In the grocery segment, it’s the tug of war for space on the (brick and mortar and virtual) shelves.

Operating in an industry notorious for razor-thin margins, grocery firms have a vested interest in private label sales, which typically carry higher profits.

And for the grocers themselves, there’s an advantage of having significant control over what goes where, which sets up the aforementioned tug of war with the brands.

In short: The “private push” will see some continued push back.

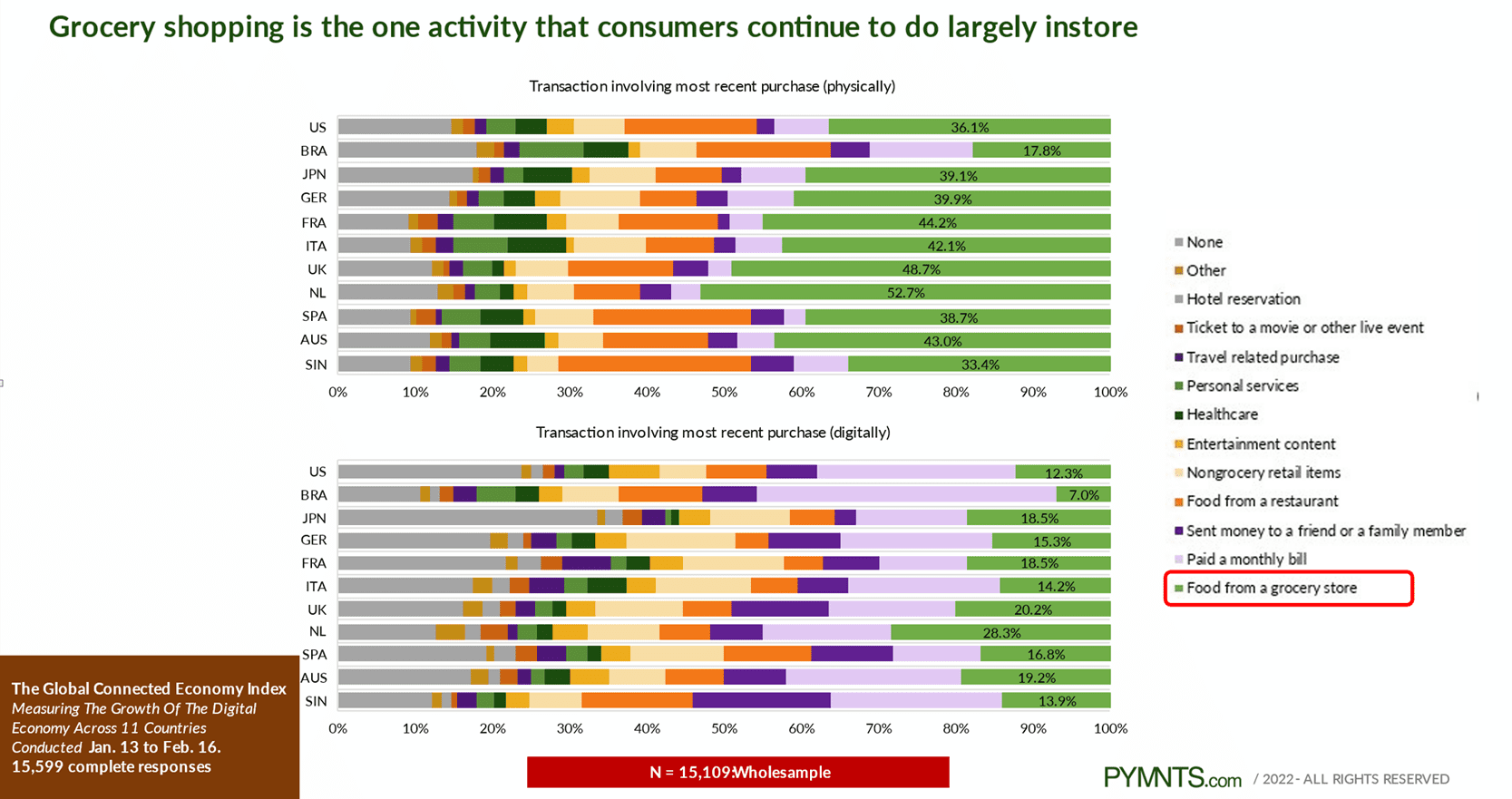

As PYMNTS data shows and as illustrated in the chart below, shopping for food and beverages — among the staples of daily life — still remains an activity done onsite. And that’s true across the globe, as measured across 11 countries.

We’re seeing some continued momentum with those private label initiatives. Kroger reported earnings on Friday morning (Sept. 9) that showed that its “Our Brands” segment notched more than 10% growth and launched more than 170 items in the quarter.

But the brands themselves are not sitting still. We noted recently that during earnings season, companies such as Kraft Heinz Co. said in its own commentary that tiered pricing offers one strategic option to keep consumers loyal. Target and Walmart executives have noted in their earnings commentary that private label purchases have been gaining ground, too.

And yet, the brands have a conduit through which to combat the rise of consumer spending on private goods: Through online channels.

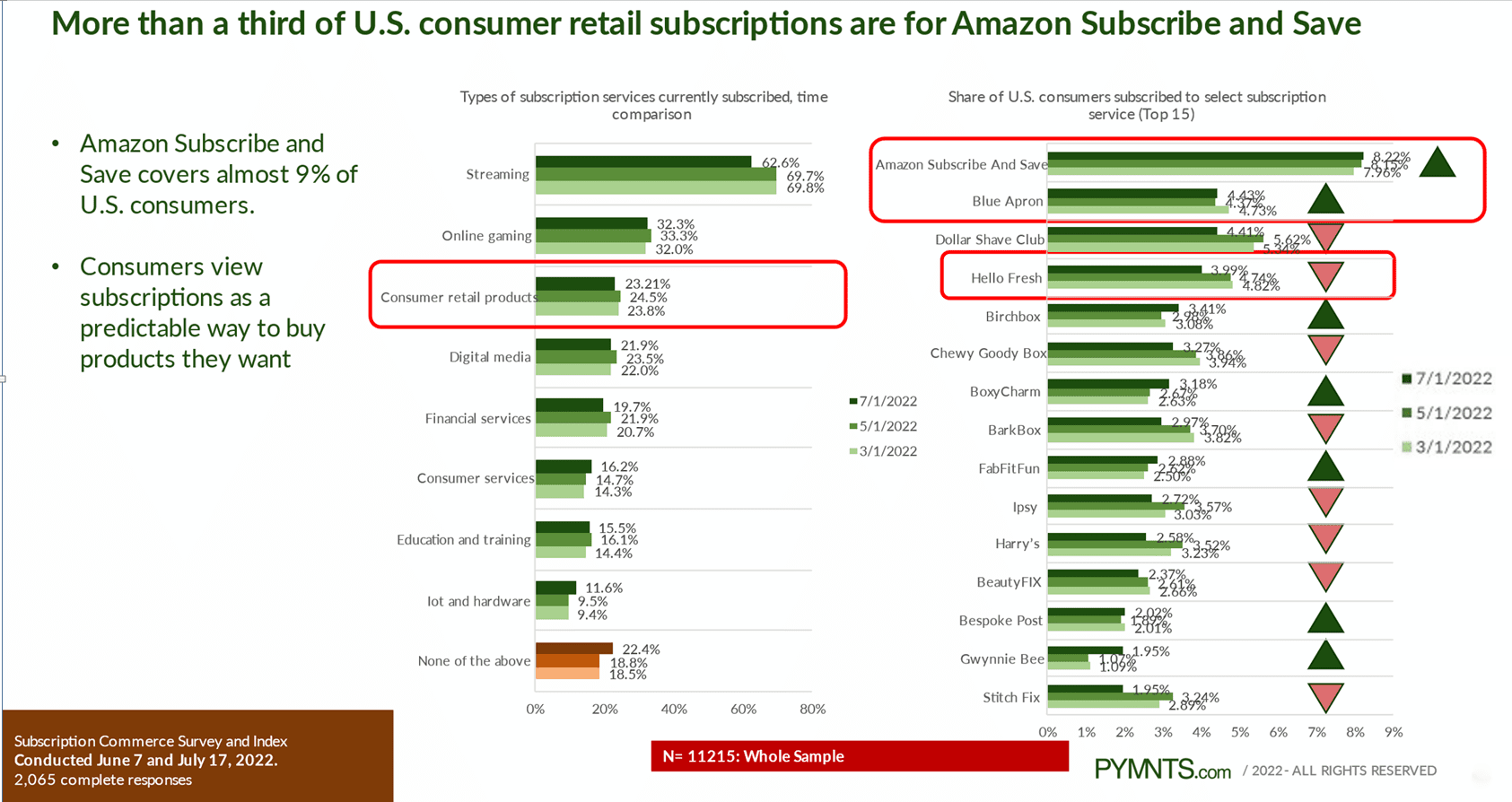

As PYMNTS’ research shows, among the most popular subscriptions are Amazon Subscribe and Save, Blue Apron and Hello Fresh. These are all ways and means to get food on the table and also represent at least some competition for in-store commerce.

Traditional grocers are facing a formidable threat from Amazon, which has been gaining some share of spending on food and beverages, across brick-and-mortar settings such as Whole Foods and digitally, too. As seen below, Amazon’s share is growing, albeit coming off a small base (Its chief rival, Walmart, too, has been gaining share).

The fact remains that inflation is going to keep driving food prices up — which will prompt consumers to seek out relatively lower-cost (and convenient) options to combat that inflation. As reported earlier this month, in the latest baseline update for U.S. agricultural markets released last week on Sept. 2, the Food and Agricultural Policy Research Institute (FAPRI) at the University of Missouri said that the CPI for food is projected to increase by 9% in 2022 and food‐at‐home prices are expected to increase 10.6%.