Many middle-market businesses operate in a world of heightened uncertainty, but PYMNTS Intelligence data found that payment solutions such as virtual cards can help mitigate that uncertainty.

This is one key takeaway from PYMNTS Intelligence’s recently released edition of the 2024 Certainty Project Report, “Optimizing AR to Mitigate Uncertainty for Middle-Market Businesses.” The ongoing series looks at trends and sentiment shared by executives of middle-market firms and small enterprise companies (between $100 million and $1 billion in annual revenues). Included in the new report is an examination of virtual cards and how they can help accounts receivable (AR) teams manage uncertainty.

For most middle-market companies, managing AR is a balancing act between efficiency and security. Efficiency prioritizes streamlining invoice processing and collection to accelerate cash flow; security, meanwhile, focuses on safeguarding against non-payments, fraud and data breaches.

For smaller middle-market firms (those with revenues between $100 million and $250 million), this balancing act often tilts towards managing uncertainty in the payment process. Sixty percent of smaller middle-market firms report they encounter significant challenges in managing payments, while only two in five firms with revenues in the $750 million to $1 billion bracket face similar issues.

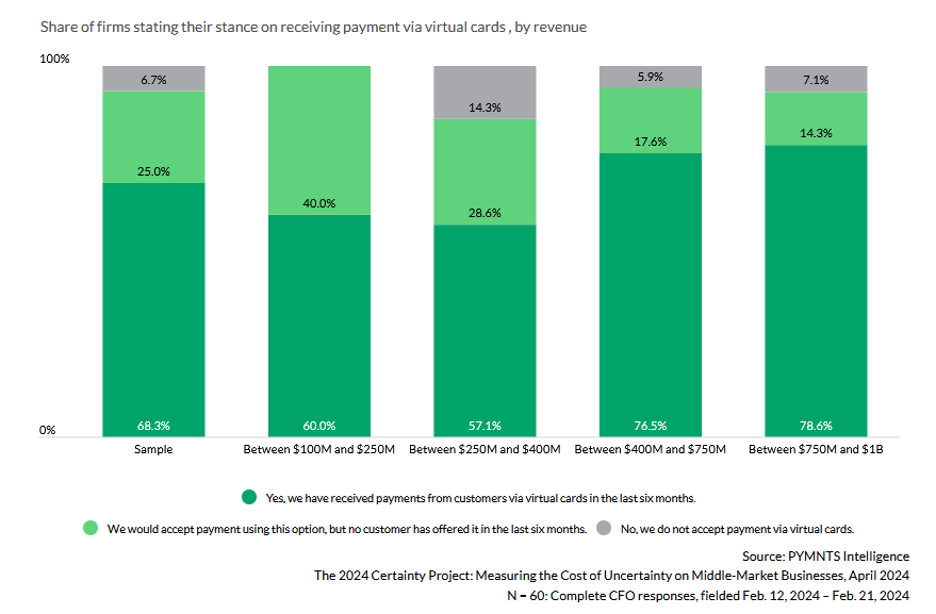

Embracing new payment technologies, such as virtual cards, could help mitigate that AR uncertainty. However, larger firms appear to be more comfortable using virtual cards, with 79% of them receiving payments through virtual cards, compared to 60% of smaller firms.

PYMNTS Intelligence also determined that firms not using virtual cards also happen to experience an average revenue loss of 4.6% from payment uncertainties. (Larger, more financially robust firms report a lower impact.)

Because uncertainty impacts smaller middle-market firms in a bigger way, those smaller organizations may also stand to see the most benefits in integrating advanced payment solutions — such as virtual cards — into their financial operations.

But, as the chart above — which reflects exclusive PYMNTS Intelligence data not included in our final report — shows, roughly three in five smaller middle-market firms received payments from customers through virtual cards in the last six months, while roughly four in five larger middle-market firms received payments that way.

Why the disconnect? Why aren’t more smaller middle-market firms using virtual cards?

One answer could be that it’s not up to them. As we found in compiling our report, often AR executives — especially those in more modest-sized organizations — may not always have the final say in how the firm gets paid. Forty-seven percent of smaller revenue middle-market firms said their buyers determine payment terms most or all the time, while in larger revenue middle-market firms, 36% said their buyers make that determination.

That’s unfortunate for smaller firms, because, as PYMNTS Intelligence found, receiving AR payments through virtual card technology can help improve efficiencies and reduce revenue losses. Smaller middle-market firms seeking a competitive edge may want to talk to their buyers about the advantages of deploying virtual cards.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More