The BNPL Innovation That Pure Plays Unlocked and Banks Are Missing

When general-purpose credit cards were introduced in the late 50s and early 60s, they were advertised as a way for consumers to buy something they wanted or needed but didn’t have the funds on hand to pay for in full at that moment.

Payment flexibility — and the convenience of a single card to shop many merchants — was the appeal of that card. Consumers could pay their balances in full at the end of the month, or they could pay whatever they were able to afford that month and chip away at what they owed.

(For a walk down the credit card’s memory lane, it’s worth watching this 1960 Barclaycard documentary video explaining how credit cards work to an audience of general consumer credit newbies.)

Fast forward now about 60 years.

One card to rule them all.

Or more accurately, one payment method that offers different repayment options for how consumers pay all the merchants they shop.

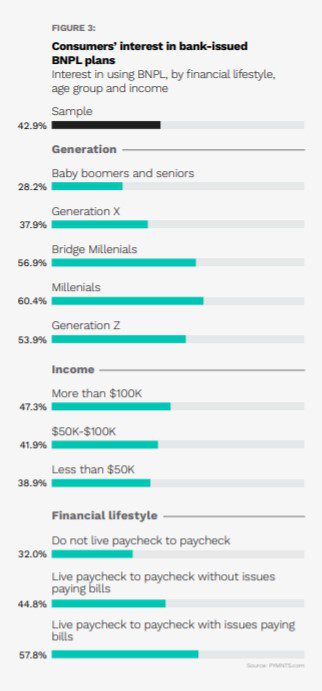

That’s what 45 percent of the adult population in the U.S. told PYMNTS they’d like their bank to provide in a study that was conducted November 5-10, 2021, based on a national representative sample of 2,237 qualified respondents.

Read more: Banking On Buy Now, Pay Later: Installment Payments And FIs’ Untapped Opportunity

It probably isn’t lost on banks that what consumers say they want sounds very much like the value proposition that they’ve have been promoting to their cardholders for about the last six decades.

Or that it is the same value proposition that the pure-play Buy Now, Pay Later providers have co-opted over the last two years with such great intensity. They are now using that value proposition to their advantage to capture consumer affinity, market share and merchant interest by themselves issuing the one “card” to rule them all: Pay now, in three or four installments, or every month for a finite period of time.

Or that this finding implies that 55 percent of consumers might consider such an option from another credit provider they trust.

Pure-play BNPL critics say they’re one economic downturn and/or one CFPB rulemaking away from being hobbled.

Traditional credit card advocates say that banks, who know how to underwrite and price credit, will ultimately prevail due to that expertise — as well as their consumer trust and massive installed base of credit card customers.

Just give it time. And a little help from bank-friendly FinTechs.

They emphasize that some issuers already give consumers the option to break up purchases into installment payments once they get their monthly statements, or when emails post-purchase invite consumers to break that purchase into installment increments.

And that findings like the ones from PYMNTS’ research are tangible proof-points that consumers want BNPL innovations to come from their bank.

That may be. But consumers aren’t currently using their banks much for installment payments — mostly because the BNPL options that banks offer right now aren’t really that much of an innovation.

See also: Banks Should Buy Into Buy Now, Pay Later as BNPL FinTechs Push Into Banking, Card Spaces

The Big BNPL Innovation Isn’t Installment Payments

According to PYMNTS research, roughly 50 million consumers in the U.S. have used BNPL to pay for at least one purchase over the last 12 months, 19.7 percent of the US adult population. The most popular providers of those services aren’t banks but pure plays: Afterpay and PayPal are the most frequently used. Affirm, Klarna, Sezzle and Zip are also on the consumer’s list of favorites.

Related: 60% of Consumers Know About Buy Now Pay Later

Two-thirds of U.S. consumers tell PYMNTS that they’ve increased the frequency of BNPL use over the last twelve months, and 70 percent of those who have used it over that period report that they plan to use it more in the next year.

We also know from data that PYMNTS will release soon that BNPL isn’t cannibalizing store cards, as some merchants may fear.

Instead, it is taking share from credit cards — perhaps most importantly from the affluent consumers who have them and are using zero-interest BNPL to buy big ticket items. For those consumers, free money repaid over time appears to be a bigger draw than rewards or cash back on those purchases.

Affluent consumers are not the only ones making the switch. Pure-play BNPL players are also moving cash or debit card sales to merchants from consumers for whom BNPL is a welcome credit alternative they can’t get from their bank. Merchants enjoy getting incremental sales and higher basket sizes without taking on that credit risk.

At 19.7 percent of the adult U.S. population, BNPL is beginning to sound like a big threat to the traditional credit card issuers.

Like every other disruptive force in FinTech, BNPL innovators have gathered momentum quickly and built a loyal user base that’s growing in numbers. More consumers are using their favorite BNPL providers to make purchases in categories beyond clothes and beauty — and for purchases that bring a bigger ticket along for the ride.

BNPL players have shifted the conversation away giving consumers the option to finance later, focusing instead on the certainty of how and when they will pay for what they want to buy.

The Credit Card Issuer Conundrum

Over the years, credit card issuers have used acceptance as their competitive calling card. Acceptance provides the certainty that a card can be used to make a purchase of just about any product at just about any merchant, anywhere in the world.

Credit lines give consumers the guardrails for how much they can spend in the aggregate; monthly statements give consumers information about what they bought over the course of the month, the balance due and the minimum payment acceptable to keep the card in good standing.

Today about half of cardholders pay those balances in full — the rest revolve those balances over some period of time. Rewards and cash back provide the incentives to keep consumers loyal to those cards and make more purchases using them.

The BNPL innovators create certainty in a different way: predictable repayment.

BNPL players start the credit conversation at the beginning of the consumer’s shopping journey, not at checkout or as part of the end-of-the-month bill payment experience, long after purchases and purchase decisions have been made.

Consumers can see on a product page what a $150 or $7500 item might cost if paid over 3 or 4 or 12 or more equal monthly payments — before they checkout, before they get their statement twenty or thirty days later, or before they abandon a purchase because they don’t want to buy something without knowing first whether they’ll get themselves into financial trouble.

That’s what consumers say is the BNPL appeal.

Regardless of the financial profile of the BNPL customer, PYMNTS research over the last two years reports that BNPL users like the certainty of a payoff in full at the end of the term — and they like knowing that before committing to a purchase.

See also: 43% of US Adults Interested In BNPL for ‘Big Ticket’ Travel, Home Repair, Medical Purchases

For consumers with thin credit files or limited traditional credit options, BNPL turns funds in their checking account into installment loans with financial guardrails. For those with access to credit cards, BNPL is a convenient, sometimes zero-interest option to pay for an expensive purchase like jewelry, electronics, home goods or vacations, leaving their credit lines available as a cash cushion for other purchases.

Merchants like BNPL because it improves conversions, which is the name of their game.

A recent conversation with two well-established merchants over the last week emphasized that point. One merchant remarked that 30 percent of their sales are now made via BNPL pure plays — the other said it was 50 percent. Both said those numbers are increasing rapidly. They say that these BNPL purchases were made by consumers with credit card alternatives. Each of those merchants sell products that can cost as much as two, three to five thousand dollars for a single purchase.

One of those merchants also offers multiple BNPL logos on their checkout page to accommodate the brand affinity that users have to those providers, something more merchants also seem to be doing.

Their experiences are echoed by many other merchants I’ve spoken with over the last year about their adoption of BNPL and the momentum they see from consumers who like using it.

The One Question

In many ways, BNPL innovators have taken a page from the card issuers’ playbook. They’re issuing plastic or virtual cards that can be used anywhere a consumer wants to shop and buy any product that a consumer wants to buy. Acceptance, they rightfully concede, is critical to expand their addressable market of merchants and consumers — and ultimately, their payments volume and economic model.

They’re also creating their own shopping ecosystems of merchants that offer the payment method they like, want and know how to use. These innovators are birthing or expanding “super apps” that offer a broad array of financial services — including savings and direct deposit options — using their new credit narrative as the cornerstone for an acceptance network built on how to repay, not only how to finance what they buy.

In depth: Affirm Turns Its App Into a Super App

They’re doing that by using technology and real-time data to help consumers make those choices, including pre-approvals that offer clarity about what they can spend before they shop online or instore. Consumers get payments choice from a single provider with whom they are building trust and a different type of payment relationship.

Read more: Super Apps Proliferate, BNPL Sees More Competition and Grocers Boost Online Efforts

These innovations are irrelevant to merchants, who just see higher conversions and sales from consumers with multiple options for how to pay off purchases. For now, at least, they don’t complain about the haircut they take from the BNPL providers for that option. That will likely change — reports suggest, in fact, that fees are already coming under competitive pressure.

For example: Klarna CEO Says BNPL Competition Is Driving Down the Fees Paid by Retailers

At the same time, card networks and FinTechs are working with issuers to improve their BNPL experience today, leveraging existing credit lines to manage their risk and improve the user experience. For them, it’s the BNPL pure-pay user experience that they have to beat.

A final thought:

We’ve heard a lot over the last few years about FinTechs taking on the banks. There’s been a lot of innovation by FinTechs, for sure, but a mixed bag of uptake — particularly when it comes to those who are trying to beat the banks with little more than a mobile prepaid card.

But then came BNPL, which has turned out to be the biggest challenge yet to the credit and interchange revenue streams retail banks get from credit cards. How big, and how much of a threat potentially, I’ve written about before.

So far, banks have been slow to meet the challenge. How they do may tell us a lot about a how big a threat these FinTechs really are to traditional banks.

See also: The Buy Now, Pay Later Battle That’s Brewing