Consumers examining the debt they’re carrying — and the cost of servicing that debt — may be tempted to make the switch away from credit cards.

And there’s some evidence that the pivot has already begun.

In joint research conducted by PYMNTS Intelligence and Nuvei and as noted here, half of U.S. consumers tried using a new payment method in the past year, and 16% switched to a new one.

Digging a bit deeper, only 13% of consumers said credit cards were the new payment method they tried.

On the flip side of the equation, digital wallets are seeing relatively widespread uptake, having been used in 30% of what we might term “new” cases, which means that 3 out of 5 U.S. consumers who tried a new payment method in the last year did so with digital wallets.

Digital wallets, we found, offer convenience as consumers track their payments. Moreover, 4 out of 10 consumers who tried this method reduced the use of other payment methods after beginning their use of digital wallets.

Trailing, but still capturing some share are buy now pay later (BNPL) options, cited as a new payment method by 5% of consumers. And as reported in recent days, BNPL company Affirm reported a 28% increase in gross merchandise volume, reaching $5.6 billion compared to the previous year.

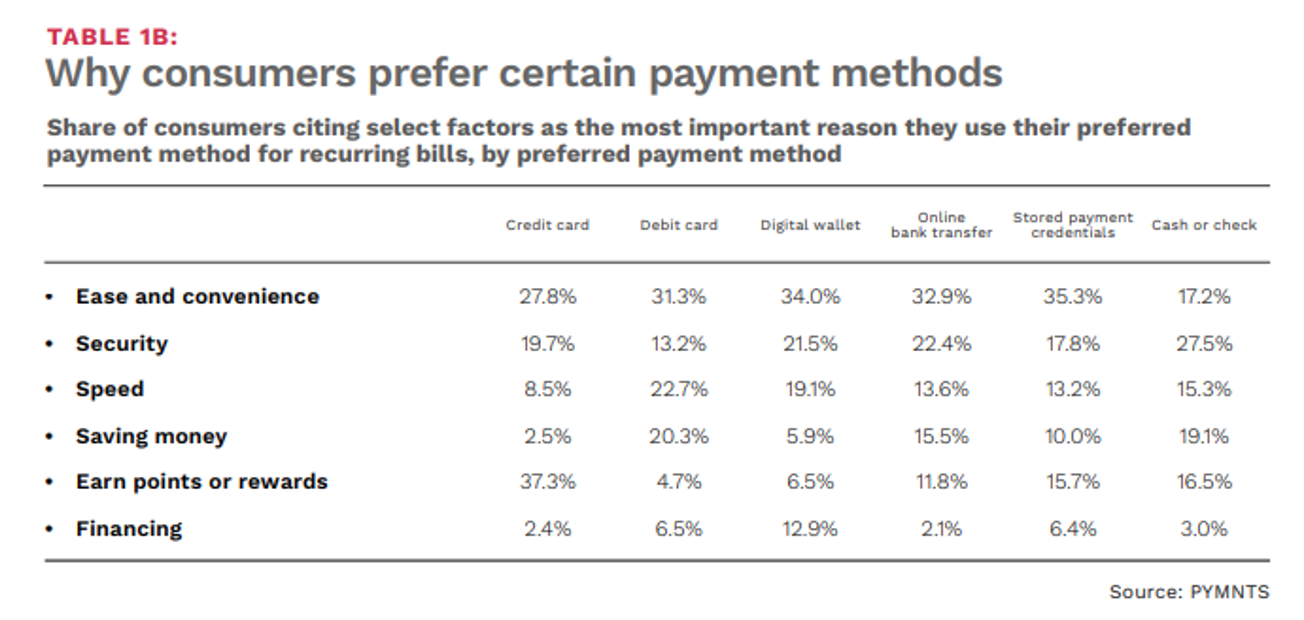

What Consumers Value in a Payment Method

It seems a number of factors are coming to bear on the use of digital wallets (and other options) at the expense of cards. As shown in the accompanying chart, more consumers cite speed and convenience as among the important factors in choosing digital wallets than they do with credit cards, and security too, as they satisfy their recurring payment obligations.

None of this is to say that credit cards will be supplanted by other payment methods, not entirely, of course. But the willingness to try new payment methods, and reduce reliance on entrenched ones, comes as the vast majority of us hold credit cards. PYMNTS Intelligence data has estimated that 74% of households surveyed have credit card debt and as many as 55% of consumers are revolving their credit card debt, with a third of consumers increasing their spend on credit cards through the past several months. Nearly half of Generation Z and millennial consumers have been shifting more of their spending onto their cards.

And in a high level view, the Federal Reserve has estimated that U.S. consumers hold $1.08 trillion in credit card debt, and that credit card balances jumped by $154 billion since 2022, the biggest increase since the bank began monitoring the data in 1999. The number of accounts in “serious delinquency,” at 90 days or more delinquent, has been on the rise. The sharpest increases in credit card delinquencies were seen among borrowers between the ages of 30 and 39.