Despite a year of unmatched growth, countless news stories and a few blockbuster acquisitions within the buy now, pay later (BNPL) space, as the old saying goes, you ain’t seen nothin’ yet.

This, as new research in the Buy Now, Pay Later Tracker for December 2021 shows that, despite a year-long rollout and ramp-up effort that saw BNPL usage grow to one-third of overall consumers, as well as a near-doubling of consumer awareness in citing it as a preferred payment method for the holiday season, its overall position within the realm of financing options is still tiny.

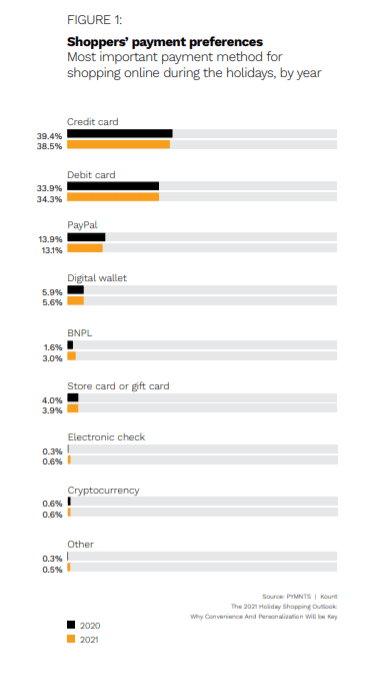

As a quick glance at the attached chart from the PYMNTS and Sezzle report shows, credit and debit cards still dominate consumers’ head space, accounting for a combined 73% share of the payment preference survey.

On a trend level, it is also worth noting that credit cards slipped a bit (to 38.5% in 2021 from 39.4% the year before) while debit cards increased a bit, in line with broader spending trends and a budding consumer bias against debt.

While PayPal held onto a solid but distant third place position, its 13.1% payment preference rank in 2021 was also down a smidge from 13.9% a year ago, with similar slides in this survey also seen in digital wallets and store cards.

But, while you may have to squint to see it, BNPL’s 3.0% tally in 2021 — a figure that’s less than one-tenth the credit/debit shares — its growth rate nearly doubled, making it far and away the fastest growing payment method in the minds of consumers.

The Mind Game

And therein lies the magic — and the motor — that is set to drive BNPL to the next level once again: awareness.

Simply put, when it comes to making purchases and paying for things, BNPL is, as the saying goes, living rent-free in the minds of more and more consumers.

Not just any consumers either: PYMNTS research found the appeal of installment payment plans is also showing a distinct bias toward younger shoppers. In fact, generationally speaking, millennials and bridge millennials (roughly aged 25-40) were the most likely to seek out a store that offered BNPL.

Specifically, the data showed these coveted demographics, in or entering their peak earning and spending years, each showed a 30% preference for stores that offer BNPL, compared to roughly 22% of all age groups who felt that way, and more than double the 13% of baby boomers and seniors who have boarded the BNPL train.

Retailers Rush

It’s the kind of statistics that explains why retailers have clearly taken notice of the trend and are adding the optionality at a record pace. When given a choice to spread out payments over a few months (or in some cases now a couple years) consumers tend to spend more when the chance to purchase larger items is put within their reach.

This option is proving to be especially appealing to consumers who may not be as financially stable, as it provides them with greater peace of mind, a trend that should not be disregarded given that 33% of consumers say they are still facing financial insecurity because of COVID-19.

Other factors revealed in the study that reflect BNPL’s dual push-pull effect from retailers and consumers, include a growing shift away from debt and high interest rates and toward better financial decisions, especially those that can help — or at least not hurt — a consumer’s credit rating.

While the budding BNPL business is only starting to get on the regulatory radar, its path forward looks otherwise unimpeded, with plenty of headroom to grow amongst payment methods, and the twin tailwinds of consumer demand and retail need also helping to get it there.