More than half of Americans made at least one purchase on Black Friday, according to PYMNTS Intelligence data. However, not all online transactions were likely successful. According to PYMNTS Intelligence data, nearly 1 in 10 online transactions failed in the last 12 months, which means that on this Black Friday, chances are a good number of online transactions were not completed, resulting in a big portion of missed sales.

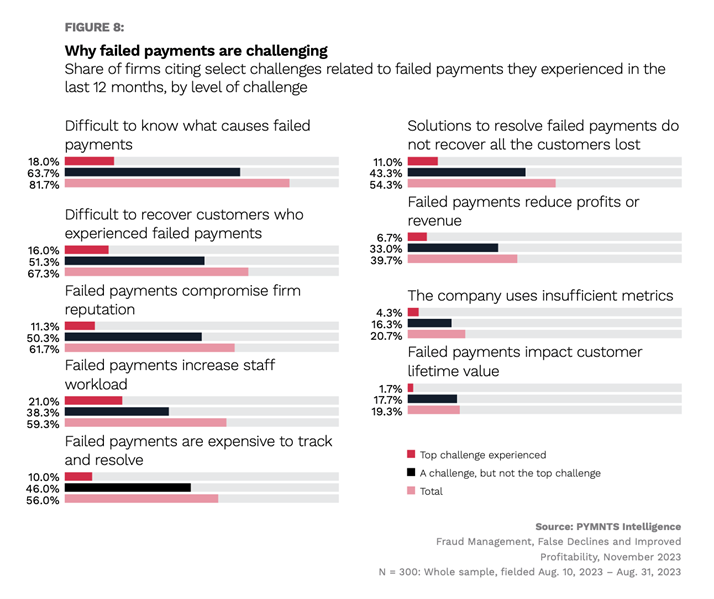

Despite the pervasiveness of failed payments and their impact on business volume and customer satisfaction, 82% of online merchants struggle to identify the causes of these failures. Similarly, 67% of online merchants face difficulties recovering customers who experienced failed payments, this being the main reason for customer churn.

These are only some of the key findings drawn from “Fraud Management, False Declines and Improved Profitability,” a PYMNTS Intelligence and Nuvei research collaboration that examines the intersection of fraud prevention and failed payments in eCommerce.

According to the study, 72% of firms experienced higher rates of failed payments in cross-border sales compared to domestic sales. This highlights the importance of screening mechanisms that identify fraud and typos for mitigating the incidence of failed payments, especially for international commerce. Visa Chief Risk Officer Paul Fabara said in a recent interview with PYMNTS, “Cross-border sales is an area in which it is worthy to have a journey that at the end of the day is going to provide additional protection to consumers. Opposite to an ACH transaction where consumers have absolutely no protection.”

However, only one-third of firms utilize these screening mechanisms, evidence of a missed opportunity to minimize false declines and recover failed payments. Most eCommerce firms cite customer satisfaction and cybersecurity as benefits to utilize them, but not profitability. Although nearly all firms plan to innovate their anti-fraud toolkits, just 1 in 6 see improved profitability as a benefit.

When implementing anti-fraud measures, the study revealed that most firms rely on third-party providers to find solutions to recover failed payments. This is especially significant when utilizing payment recovery software or payment collection solutions. In this line of argument, “The best way to ensure safe payments,” added Fabara, “is through collaboration between financial institutions, providers, consumers, and merchants, with the support of artificial intelligence (AI).”

Nevertheless, payment failures impact sales, customer satisfaction and operating costs. Six in 10 companies in the study stated they experienced an increased staff workload due to failed payments, resulting in a loss of profitability.

Fabara shared with PYMNTS his good prospects regarding anti-fraud toolkits available for companies: “In 2024, we might expect a quick step with better tools, and accessibility to those tools at relatively low operating cost”.

As long as these systems are perceived as a real solution to retain sales and improve profitability, we might expect further adoption of them.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More