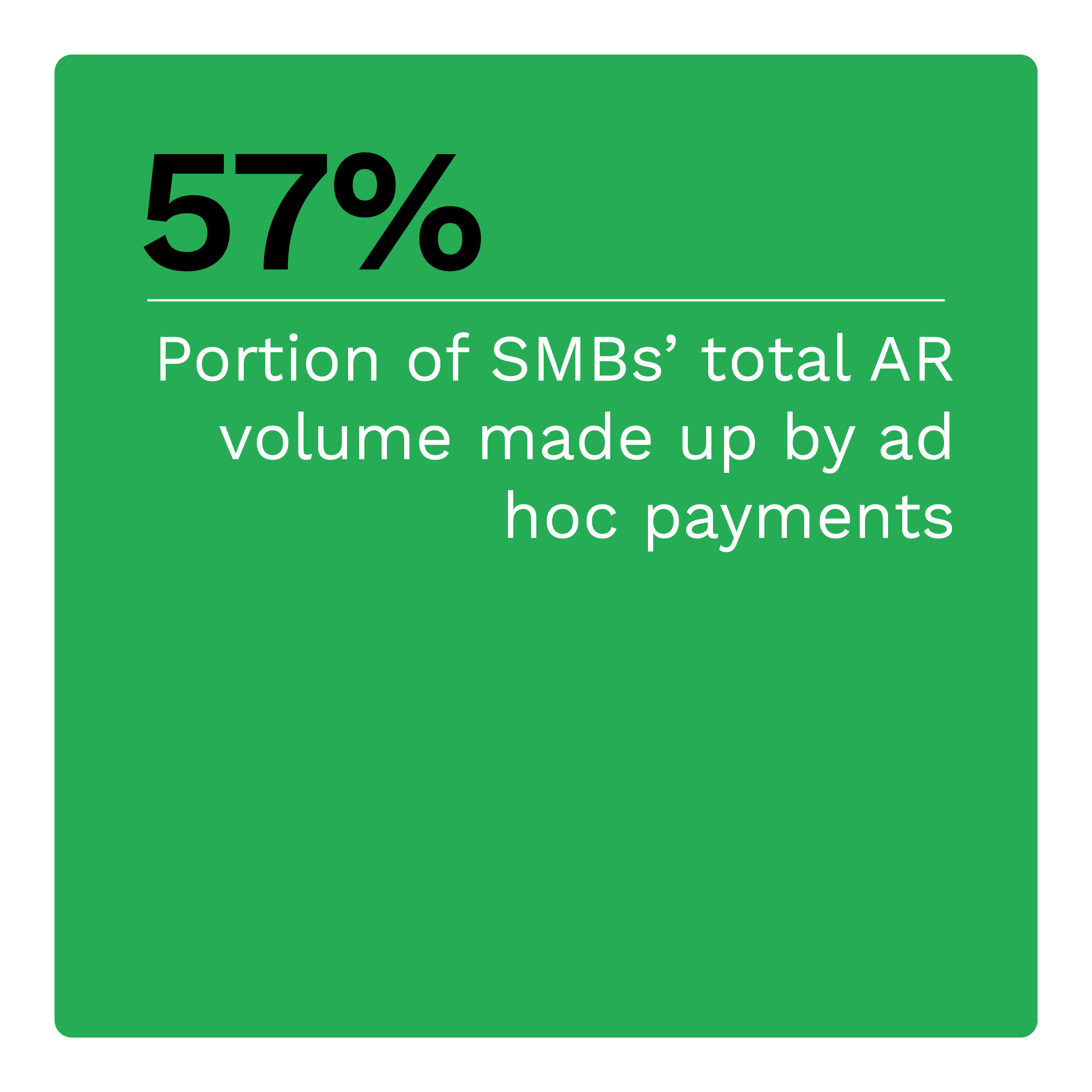

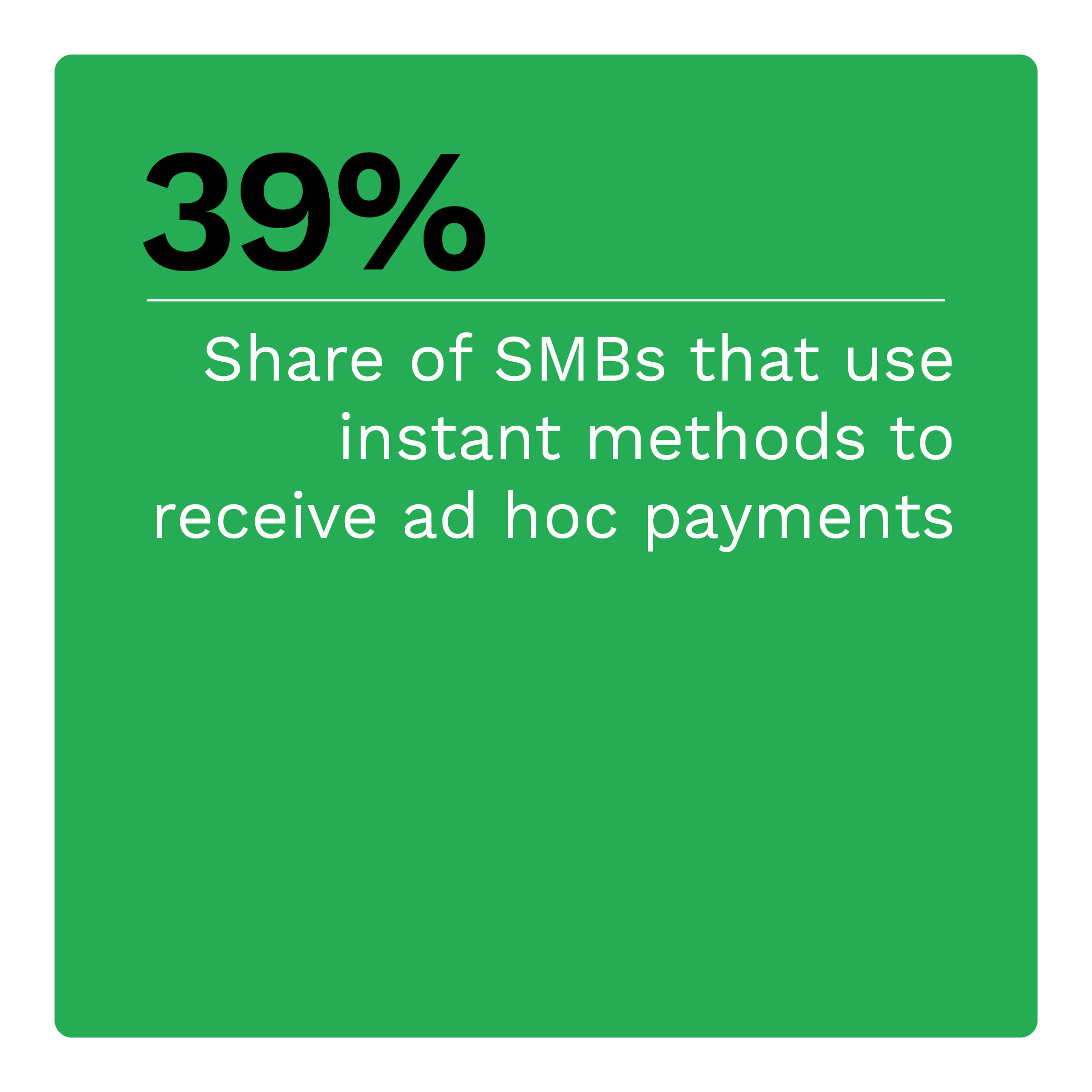

The cost of receiving these payments instantly remains a deterrent to businesses that could benefit from them the most. These payments account for most SMBs’ AR volumes, but SMBs choose instant for 39% of all ad hoc payments received. The smallest SMBs — those annually generating less than $100,000 in revenue — have decreased instant payment use since September 2023. This is most likely due to cost. Small SMBs that use instant methods report that they pay the highest fees.

These are some of the findings detailed in “How Instant Ad Hoc Payment Costs Impact Small SMBs,” a PYMNTS Intelligence and Ingo Payments collaboration. This report is based on a survey of 405 SMB receivers generating less than $25 million in annual revenue across the United States conducted between Dec. 29, 2023, and Jan. 18, 2024. The report examines SMBs’ reliance on ad hoc payments, the challenges they face when processing AR and how instant payment methods can help SMBs manage their cash flows and set them up for success.

Other findings from the report include:

The primary instant method for most payments of this type is instantly to bank accounts via a debit card. However, SMBs generating less than $100,000 in annual revenue receive 57% of their instant ad hoc payments through Zelle, an indication that their AR processes are less capable of receiving via push-to-card and other instant options. The report explores trends in SMBs using Zelle, push-to-card payments, the RTP® network and other instant methods.

The cost of instant methods for these payments remains higher than most options for SMBs, even though costs have begun to come down. The smallest SMBs pay $11.70 per instant transaction, disproportionately more than the average of $7.90 per transaction among all payment types. One explanation is that many SMBs, particularly the smallest ones, rely on manual means to process ad hoc payments. The report delves into how manual AR processes and the costs of instant can increase poor payment timing, which 1 in 4 SMBs cite as their biggest challenge.

The cost of instant methods for these payments remains higher than most options for SMBs, even though costs have begun to come down. The smallest SMBs pay $11.70 per instant transaction, disproportionately more than the average of $7.90 per transaction among all payment types. One explanation is that many SMBs, particularly the smallest ones, rely on manual means to process ad hoc payments. The report delves into how manual AR processes and the costs of instant can increase poor payment timing, which 1 in 4 SMBs cite as their biggest challenge.

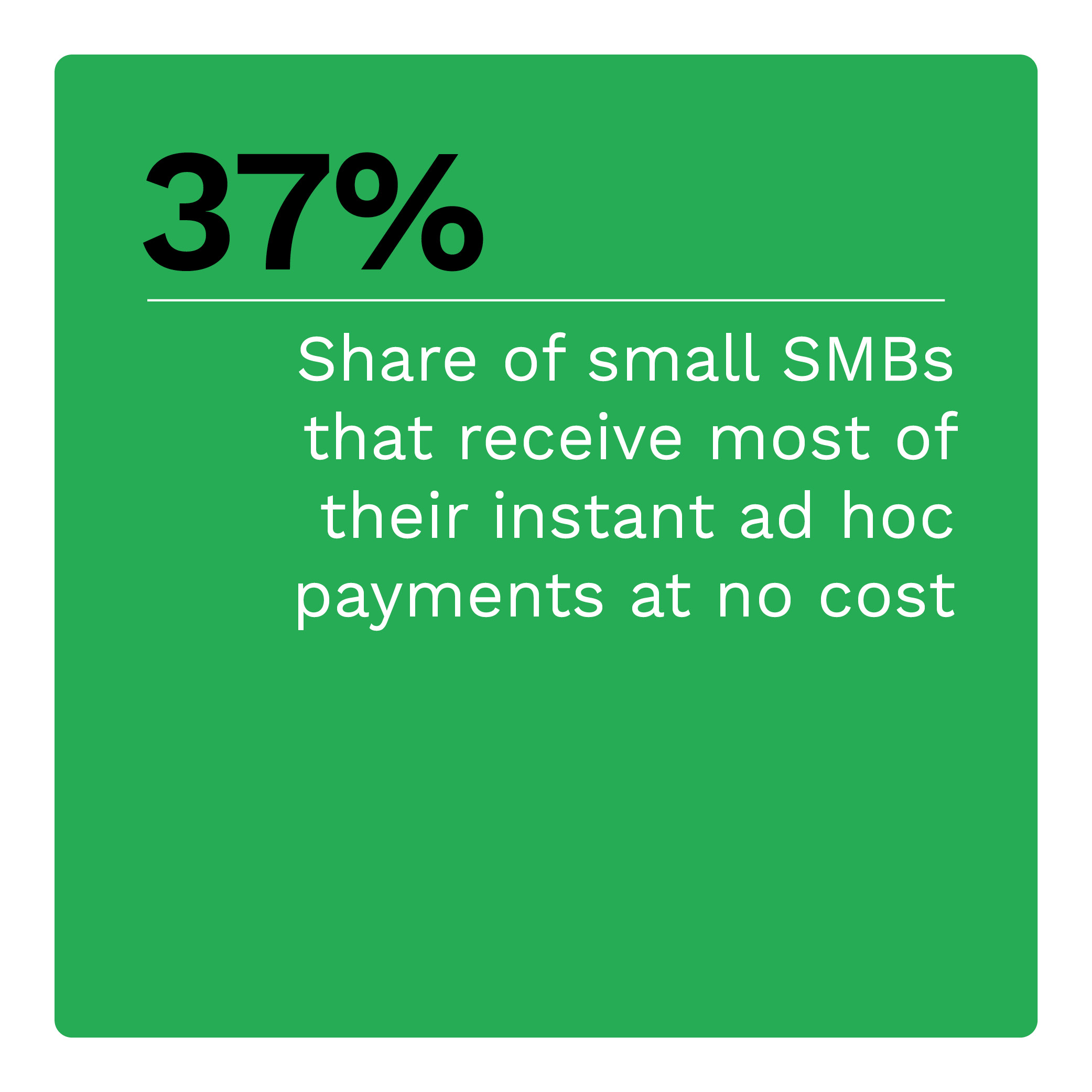

Receiving instant ad hoc payments at no cost is an attractive option for SMBs. However, just 19% of SMBs report receiving these payments via instant methods for free, down from 29% in September 2023. This may help explain why the smallest SMBs reported receiving fewer of these payments via instant methods than in September. Nonetheless, more than half of SMBs are willing to pay a fee to receive instant payments. The report details which SMBs find fixed fees appealing and which prefer percentage fees.

The cost of receiving instant ad hoc payments remains a challenge for the smallest SMBs. Reducing instant payment costs by improving AR systems is one key to boosting instant use among these SMBs. Senders who can offer the right fee structure may have a competitive advantage. Download the report to learn more about trends in SMBs’ use of instant methods to receive ad hoc payments.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More