Fears of a recession are stressing consumers and complicating banks’ efforts to deliver winning customer service.

More than eight in 10 bank executives, for example, reported that their banks increased their technology budgets over the previous year, with a substantial 63% implementing or upgrading payments capabilities to improve the customer experience. At the same time, most banks seemed to miss the mark on customer satisfaction, according to a J.D. Power survey, with only 44% delivering the personalization their customers desire.

For banks today, customer satisfaction is a moving target, with the line between nice-to-haves and must-haves becoming muddied as financial winds change and digital banking becomes more of an expectation. In times of such rapid evolution, the need for customer-centricity is quickly emerging as the only constant. This month, PYMNTS examines why a customer focus should be the North Star for banks seeking a greater share of consumers’ satisfaction and loyalty.

Improvements in the digital experience are likely to increase customer satisfaction and retention.

Improvements in the digital experience are likely to increase customer satisfaction and retention.

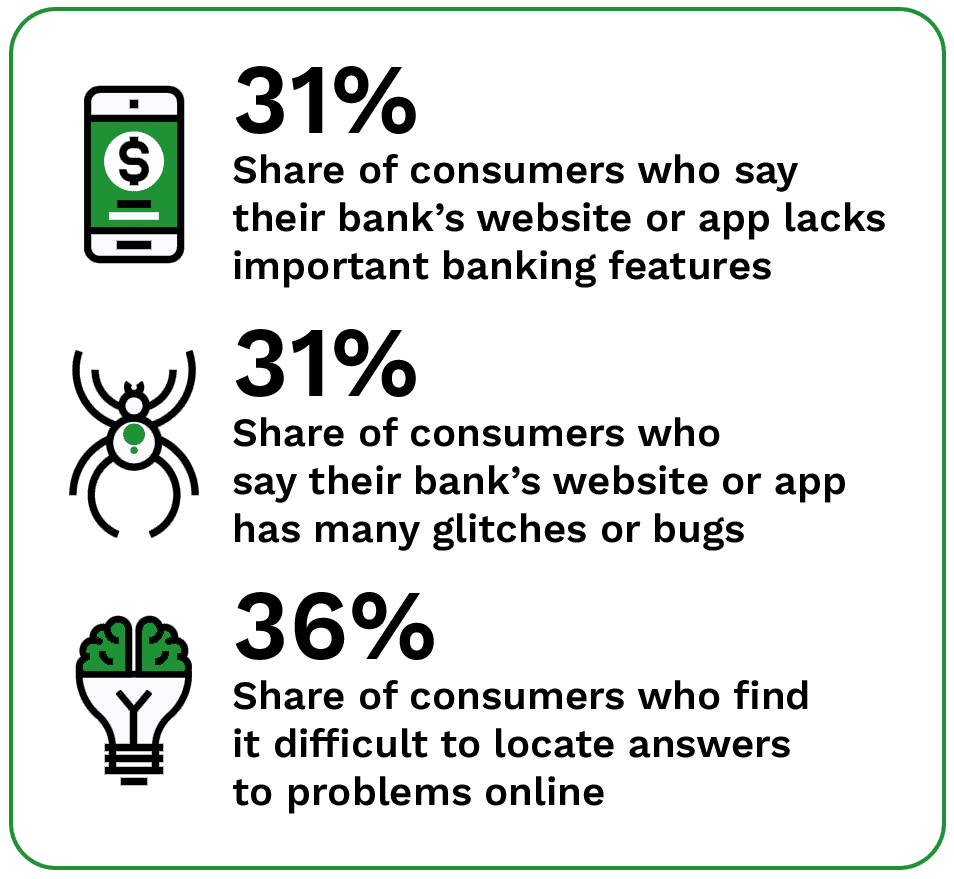

Trends unquestionably demonstrate that consumers want their financial services to be digital. With 23% of customers having moved to a different bank because their primary bank lacked all the banking features they needed, FIs must take stock of how their services might be more up-to-date, personalized or in line with competitors’ offerings. At the same time, some 47% of consumers cited a poor customer service experience or a similar competitor with better service as reasons for closing an account. The lack of availability of all the digital features a customer needs or effective online problem resolution are among the reasons provided by consumers to close an account.

Improved digital experience must follow customers to whatever channels they prefer.

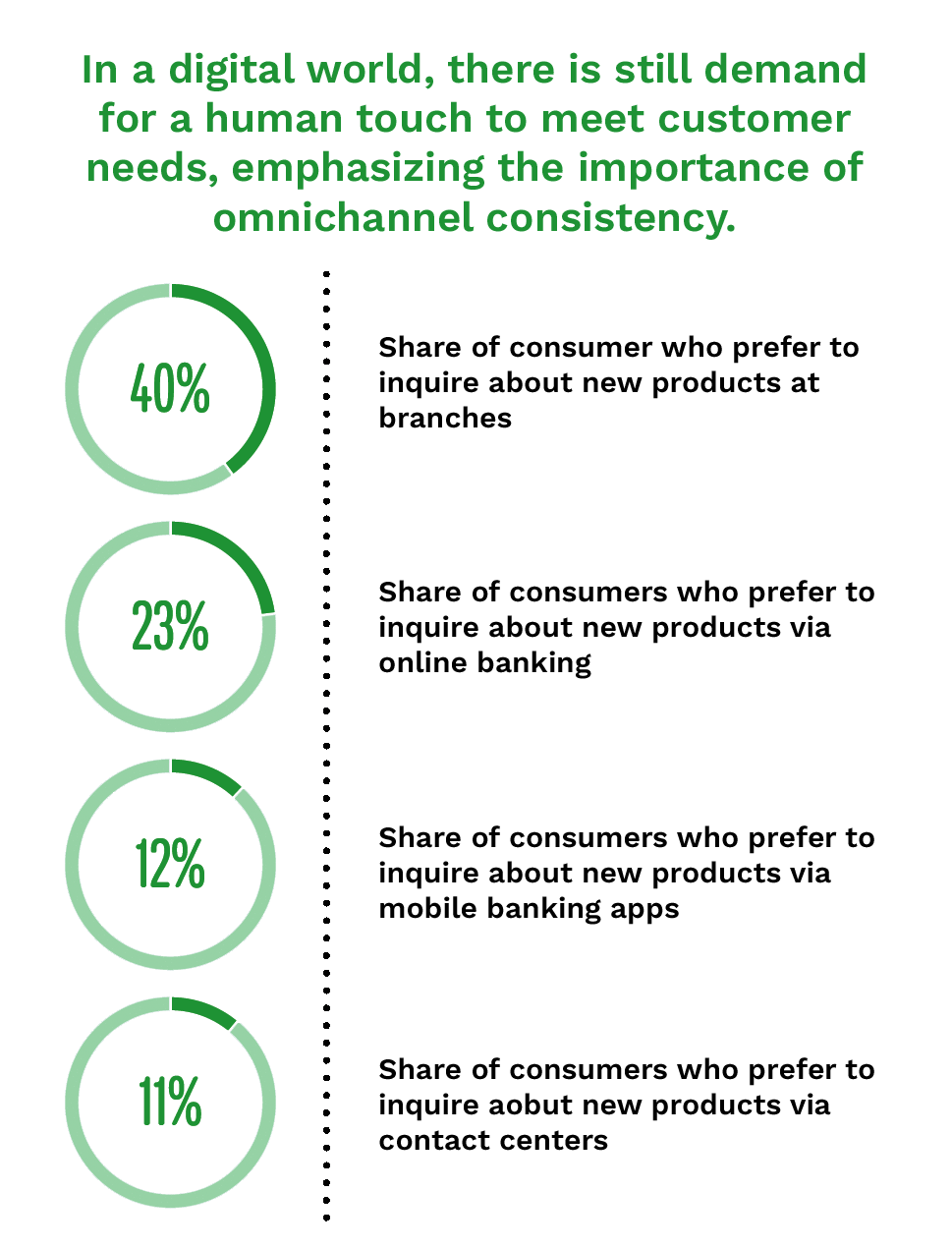

FIs’ digital improvements are a strong pull for the growing number of consumers who prefer online and mobile features, but banks also must provide better and more self-directed customer experiences via technology innovation for the substantial number of consumers who still prefer branches to conduct certain banking activities.

While nearly one in four consumers say they will visit branches fewer times in the future, 82% maintain that local branches in their communities are important. As more customers flock to digital channels, overcoming barriers to technology adoption to achieve an easy, secure and omnichannel experience for wherever they need service is essential for traditional FIs to compete.

Banks must anticipate consumer needs to deliver personalization that resonates.

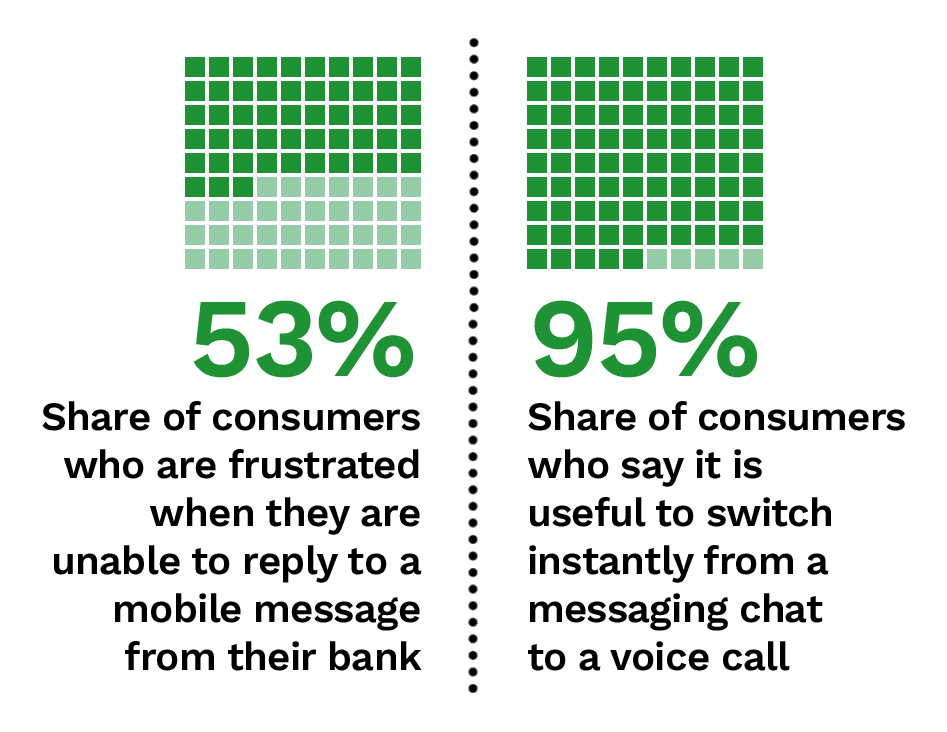

Banking customers are just as clear about their demand for personalization as they are for digital banking. More than nine in 10 customers want personalized financial advice from their banks, but less than three in 10 can say they are receiving it. Customers are seeking two-way digital conversations, rather than one-way notifications. They also want the option to speak to a human when needed — such as being able to switch instantly from a messaging chat to a voice call.

First, banks need to shift their mindset from fixing customer problems to anticipating them. This adjustment is not dependent on the latest technology but instead requires smart use of existing data to deepen customer relationships. Trust is a requirement for customers to take advantage of new digital features and tools and is a key factor in creating positive customer experiences.