There is a better way for banks to help corporations and businesses, including SMEs, to make money — a method that takes advantage of all the benefits of digital technology while working within the limitations of legacy banking systems.

That is among the emerging topics in the payment world, and one of the possibly controversial assertions in a recent interview between Karen Webster and Phil Cantor, executive vice president at Intellect Global Transaction Banking (iGTB), a provider of corporate banking technology.

The interview was a continuation of a recent PYMNTS discussion with iGTB CEO Manish Maakan about the general outlines of “contextual banking.”

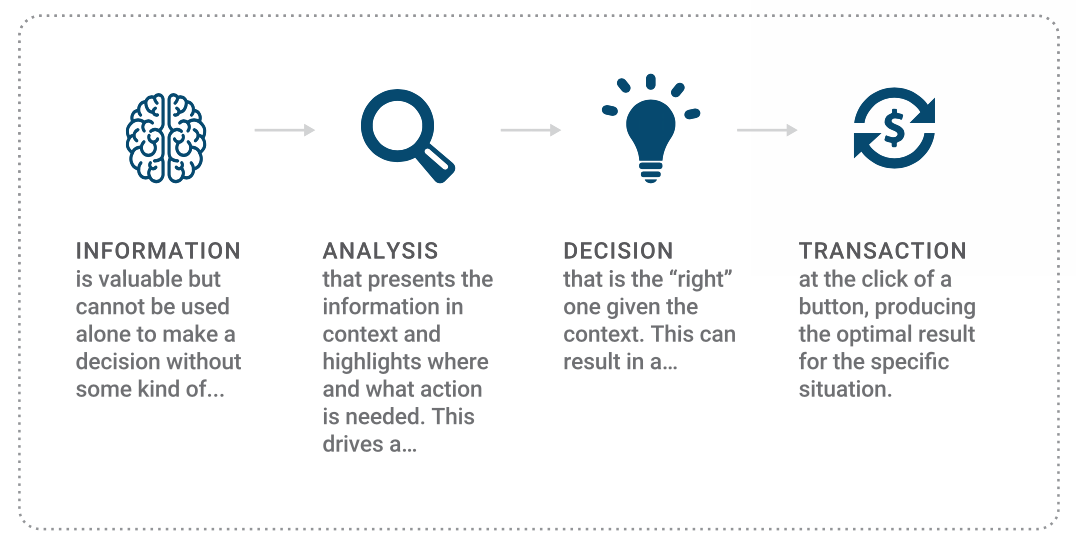

That largely unfamiliar phrase, simply put, refers to using automated processes, data analysis and machine learning to better grasp why, how and when invoice and other B2B transactions are made. This, in turn, leads to supporting more of the real value chain, including the more efficient routing of those payments, which also exploits the advantages of currency fluctuation, settlement discounts and other factors to reduce payment expense.

The Context of Payments

The Context of Payments

Businesses make B2B transactions for a variety of reasons: to pay suppliers for inventory and services, to pay for office and warehouse space, and to pay for workers, utilities, insurance and debt. Paying salaries, for example (100,000+ small, time-critical, beneficiary-hidden payments), has very different parameters from paying for new plants (one large-value, maybe trade-finance-backed, largely time-insensitive payment). These complicated, often heavily manual processes, which involve the headache of reconciling invoices and various accounts, are ill-served by a single “make payment batch” function, and can leave corporate treasurers unsure about the seemingly tiny methods that can bring efficiency — and maybe even revenue opportunities — to that non-stop process.

APIs, machine learning, predictive analytics and other technologies to automate and customize operations for corporate banking and B2B transactions create the “best-next” actions for banking clients, as well as product upsells and cross-sells using business data. That, Cantor said, provides the “context-aware recommendations,” which not only help corporates optimize their cash, but also help the banks to enable the services to drive more bank profit.

The “Why” of B2B Payments

Getting to that idea requires a thinking shift from the “how” of B2B payments (first question: “how do you want to pay – Fedwire, CHIPS, Ripple, etc.”) to the “who” of B2B payments (“who do you want to pay?” – then enter lots of data) to the “what” of B2B payments (“what do you want to pay?” – the invoice has all the data) to the “why” (“why do you want to pay?” – i.e. why now, maybe the big data picture will pick a better date), according to iGTB. Banks already know what their corporate clients are doing with payments, as it’s pretty easy to figure out which supplier is owed money on a certain date, and for what product or service. But going a step further — getting into the “why” — can lead to a better, less expensive and more lucrative payments process.

At the simplest, it means the bank – not the user – makes an informed choice of which payment rail to use (comparing cost and speed, just like Expedia does). For a more complex instance, maybe a business pays an invoice at a certain time that might seem to make immediate sense, such as when the invoice is due, but the bank’s system might advise that the payment would be better made at a different date, perhaps to take advantage of incoming funds, a settlement discount or a maturing investment. According to iGTB, proper deployment of contextual banking technology could help identify such practices and opportunities, and lead to a better return on investment.

Once that “why” is understood and programmed into the payments process (that is, once the context is established), the technology would, ideally, help corporate treasurers, CEOs and other officials to rely on automation and machine learning for payment-related suggestions.

The Past Is the Future

For Cantor, such a context-based B2B payments process would help banks recover value they lost over the decades. During the interview, he painted a picture of a banking industry more trapped in this status quo, with profits assured from their control of the value chain rather than finding ways to better serve corporate customers.

Banks exist, in large part, to encourage wealth creation via the facilitation of trading among businesses, Cantor noted. Banks serve as oil for the gears of any robust economy. According to Cantor, smarter banks are now beginning to refocus on that purpose.

“Historically, banks, with their literal license to print money, made good lip service out of ‘we want to help you,’” he told Webster, expressing skepticism that, at least generally, they were able to do it, or really needed to do it. But APIs, either demanded by corporations or driven by regulations, are forcing banks to compete more in each element of the value chain – and AI is fueling how they do it.

In Cantor’s view, the practice of contextual banking can help financial institutions gain that lost focus, while also ensuring profits for all the parties involved. Gaining — or regaining — the proper focus requires attention to be paid to the “why” of banking transactions, he said.

For instance, contextual banking technology, which employs AI and machine learning, can take the question “Why do you want to pay this invoice?” and turn it into something efficient and lucrative. Why pay this particular bill now instead of, say, waiting a little bit to benefit from possible settlement discounts or currency fluctuations? Why not let the technology analyze various factors to locate advantages tied to interest rates and other parts of the overall financial machine?

“Suddenly,” Cantor said, detailing his vision, “the banking system and its products – not just the account manager – can become an advisor to the client, and help to run the business.”

Corporate Treasurers

The rise of contextual banking could also change the role of the corporate treasurer, he said. People in that position usually spend much of their time reconciling invoices instead of asking themselves, in Cantor’s words, “Why am I having to reconcile so many invoices in the first place?”

The technology of contextual banking could automate much of the invoice reconciliation process, figuring out, based on data and past payments, which invoices get paid from what accounts, to what destination and by which date. That could free up corporate treasurers for more “strategic” work, Cantor said.

There is no question that banks — some more quickly than others — are embracing digital technology, AI and machine learning, as payments across the globe become faster and more complex. However, core banking systems still remain bolted into the daily operations of financial institutions. According to Cantor, contextual banking technology does not necessarily mean those core systems need to be ripped out and replaced.

“We are here to give you things that [go] around the core banking,” he told Webster.

Actionable data about B2B payments will continue to accumulate with the financial institutions that facilitate those transactions, and the banking industry will continue to get more competitive, especially as payment technology continues to develop. Those trends could well provide larger openings for contextual banking in the years to come.