Credit card installment plans for common purchases are gaining popularity among consumers, who are drawn to the flexibility they offer in managing their spending and credit.

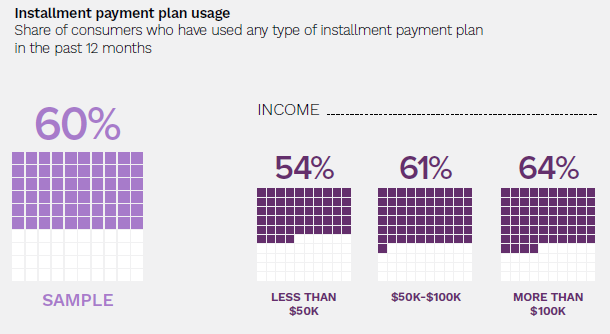

As detailed in “Installment Plans Becoming a Key Part of Shopper’s Toolkit,” a PYMNTS and Splitit collaboration, 60% of shoppers used these installment plans to buy consumer products in the past year, with younger age groups exhibiting even higher usage rates.

These findings challenge the assumption that younger generations are averse to credit use. Millennials, in particular, are much more likely to opt for an installment plan compared to baby boomers and seniors. They also show a preference for general-purpose credit card installment plans over other types.

This aligns with findings detailed in “The Credit Economy: How Younger Consumers Make Credit Decisions,” which show that more than half of younger consumers use credit for everyday purchases as a way to better manage their cash flows, a further indication that young consumers are embracing credit as a cash management tool.

The study also provides insights into the usage patterns of different generations. Generation Z consumers tend to use installment plans for everyday essentials, such as clothing, groceries, and health and beauty products. On the other hand, millennials are more likely to use installment plans for one-off purchases, including furniture, appliances and travel.

It is also interesting to note that installment plan use is not limited to specific income brackets. In fact, the study finds that high-income earners favor installment plans more than lower-income consumers, with 64% of consumers earning $100,000 or more annually using these plans, exceeding the shares of consumers in lower income brackets.

This highlights that consumers across all income brackets are tapping into the benefits installment plans offer, defying long-held perceptions about the relationship between financial means and credit use.

The widespread use of credit card installment plans among individuals with high incomes indicates a profitable potential for merchants, who can harness this trend to expand their market presence and capitalize on shifting consumer habits.

That said, there are still obstacles to broader adoption that retailers will have to tackle head on. The PYMNTS-Splitit report identifies consumer indifference and friction in current installment plan offerings as key challenges. To address this, merchants will need to assess and adapt their current installment plan offerings to meet consumer preferences and priorities.

The report also emphasizes that trust, minimal costs and other incentives play important roles in influencing consumer decisions to use installment plans. As a result, fine-tuning installment offerings to align with these priorities can go a long way to help merchants build stronger brand credibility and foster customer loyalty.

Timing and positioning are also crucial when offering installment plans. Consumers prefer installment plan options to be presented before the checkout process, allowing them to evaluate their shopping decisions in terms of value and volume. By integrating installment plan offerings early in the shopping journey, merchants can enhance customer satisfaction and potentially influence purchasing decisions.

In conclusion, the widespread adoption of installment plans by high-income earners is reshaping consumer behavior and challenging assumptions about credit use and income. Merchants have the opportunity to tap into this trend by adapting their offerings to meet consumer preferences, building trust and providing a seamless customer experience.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More