Buy now, pay later (BNPL) has become a part of everyday life for American consumers, and its popularity is still expanding. Twenty-nine million consumers in the United States leveraged BNPL to make purchases in 2021, and 59% of consumers said they would be willing to use third-party BNPL solutions.

Americans are branching out to more unusual BNPL use cases, such as education and medicine. One of the primary draws of BNPL is its lack of interest rates as long as the payments are made on time, and this makes it an attractive option for big-ticket purchases beyond just merchandise.

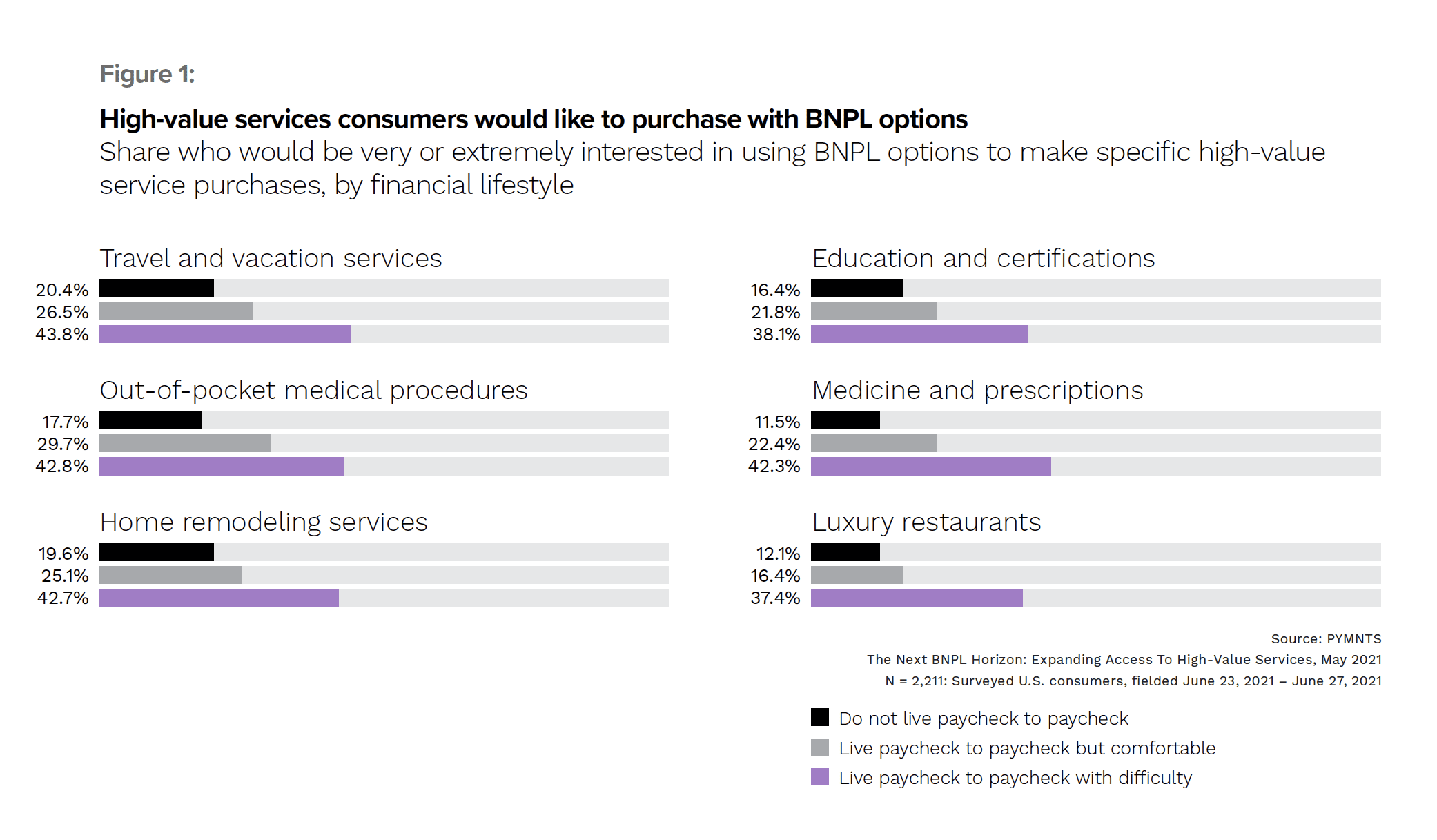

This month, PYMNTS explores how consumers leverage BNPL to pay for services rather than retail and the benefits of doing so.

Medical procedures, education and prescriptions are some of the most popular BNPL use cases. A recent PYMNTS study found that 59% of all U.S. consumers are living paycheck to paycheck, including 43% of those earning more than $100,000 per year. Forty-three percent of these paycheck-to-paycheck consumers said they would be interested in leveraging BNPL for out-of-pocket medical procedures, while 43% would use it for home remodeling services, 42% would use it for medicine and prescriptions and 38% would use it for education and certifications.

All told, 43% of consumers would prefer to use BNPL for high-value purchases, translating to approximately 111 million consumers. Eighty-three percent of those who agreed with this statement preferred BNPL over a credit card, with 34% saying they liked having a finite end to the payment terms, for example.

BNPL providers are exploring a number of new products to improve customers’ access to these services. Digital education merchant upGrad, for example, recently partnered with a BNPL provider to offer installment payments. The global eLearning market was worth $215 billion in 2021 and it is expected to grow 13% annually. BNPL provider Splitit has seen growth in the segment triple in the last few years, and its data shows students paid $1,500 over 8.5 installments in 2022, up from $1,240 over 7.3 installments last year.

Overseas customers are also exploring BNPL for access to services. Education payments are a growing concern in India, for example, where the eLearning market is valued at more than $1.96 billion, yet just 3% of the population has access to traditional credit services. BNPL companies aim to take advantage of this funding gap as well as the fact that 48% of students are currently paying for their education through installment payments. These companies hope to harness these individuals’ familiarity with installment payments to introduce them to BNPL.