Credit remains a lifeline for Generation Z — if they’ve got access to it in the first place.

To that end, PYMNTS data shows that younger consumers, specifically those born at the end of the Millennium until about 12 years old, wield their cards in force to satisfy their daily commerce needs.

As reported in the recent study, “Credit Card Use During Economic Turbulence,” a PYMNTS and Elan Financial Services effort, we found that 43% of Gen Z consumers have been using their cards more often. The increased use of credit dovetails with our separate findings that 66% of this cohort lives paycheck to paycheck. That ratio has moved up from a recent low of around 57% seen in September of last year.

Savings are of little succor here. Our data shows through the past year that Generation Z had among the lowest savings across the pantheon of those belonging to the paycheck-to-paycheck economy, consistently around $1,100 or so.

Despite the overall increase in spending on cards, we’re already seeing that there’s been some shifting away from nonessential categories.

The resumption of student loan payments looms as a further headwind to discretionary spending. We’ve found that the average Generation Z individual carrying student debt has about $14,000 in loans outstanding, representing about 4.3% of disposable income, which would put a crimp in spending over the near term. It’s important to note that the Federal Reserve’s definition of “disposable income” does not consider the real and ongoing expenses of paying for shelter, food and healthcare. Hence, the pressure on the proverbial pocketbook is real.

Generation Z has been cutting its use of subscription services, as the share of this demographic with subscriptions to Amazon Prime and Walmart+ has declined by mid-single digit percentage points From March to May of this year.

The data above spotlights that Gen Z — a group representing the future backbone of consumer spending, as careers are launched and grow, and as salaries (hopefully) grow, too — has been pressured to find efficient ways to juggle spending.

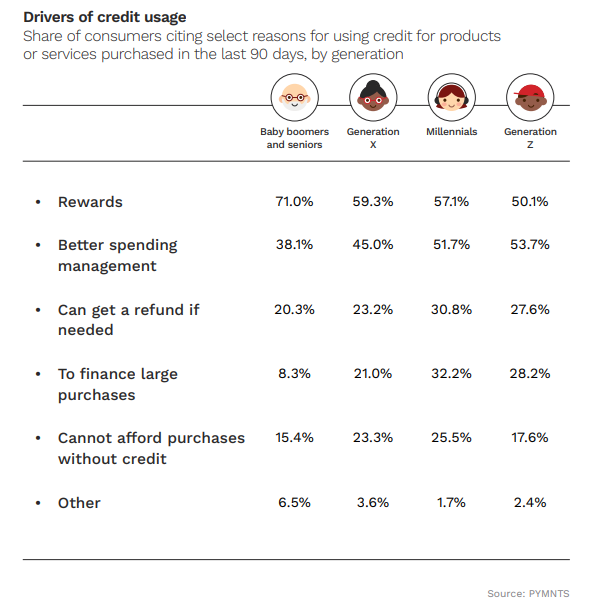

The findings in “The Credit Economy: How Younger Consumers Make Credit Decisions,” a PYMNTS and i2c collaboration, show that more than half of Generation Z credit card users has used cards for better spending management (the highest percentage among all generations we surveyed) as detailed in the chart below.

But 29% of Generation Z either doesn’t know their credit score or has no credit score to speak of, which hints that there are at least some constraints in the ability to obtain cards with favorable terms — or get them at all. In the meantime, some 14% of Gen Z consumers reported using buy now, pay later options to make purchases to get what they’ve needed in the past 90 days.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More