Main Street small business owners anticipate limited wiggle room to boost prices, and they’re prepared to tap credit to help grapple with operating costs.

As disclosed by the National Federation for Independent Businesses Tuesday (Dec. 12), the Small Business Optimism Index was down in November by 0.1%. The index has logged 23 straight months below its 50-year average reading. Inflation continues to be a concern, and 22% of firms reported that inflation remains their single most pressing concern at present.

A net negative 17% of all owners (seasonally adjusted) enjoyed higher nominal sales in the past three months, unchanged from October and the lowest reading since July 2020, per the index.

The net percent of owners raising average selling prices decreased five points from October to a net 25% (seasonally adjusted). A net 0% of owners viewed current inventory stocks as “too low” in November, up three points from October, the data showed.

Profits Are Being Pressured

The pinch of top-line pressures and the need to satisfy operating costs is eating into profits.

Firms reporting positive profit trends were a net negative 32%, unchanged from October. More than a third cited weaker sales, and a mid-teens percentage point tally said that labor costs and material costs were higher.

Credit can be — and in the current environment, might be — used to help contend with volatility that marks sales, while operating costs remain unpredictable and stubbornly high.

Will Credit Be There?

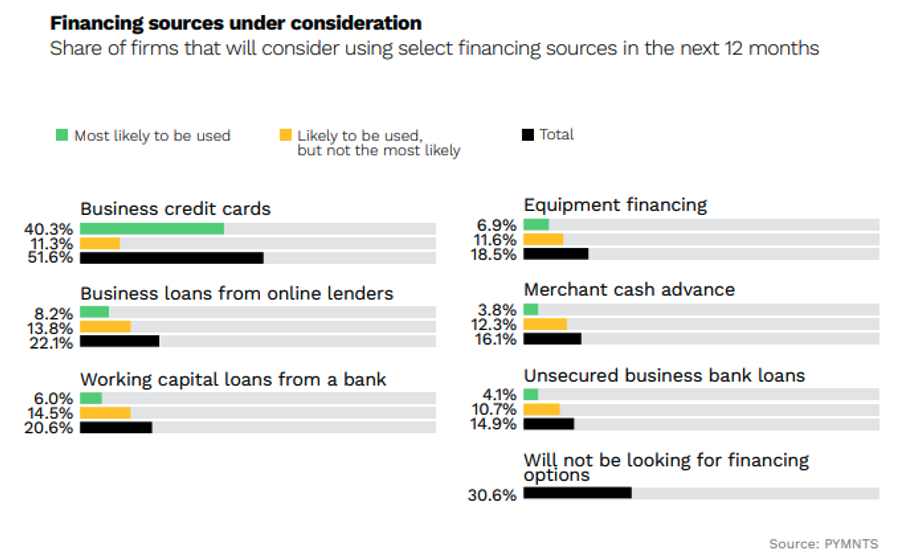

PYMNTS Intelligence found that nearly 34% of small- to medium-sized businesses (SMBs) do not currently use credit but want to start doing so. As of July, 47% of SMBs with annual revenues of $10 million or less had access to business or personal financing. The impact is being keenly felt in retail, as 41% of SMB retailers said they had access to financing. Over half of SMBs said they anticipated using corporate cards into the middle of 2024, surpassing business loans from online lenders (22%) or working capital loans from banks (21%).

But intent may be dashed against the hard shoals of reality. The NFIB found that 25% of respondents reported that all their credit needs were met, and 63% said they were not satisfied in a loan. A net 8% reported their last loan was harder to get than in previous attempts. A net 25% of owners reported paying a higher rate on their most recent loan.