Fraud’s hindering money mobility, and the customer experience is rife with frictions.

The average FinTech loses 1.7% of its annual revenue to fraud — approximately $51 million per year.

And as we found in the report “The FinTech Fraud Ripple Effect: The Money Mobility 2022 Series,” a PYMNTS and Ingo Money collaboration, nearly half of issuers say the costs incurred from fraud are the top challenge they face as money moves between accounts.

At a high level, money mobility is shorthand for the ease with which holders can shift funds in and out of accounts and access those funds.

It makes sense that as FinTechs experience more fraud, they impose more frictions on their account holders. The more frictions established to beat the fraudsters, the more operations are impacted. Consequently, the negative ripple effects hit the end users of those accounts. The cost of fraud is cited as among the top challenges facing money movement.

Of the 200 FinTechs we surveyed, the great majority — at more than 79% — said that moving guaranteeing “good” funds was a difficulty for consumers, as was the ability to move that money with speed.

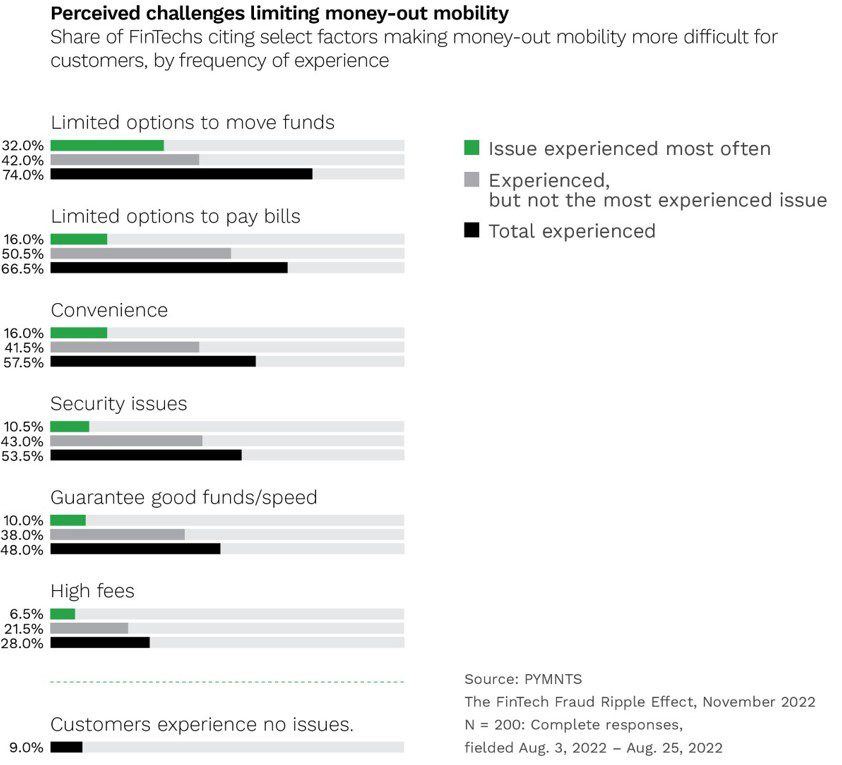

And when it comes to moving money out of accounts, the majority of firms, at about 74%, state that there are limited options to move the funds, as seen in the chart below.

There’s a disparity here, too, one that is based on the very size of the enterprise. The data shows that small- and medium-sized FinTechs are more likely than their larger competitors to consider fraud one of their most pressing issues.

Respondents to our queries said that 55% of mid-sized firms and 47% of small firms cite the cost of fraud as their most pressing issue, far exceeding the 35% of larger firms that agree.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More