As FedNow finally coming online generates a mix of reactions, money mobility generally — and instant payments specifically — have never been more in the spotlight. While FinTechs are gaining ground with offerings consumers want, significant room for improvement remains.

Based on two surveys — one of issuers, and another of consumers — “The Issuers Report 2023: FinTechs’ Instant Payments Mismatch,” a PYMNTS and Ingo Money collaboration, weighs the performance of FinTech issuers against consumer expectations around money movement and finds that while progress is being made, there are disconnects that demand attention.

As the study states, “Despite their efforts to meet consumer demand for P2P transfers, our data suggest that FinTech issuers need to better understand their customers’ needs. For instance, consumers were most likely to use FinTech providers because they offer a wide array of fund transfer options and fast transactions, but FinTechs tout convenience and customer experience as their top features.”

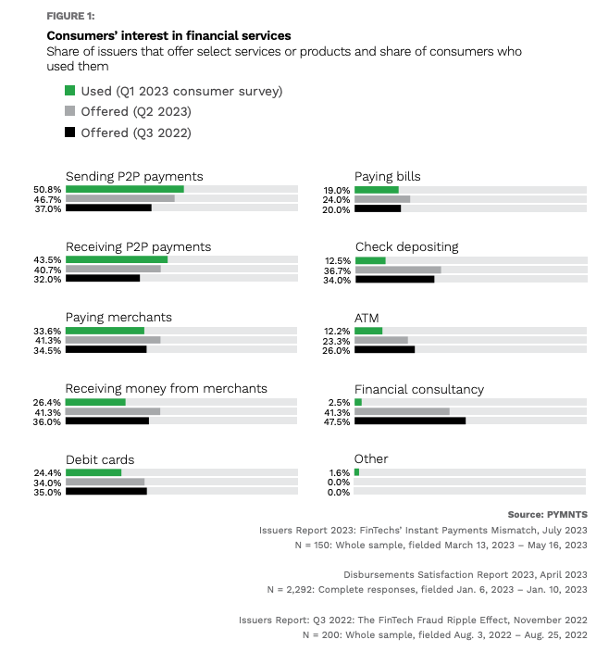

Sending and receiving P2P payments are dominating consumer usage of FinTech issuers, as survey results from Q1 2023 activity show. Paying merchants also ranks high, showing where consumer interest in using FinTech payment solutions is also concentrated.

As FinTech issuers respond to the demand for more instant services, their Money Mobility Index (MMI) scores are rising due to higher consumer satisfaction. Looking at changes to MMI scores since Q3 2022, “The Issuers Report 2023: FinTechs’ Instant Payments Mismatch” notes that “Currently, 47% of FinTechs allow consumers to send P2P transfers and 41% allow consumers to receive these transfers. This represents an increase of 10 percentage points for sending and 9 percentage points for receiving since Q3 2022.”

More Options Needed

And while these are meaningful gains, the report points to “a mismatch between FinTech issuers and account holders as to what features customers deem important when using a FinTech account.” FinTech CFOs surveyed for this study believe convenience and customer experience were prime drivers to use such accounts. On the contrary, our consumer survey finds that account holders want a wide array of fund transfer options and speedy transactions.

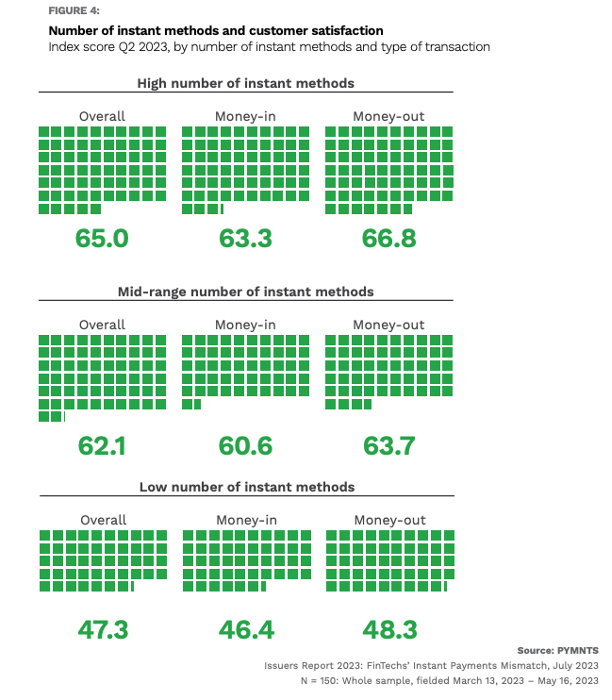

Additionally, while FinTech issuers get generally higher marks for deposits and transfers, the study states that “FinTech customers faced more issues and reported being less satisfied when moving funds in than when moving funds out,” adding that “FinTechs providing a high and a mid-range number of instant payment options average an Index score that is three points higher for money-out transactions than for money-in ones, while those with a low number of payment options average an Index score that is two points higher for money-out transactions than for money-in ones.”

Aligning FinTech issuer services with consumer expectations is where more work is needed. Our consumer study finds that 41% of consumers who reported issues when depositing money into their accounts said that a guarantee of good funds/speed was the issue they faced most often, while 28% of consumers who reported issues when moving funds out of their accounts identified the guarantee of good funds/speed as their biggest concern.

By contrast, just 20% and 12% of FinTechs, respectively, reported the same issues regarding their account holders.