Suppose you asked 8,000 consumers and over 2,000 merchants in four countries around the globe about epic changes to small and medium businesses (SMBs) sparked by the pandemic. Would it surprise you to know that SMBs make worthy competitors to the biggest retail names on earth — when properly equipped? Because they are, and new data proves it.

PYMNTS’ March 2021 Global Digital Shopping Index: SMB Edition, done in collaboration with Cybersource, opens by debunking a myth of the great digital shift: that size is all that matters.

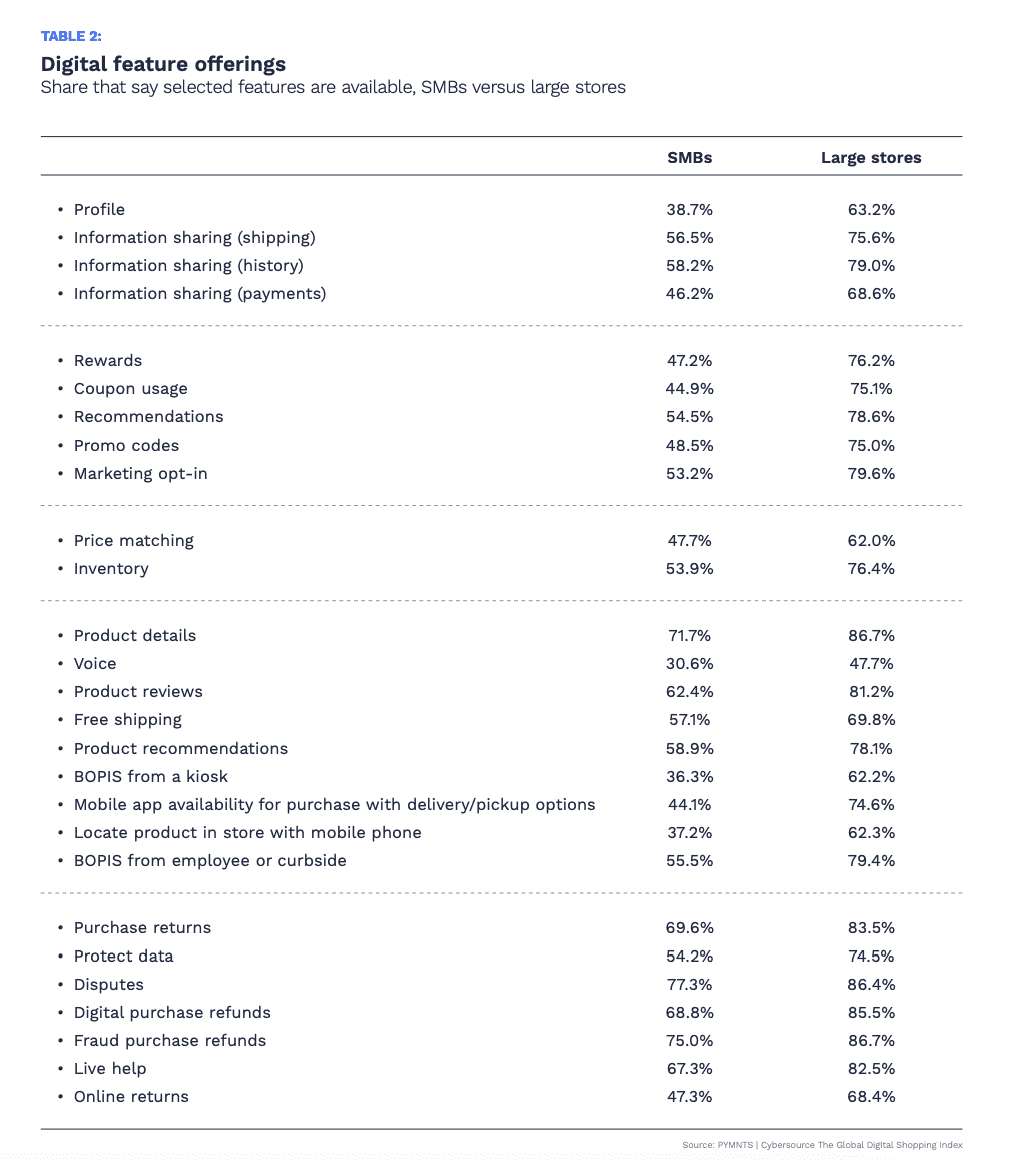

“Our research confirms some of these assumptions: SMBs are less likely to offer wide-ranging digital features and they tend to score lower than large firms in our Index, which measures satisfaction with various aspects of the shopping experience,” per the new Index.

But there’s a wrinkle in the new Index that bears deeper examination: “Consumers in the U.K. and Australia are as likely to use digital channels through SMBs as they are through large stores. Many SMBs are as ambitious as large stores in their plans to invest in digital services like mobile order-ahead and store pickup options. Our data also shows that an important subset of SMBs — those that make most but not all of their sales in-store — perform as well as large stores in consumer satisfaction. In fact, omnichannel businesses of all sizes generally score considerably higher than those that engage solely in eCommerce.”

It means that “size is not destiny when it comes to digital innovation and that well-executed strategies could magnify some of SMBs’ natural advantages,” per the new Index. In fact, knowledge of and connection to the communities in which they operate “may count for even more as the pandemic eases its grip and consumers rediscover the businesses that have served as anchors for their local economies,” both in-store and online.

SMBs Ranking As Top Performers By Closing Satisfaction Gap

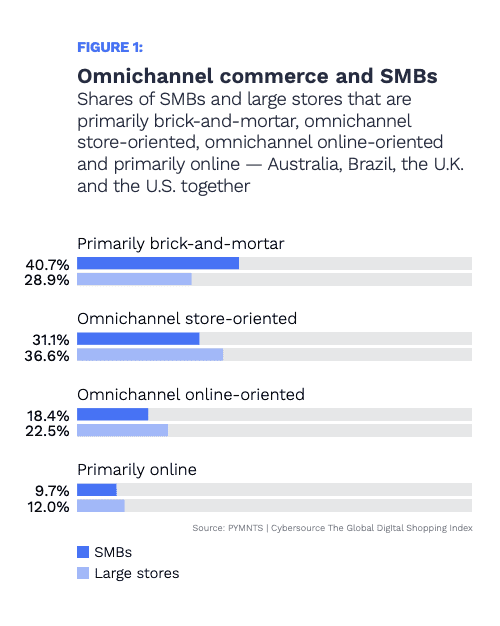

Dividing consumer groups into “primary brick and mortar,” “omnichannel store-oriented,” “omnichannel online-oriented” and “primarily online” in four international markets (Australia, Brazil, the U.K. and the U.S.) the Global Digital Shopping Index: SMB Edition finds that large retailers with vast resources score up to 25 points higher than SMBs on PYMNTS’ scale, weighted based on the features consumers most value in each of the four markets studied.

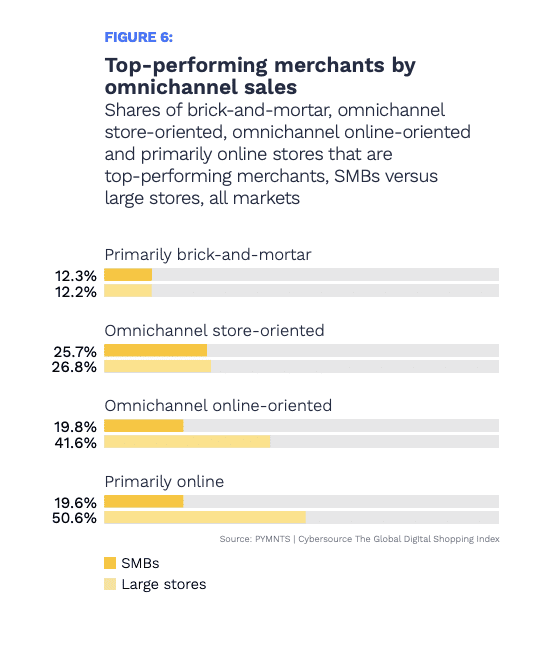

And while large online businesses are top performers, it’s a far more nuanced picture. For example, the Index notes that “omnichannel businesses that do a greater proportion of their sales in-store reveals a more complex pattern: SMBs do as well as large stores in this group. Twelve percent of SMBs that are primarily brick-and-mortar are top performers, matching the portion of large stores in this group. This is also the case for omnichannel store-oriented businesses: 26 percent of SMBs in this category are top performers, as are 27 percent of large stores.”

Put another way, SMBs offering physical retail with a solid online presence are effectively able to run with the big dogs of retail. As the Index states, “SMBs that are more brick-and-mortar-oriented appear to be able to bridge the satisfaction gap, perhaps because they offer less quantifiable attractions, such as hands-on shopping experiences or trust and familiarity.”

The Future Is Features

As lifestyles lean more into tech, features inevitably become what separates the great from the good. PYMNTS researchers found this to be the case with SMBs in Australia, Brazil, the U.K. and the U.S. throughout this series, and especially in this special SMB edition.

Per the Index, “17 percent of [shoppers] consider rewards the most important feature … making it the most cited among smaller stores’ patrons. Thirteen percent of large-store shoppers consider this feature most important. Our research shows elevated interest among SMB shoppers in other value-based features, such as coupons and promo codes, as well as convenience-based features, including buy online, pick up in-store (BOPIS).”

Another area where SMBs in the four studied markets are prioritizing is mobile, because that’s where the action is increasingly headed worldwide.

If Brazil is a bellwether — as many believe it to be — note findings there that “50 percent of SMBs in Brazil — a market where mobile is the primary channel for digital commerce — plan to invest in mobile order-ahead capabilities over the next three years, exceeding the share of large merchants that plan to do so,” as do 40 percent of SMBs in Australia, for example.

It adds up to this: significant shares of SMBs across the studied markets view improved digital-first capabilities as the key to a better customer experience, enhancing “the natural advantages SMBs have: the connection and presence they have in the communities they serve.”