Speaking last week at Vanderbilt University, Hsu said he sees a “blurring of the line between banking and commerce,” which for him brings to mind the events of 1929 and 2008 when similar “blurring” preceded market crashes.

As the transcript from his Feb. 21 presentation suggests, Hsu fears history may be repeating itself.

“Arguably, some FinTechs are already doing this, blurring the line between banks and nonbanks (and raising concerns about level playing fields),” he said. There are FinTechs, he said, that “started off simply facilitating payments,” but now “offer customers the ability to deposit paychecks directly into their accounts, earn yield on the cash held there, and access credit, all with a few clicks of a mouse or taps on a phone.”

Hsu fears that if FinTechs continue to expand their menu of services without proper oversight, it could eventually undermine public confidence.

“From a financial stability perspective, the deposit-taking-like activity warrants the most scrutiny because of the vulnerability it creates to runs,” he said. “Any entity managing money on behalf of customers can face a run if those customers have doubts about the safety of their money.”

Hsu’s concerns are understandable; however, they don’t necessarily align with the current state of bank/FinTech collaboration.

PYMNTS Intelligence found that 89% of bank executives believe partnering with FinTechs is at least “somewhat important” and at least 6 out of 10 financial institutions (FIs) are already doing so.

What’s driving these FinTech collaborations? That’s easy: consumer demand.

Seventy-seven percent of bank executives told PYMNTS Intelligence they feel pressured to work with FinTechs and 76% said they believe working with them is “necessary” to meet customer expectations. As a result, 95% of respondents now leverage FinTech relationships to enhance the digital products they offer.

But meeting customer demands while adhering to the many regulations already in place leaves many FIs executives frustrated.

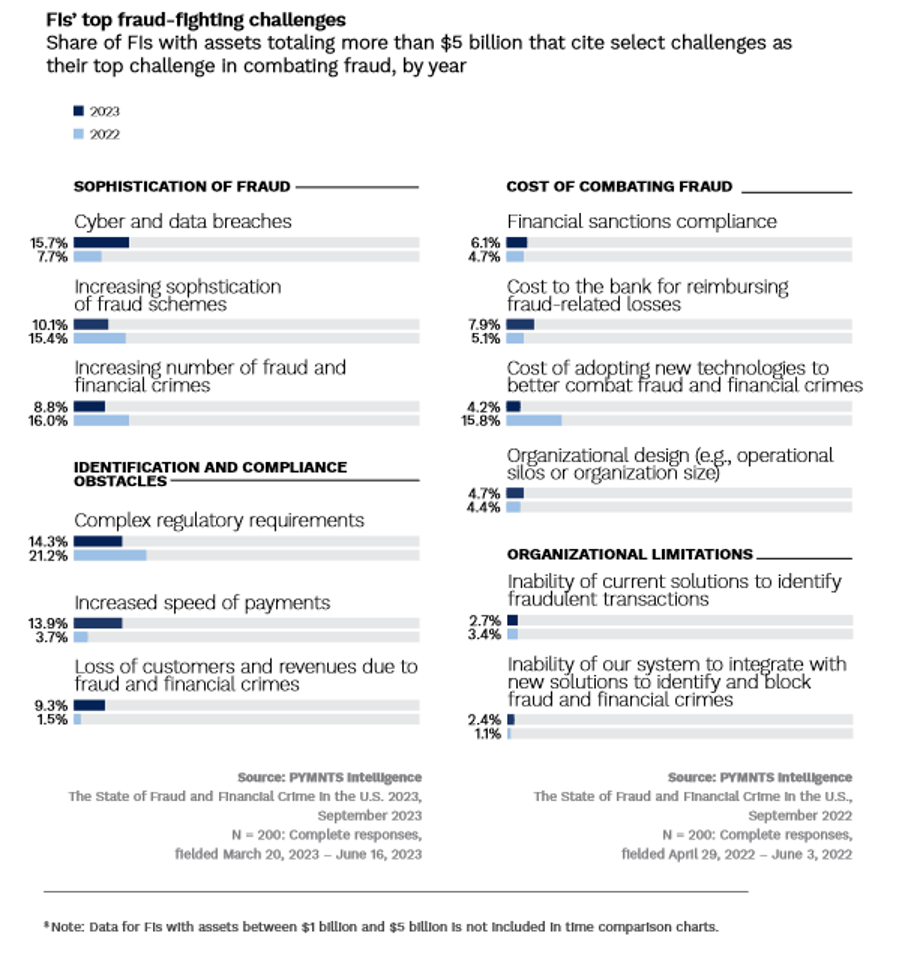

Take for instance, the challenge FIs face as they work to protect their institutions — and their customers — from fraudsters. As PYMNTS Intelligence reported in “The State of Fraud and Financial Crime in the U.S. 2023,” “The battle against rising fraud never ends, and banks of all sizes need more sophisticated tools to win the fight. … [Forty-eight percent] of FIs are either in the process of adding or will add new technology systems in [2024].”

With nearly half of FIs planning to add new fraud-prevention technology this year, one logical question is, who is building the new technology — the FIs or their FinTech partners?

Regardless of whether the technology is built in-house or externally, it is worth noting that nearly 15 percent of bank executives said identifying and complying with existing regulations is an obstacle because those regulations are “too complex.”

None of these findings are intended to downplay Hsu’s concerns, but they do underscore the challenge FIs currently face when navigating existing regulations.

And, as PYMNTS Intelligence reported last June, more regulations are coming as the Consumer Financial Protection Bureau’s (CFPB) proposed open banking framework mandates become finalized — mandates, the article concluded, that are likely to make “bank-FinTech partnerships a necessity.”