Emergency expenses are a reality all consumers eventually face — and when economic headwinds and factors like rising prices enter the equation, these unexpected expenses can be burdensome, especially for credit-marginalized and younger consumers. Some consumers’ savings will not be enough to cover the cost of the unexpected, and not all consumers have rainy day savings. In times of adversity, these consumers must opt for other forms of payment, such as credit cards; loans; buy now, pay later (BNPL); and pawnshop loans.

Emergency expenses are a reality all consumers eventually face — and when economic headwinds and factors like rising prices enter the equation, these unexpected expenses can be burdensome, especially for credit-marginalized and younger consumers. Some consumers’ savings will not be enough to cover the cost of the unexpected, and not all consumers have rainy day savings. In times of adversity, these consumers must opt for other forms of payment, such as credit cards; loans; buy now, pay later (BNPL); and pawnshop loans.

PYMNTS found that consumers who have tried BNPL before are twice as likely as the average consumer to prefer it for emergencies. Although the shares are small, this suggests that BNPL is winning over users as an emergency tool. Additionally, credit-marginalized consumers — those consumers who have been rejected for credit at least once in the last year — are also more likely to prefer BNPL for unforeseen costs.

These are just some of the findings detailed in “The Credit Accessibility Series: Unexpected Expenses and the Demand for External Financing,” a PYMNTS Intelligence and Sezzle collaboration. This report draws on insights from a survey of 2,521 U.S. consumers conducted between Oct. 10 and Oct. 31 and explores how consumers deal with unforeseen expenses.

Other findings from the report include the following.

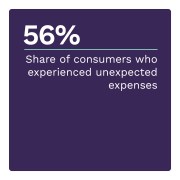

In the past year, most Gen Z and credit-marginalized consumers have faced unexpected expenses that cost almost as much as or more than their average savings balances.

In the past year, most Gen Z and credit-marginalized consumers have faced unexpected expenses that cost almost as much as or more than their average savings balances.Unexpected expenses are straining savings levels, as 56% of all consumers surveyed had a costly and unexpected expense in the past year, averaging $5,500. The situation is worse for Generation Z consumers, 7 in 10 of whom faced unexpected expenses that cost almost as much as or more than their current average savings, and credit-marginalized consumers, 8 in 10 of whom faced unexpected expenses that were as much as or more than their current average savings.

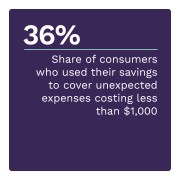

While 36% of consumers used their savings to cover unexpected expenses costing less than $1,000, most used a credit product. Credit cards, cash advance loans, BNPL and overdraft loans topped the list of credit products used. Credit products are not only preferred by consumers facing smaller emergencies but also by those with smaller reserves.

More than 80% of credit-marginalized consumers faced further credit access issues due to these unforeseen expenses.

More than 80% of credit-marginalized consumers faced further credit access issues due to these unforeseen expenses. Financial hardship is an ever-present reality for the credit marginalized, and emergencies add to this reality. Survey data supports this statement, as 56% of all consumers and 81% of credit-marginalized consumers who faced unexpected costs in the past year also experienced further credit issues as a result. The primary effect of unforeseen costs is a decline in credit scores.

Although “saving for a rainy day” is advice most consumers consider, savings levels continue to decline due mostly to economic hardship and persistent inflation, and many consumers have to use credit products for unexpected expenses. Download the report to learn more about how U.S. consumers are financing emergency expenses.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More