Installments loans we know as buy now, pay later (BNPL) have broad appeal, and months of research into how different types of consumers use BNPL services is revealing unique patterns.

Uptake by consumers living paycheck to paycheck is understandably strong, while increasing usage of BNPL solutions by those not struggling to make ends meet is equally fascinating in that it shows BNPL’s power as a tool to help “worry-free” consumers stay that way.

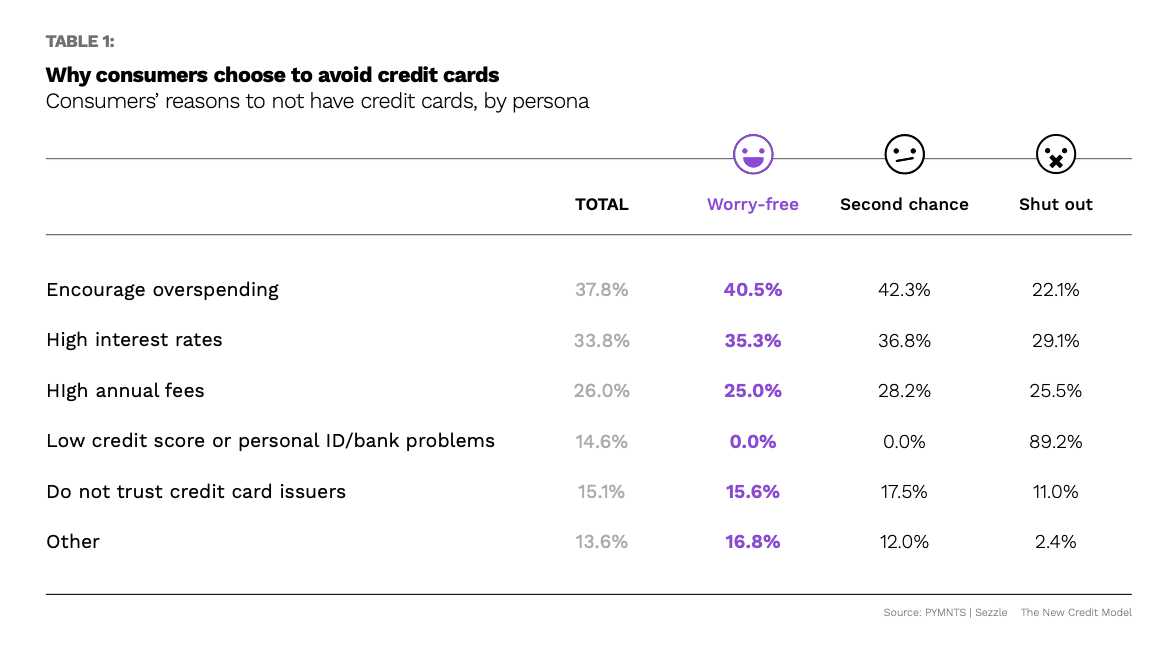

According to The New Credit Model: Why Financially Worry-Free Consumers Still Want Alternatives To Traditional Credit, a PYMNTS and Sezzle collaboration, “worry-free consumers — those with good credit or access to credit — are interested in alternatives to traditional credit card payments,” noting that 40% don’t use credit cards to avoid overspending, 35% avoid credit due to high interest rates, and 25% of the worry-free feel card fees are too steep.

BNPL as budgeting tool is a trend that emerged in 2021 and it has a strong draw for three BNPL personas identified PYMNTS research, although again, not always for the same reasons.

Noting that smaller purchases have been the firm’s sweet spot, Sezzle President Paul Paradis said in a new PYMNTS TV On the Agenda panel discussion that the company launched “a longer-term installment loan solution for higher ticket purchases last year and are starting to see that really pick up now in higher ticket categories like furniture, exercise, equipment, travel high and electronics,” adding that Sezzle has high expectations for personas seeking larger loans.

Get the study: The New Credit Model: Why Financially Worry-Free Consumers Still Want Alternatives To Traditional Credit

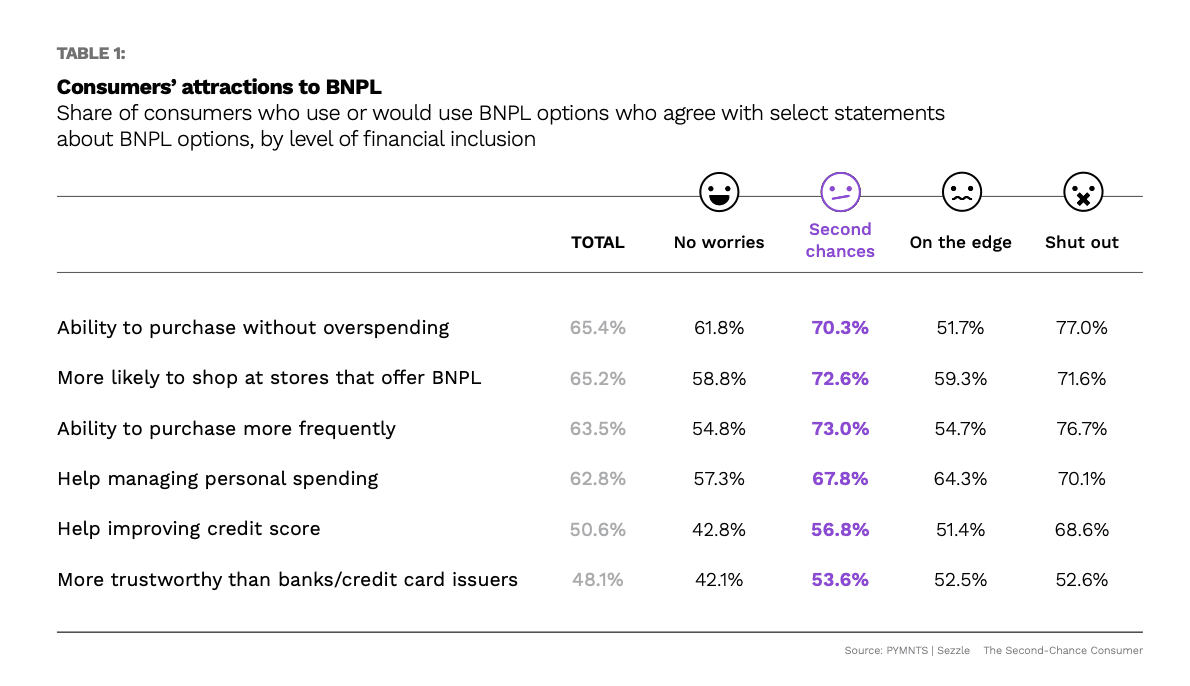

Usage among second-chance consumers with lower FICO scores and limited access to revolving credit tends to be more utilitarian ways than with their worry-free cohorts.

In The Second-Chance Consumer: How Buy Now, Pay Later Payments Create New Merchant Opportunities we found that over half (55%) of respondents like BNPL to manage payments, while more than 4 in 10 (43%) like it for budgeting and managing personal spend.

“These two capabilities were second-chance consumers’ most-cited benefits, yet notable shares of respondents also said it allowed them to avoid fees (25%) and held less chance of fraud than other payment methods (19%),” per that study of over 7,000 U.S. consumers.

Shut-out consumers, as the nomenclature implies, have FICO scores and poor or thin credit files, giving them few choices outside of predatory options. For them, access to installment credit can be a life saver, which ends up reflecting well on merchants offering it.

“Retailers who want to boost their profile among an often-underserved demographic group that tends to feature enthusiastic and budget-conscious consumers may find new opportunities for consumer engagement by offering BNPL as an option at checkout,” that study states.

Similarly, 59% of worry-free consumers who use or would use BNPL solutions said presence of BNPL options at checkout also make them “more likely to shop with those retailers.”

Get the study: The Second-Chance Consumer: How Buy Now, Pay Later Payments Create New Merchant Opportunities