According to a recent study conducted by PYMNTS Intelligence, 60% of shoppers used installment plans to purchase consumer products in the past year, with younger age groups exhibiting the highest usage rates.

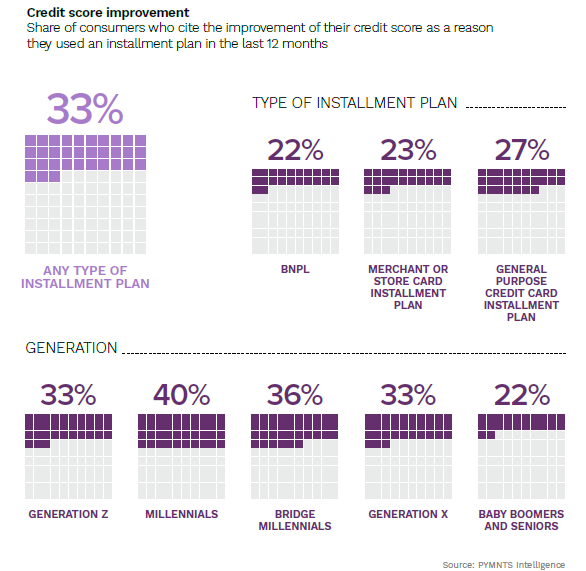

Another key finding from the study is that consumers are leveraging installment plans to improve their credit scores. Approximately 33% of shoppers who use installment plans do so with the goal of boosting their credit scores. This trend is particularly prominent among millennials and bridge millennials, with 40% and 36% of them, respectively, utilizing installment plans for this purpose.

Overall, general-purpose credit card installment plans are the most popular plans used for boosting credit scores, at 27%, followed by merchant or store card installment plans and buy now, pay later (BNPL) options, at 23% and 22%, respectively.

The need to improve credit scores is particularly critical, especially in the U.S., where having a strong credit score can be the determining factor in whether you are approved or denied for a mortgage or student loan, or get access to lower interest rates and better borrowing terms.

In fact, PYMNTS Intelligence data published in “The Credit Accessibility Series: BNPL’s Wide-Ranging Impact on Consumers and Merchants” shows that consumers with low credit scores of 650 or less are roughly twice as likely as the average consumer to experience issues that impact their finances and daily lives. Additionally, 80% of consumers surveyed have suffered financial hardship due to their low credit scores.

On the upside, better credit scores could put as much as $1,700 in consumers’ pockets, the data found, as well as enable consumers with low scores to afford essentials and access additional credit products.

Deep subprime consumers, too, can alleviate their financial woes by improving their credit scores, the data further noted, helping them to raise their living standards and keep high-interest-rate loans at bay.

As the study noted, “if deep subprime consumers — those with credit scores of 579 or less — raise their credit scores to near prime levels, they could increase their borrowing capacity by 68% of their income.”