The subscription economy — including everything from financial management apps to automated savings services — has brought consumers’ need for improved control over their finances into the spotlight. Globally, as millions of consumers use recurring payments to automate tasks digitally, the importance of rapid, secure payments and deposits management to national economies has spurred regulatory agencies to action.

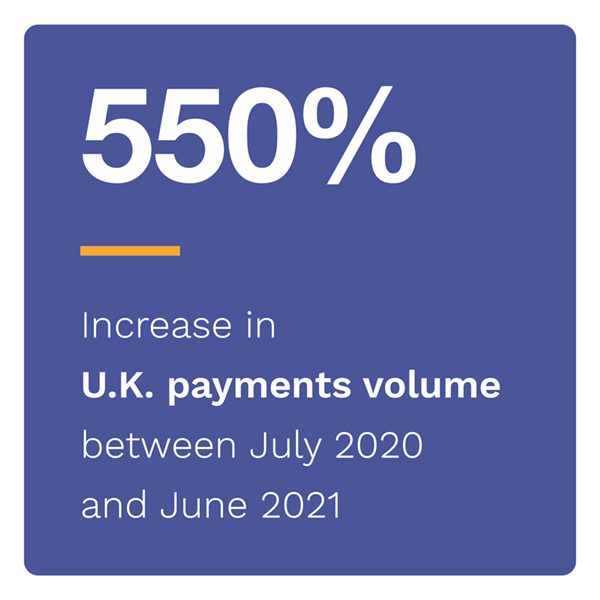

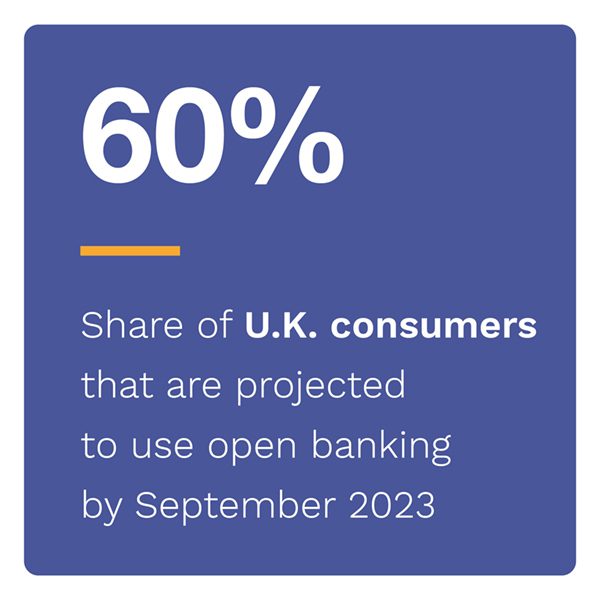

Earlier this year, the United Kingdom’s Competition and Markets Authority (CMA) presented a mandate to the nation’s nine largest banks: They would have just six months to improve the customer experience for users of apps and websites by enabling variable recurring payments (VRP) — a feature that allows customers to easily sweep money between accounts to manage recurring payments. In Open Banking API — Improving Customer Experience With Variable Recurring Payments, a PYMNTS and TrueLayer collaboration, we examine how the new impetus for payments management modernization will impact third-party providers (TPPs) and consumers eager for streamlined payments.

According to our research, the CMA mandate may produce widespread positive changes for consumers and subscription-based services. Not only will this new requirement help businesses and customers access funds and payments more quickly, but it also will give consumers new levels of control over how and when they make payments while managing multiple accounts using subscription-based services. VRP application programming interfaces (APIs), once implemented by leading banks, will empower FinTech companies to develop innovative new products that may make a subscription services’ recurring payments architecture more customizable for the needs of consumers.

Open banking is regulato ry compliant by definition. Based on secure bank-to-bank communications, open banking APIs offer TPPs the ability to provide an “instant” banking infrastructure to B2B clients and customers, streamlining payments processes and user authentication. In addition, the new VRP feature will likely drive customer experience innovation for TPPs and their clients. Open Banking APIs take the guesswork out of innovation, allowing TPPs to develop new user experiences that deliver value to consumers without restraints on the features they can create because their products’ technical payments capabilities lag behind their vision.

ry compliant by definition. Based on secure bank-to-bank communications, open banking APIs offer TPPs the ability to provide an “instant” banking infrastructure to B2B clients and customers, streamlining payments processes and user authentication. In addition, the new VRP feature will likely drive customer experience innovation for TPPs and their clients. Open Banking APIs take the guesswork out of innovation, allowing TPPs to develop new user experiences that deliver value to consumers without restraints on the features they can create because their products’ technical payments capabilities lag behind their vision.

When a subscription service uses an open banking VRP API to manage payments, consumers may cancel recurring payments at any time and ask their bank to cancel TPP access to their data. This allows subscription services to develop new, customizable subscription models that may permit consumers to pause memberships or select subscription periods of various lengths without fear of unwanted recurring charges.

The report also shares insights from Plum, a leading money management and investment app, on how giving consumers more control over their money using fast, seamless payment processes improve customer experience and ultimately builds trust. According to Elise Nunn, Plum’s head of product and data, the CMA mandate will be good for business.

Trust is therefore essential in helping build consumer confidence, both with the product and with managing their money. Speed, security and reliability of transfer are critical to making sure that trust is built. If a transfer takes several days to settle, this can be alarming for customers, especially if they are not used to moving money.

To learn more about how TPPs and consumers can benefit from the flexibility offered by open banking APIs, download the report.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More