Moreover, cardholders who have both types of cards tend to reach for the latter more often. In fact, 61% say they frequently use their general-use card. Nonetheless, co-branded cards are relatively more popular among older consumers and those earning over $100,000.

In “The Role of Strategic Partnerships in Consumer Credit Cards,” a PYMNTS Intelligence and Elan collaboration, we examine the state of play for various card types, including the key drivers for card ownership and how consumers view these cards differently. The study draws on insights from two surveys. The first survey of 3,036 U.S. consumers was conducted from Feb. 15 to March 20. The second survey of 776 U.S. consumers was conducted from March 13 to March 20.

Other key findings from the report include:

Loyalty and rewards benefits rank as the top reason draws for co-branded cards.

To capture the attention of more potential cardholders, providers should leverage loyalty and rewards benefits. These are the primary draw for co-branded cards, even above low fees and interest rates. Thirty-eight percent of cardholders cite loyalty and rewards benefits as the top reason for obtaining a co-branded card. This is more than twice the rate seen among consumers with general-use cards.

Consumers prefer co-branded cards from large businesses that provide easy opportunities to earn and use rewards.

Sixty percent of individuals with co-branded credit cards say they most heavily use a card from a retailer affiliate, with 19% using one from Amazon alone. Relatively small shares cite a card from a travel affiliate, such as airlines and hotels, and even fewer from other affiliate categories. However, travel affiliate cards tend to generate higher average spending levels, making this a lucrative space in the market.

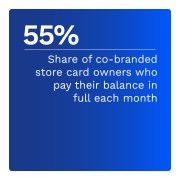

Consumers are more likely to revolve balances on general-purpose cards.

We find 55% of respondents with store cards, and 52% of those with co-branded credit cards pay their full balances off monthly. Meanwhile, just 49% of general-purpose card holders do so. Consumers appear to view co-branded cards more as ways to access rewards and loyalty perks. On the other hand, they treat general-use cards more as borrowing tools.

Even though general-use cards are the go-to choice for most consumers, co-branded credit and store cards have substantial appeal. Providers that lean into the cards’ core value propositions may be able to expand their reach. Download the report to learn more about what draws consumers to co-branded cards and how providers can better leverage this.