Often as part of loyalty initiatives, brands and merchants partner with financial institutions to launch their own credit cards.

These store cards or merchant-branded cards not only allow cardholders to access a series of benefits such as discounts or reward points when purchasing products, but they can also unlock the possibility of paying in set installments, as some general-purpose credit cards can.

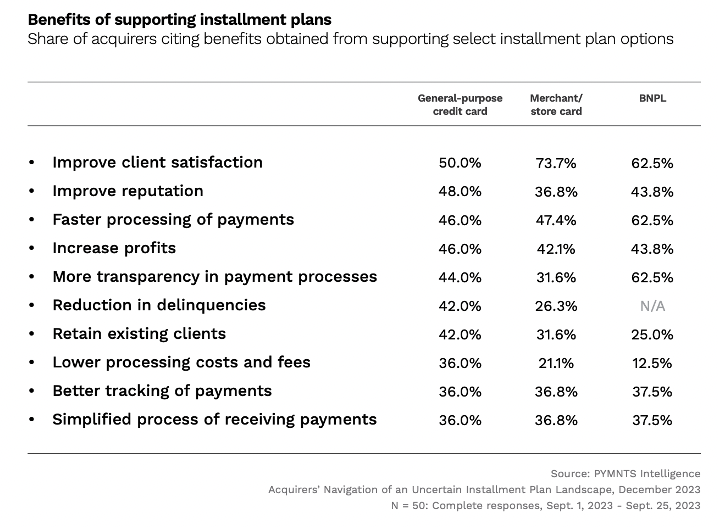

The PYMNTS Intelligence study “Acquirers’ Navigation of an Uncertain Installment Plan Landscape,” revealed that around three-quarters of acquirers’ clients are satisfied with merchant/store card-based installment plans. That represents the highest satisfaction observed among all split-payment plans reviewed, including buy now, pay later (BNPL) options, and those that work with general-purpose credit cards.

The study examined consumers’ use of installment plans for completing common purchases. It surveyed 50 acquirers that work with financial institutions, merchants and other pay-later system providers.

Benefits of Installment Plans for Merchants

According to the research, 74% of acquirers said their clients benefit from an improved customer experience when using their branded store cards to pay their purchases in installments. This share exceeds the corresponding portion of satisfaction among BNPL providers, with 65% saying the same; client satisfaction among general-purpose credit card installment plans lags at 50%.

Support for installment plans by acquirers revealed the importance of offering flexible payment options to boost sales and gain competitiveness. With over 62% of individuals living paycheck to paycheck as of November, and with the consumer price index at 3.4%, flexible payments help customers to make ends meet. Merchants not offering solutions like these may be missing a business opportunity, especially during periods of the year that have high promotional intensity.

Data showed that nearly 68% of installment plan acquirers think business clients would be very likely to sell higher-priced items or services if they offered card installment plans to clients before checkout.

PYMNTS Intelligence research showed that installment plan adoption is occurring across all consumer demographics and is not limited to specific income brackets. For instance, high-income earners favor installment plans more than low-income consumers, with 64% of consumers earning $100,000 or more annually using these plans, which constitutes an opportunity for merchants.

The positive impact on customer experience confirms the critical role of installment plans in enhancing consumer satisfaction and loyalty. By providing flexible payment options, installment plans could well serve as an engine to drive sales growth, especially among retail brands and merchants that offer compatible cards.