In life, context matters. Say “I love you,” and the tone of voice may give the context of — to quote Marvin Gaye’s lyrics — “What’s Goin’ On.” Are the words honeyed and romantic, whispered in the recipient’s ear while swaying on the dance floor on a date? Maybe dripping with sarcasm, and no slight tinge of venom, after driving around lost for four hours while the gas gauge is on empty?

Same words, different meaning — as well as different urgencies and results. In the first case, a kiss to seal the relationship — in the second, a kiss-off.

If context gives us direction and helps us decide what comes next, depending on the circumstances that surround information, data or demands, then why should it be any different for payments in general — banks in particular?

Thus, giving context to payments helps make intelligence and data actionable. In a world of 24/7 commerce that is getting ever global, especially in B2B payments, speed matters — but so does accuracy. Context gives rise to that speed and accuracy. It can help firms establish a hierarchy of urgency, funneling transactions with an eye on destination, payment type and timing. Artificial intelligence (AI) and machine learning are the means to this end.

In an interview with Michel Jacobs, EVP and head of digital payments at Intellect Global Transaction Banking (iGTB), the executive noted to Karen Webster that for banks, marked as they are by legacy systems, the goal is to “move at the speed of commerce.” However, that is no easy task when grappling with back-end systems that are, in some cases, decades older than the executives and IT professionals responsible for making sure commerce is kept humming in the first place.

The discussion between Jacobs and Webster was part of an ongoing series focused on contextual banking. One common theme: The overarching question that dominates transactions need not be “how” or “what,” but “why.”

The “why” of transactions is granular and moves beyond names and numbers. The “why” embraces whether a payment is destined for accounts payable or receivable, to offer context. The “why” can pay dividends, improving the efficiencies of payment settlement and transparency.

Beyond The “Rip And Replace” Mindset

More on the “why” in a minute. One important point, as underscored by Jacobs: All of this can take place without requiring banks to rip and replace their aforementioned legacy systems, or requiring them to embark on IT deep dives that transform the nuts and bolts of operations, but over the course of 16 months when the commerce is constantly shifting.

Speaking of his own firm, Jacobs said that iGTB is creating a powerful engine — the Contextual Banking Experience — that connects to the core banking platform, rests on top of already extant functions (by dint of RESTful APIs) and brings banks closer to moving at the speed of commerce. But an important distinction must be made here, one that cleaves consumer transactions from corporate ones.

“If you truly think about where the future of a retail bank lies, it is fairly obvious that their aim has to be to become an integral part of a consumer lifestyle,” he told Webster. “[And] if they don’t, at best, they’ll have margin compression. At worst, they will be disintermediated.”

The pressure and opportunity, he said, lies equally with corporate business, where legacy systems dominate and transactions are relatively much more complicated. At the same time, competition for corporate payments business has become heated enough that just offering wire services and the like is no advantage — now, it’s merely table stakes. Done right, with the aid of context, banks can become what Jacobs termed “an integral part of the corporate supply chain.”

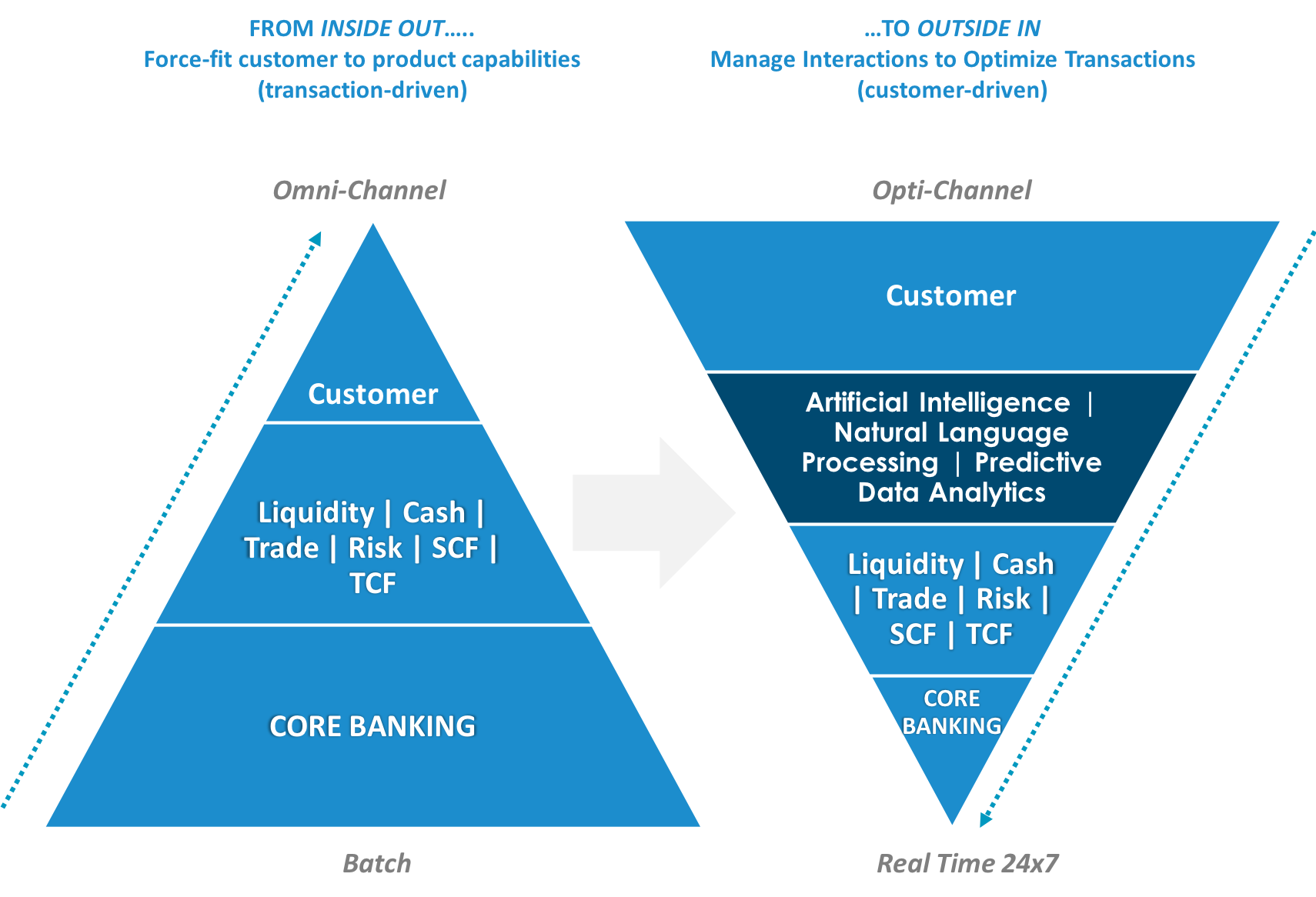

Against that mindset, where the interaction is key, iGTB has inverted what Jacobs offered as an illustrative triangle, one where the bottom of the triangle has traditionally been dominated by the core banking platform, channels and user interface. Up top, at the apex, the particulars of the transaction itself resides, a less dominant consideration. Now, that model gets flipped a bit: iGTB sits in the middle with its platform on top of the core, and the context of the payment, now at the top of the inverted triangle, occupies top of mind and technology.

“What we did is create a whole new architectural framework that we call the interaction management layer, that can manage and understand the intent and context of each and every interaction, and this is then used to optimize and maximize the execution of the associated transaction path,” Jacobs explained.

The interaction layer, he stated, is where the data and context on transactions are stored, and where the analytics happen — during the interaction, not afterwards. A real-time database is leveraged and allows banks to do in-line analytics, reporting and efficient tracking. Jacobs noted that tracking ability is crucial, as “the biggest issue that people, for example, have with wires, besides cost, is that it’s a black hole for today. You don’t know the status of a payment until you either get an error or confirmation days later.”

Not Just “Where,” But “Why”

Think, then, of two boxes of payments. With the old way of transacting, sending these payments would just route them over existing rails, with nary a thought of context. Add machine learning and AI into the mix; one can dig a bit and find that one box has fresh flowers on their way to Amsterdam, while the other box harbors scrap metal. The former needs overnight shipping and a cool container (in other words, urgency is the mindset with this payment), while the scrap metal can wait around a bit before getting sent off. With this level of insight, firms can take advantage of timing, getting a boost to cash flow from prudent matching to interest rates or discounts offered on timely (or early) payments.

Jacobs said that real-time payments means different things to different people. “For banks,” he said, “it’s about day-two exceptions. For compliance guys, it is about Basel III and intraday liquidity.”

The context helps to satisfy the numerous factors or considerations that go into any corporate payment, said Jacobs. The payment needs to be irrevocable. There needs to be an understanding of the bilateral risk of both parties involved in a transaction, as well as an understanding of the business impact of payments — and to understand business impact, there needs to be an understanding of costs tied to overnight settlement.

But to get there, Jacobs said, “the focus needs to be about the interaction, not the transaction.”