This financial tightrope is not limited to those with lower incomes; it extends its grip to high-income earners as well. In fact, among those earning over $100,000, as many as 44% find themselves in this paycheck-to-paycheck cycle.

During these financially challenging times, having a savings cushion can be a lifesaver. However, many consumers still struggle to set aside money for a rainy day despite dedicated efforts, across all income levels, to effectively manage finances.

On average, consumers deplete 67% of their available savings, with such depletions occurring, once every four years on average. For those living paycheck to paycheck, this recurrence is even more pronounced, occurring as frequently as once every 2.5 years.

These are some of the findings detailed in the latest edition of New Reality Check: The Paycheck-to-Paycheck Report entitled “Savings Deep Dive Edition,” which draws insights from a survey of more than 3,600 consumers to assess their capacity to maintain their savings in the current economic environment, particularly when confronted with significant expenses.

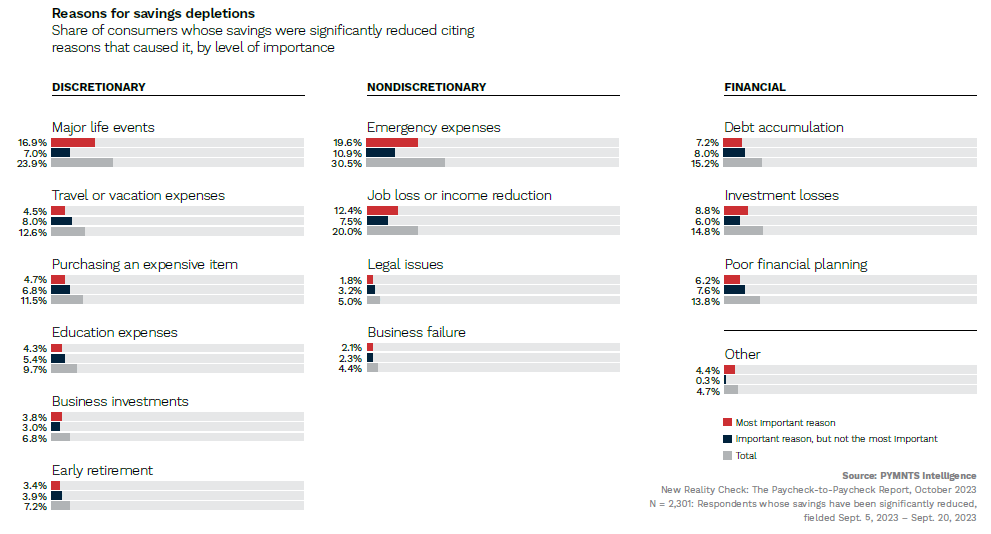

When it comes to reasons behind consumers depleting their savings, emergency expenses, such as unexpected medical bills or home repairs, are the primary cause, accounting for 31% of cases where savings are depleted, per data from the joint PYMNTS Intelligence-LendingClub study.

Major life events, including weddings or buying a home, contribute to 24% of savings reductions. Other factors, such as travel expenses, investment losses and discretionary spending also significantly impact consumers’ ability to save.

Job Losses Impact Savings

Examining the data further reveals that job loss or a reduction in income is another significant reason for depleting savings, with 1 in 5 consumers identifying it as a contributing factor. This trend is expected to persist and further erode consumers’ savings as job losses continue to rise across various sectors.

Just last week (Oct. 25), U.K. banking giant Barclays announced that it is trimming its U.S. consumer banking division as it looks to lower costs, resulting in the layoff of 3% of its staff. This comes amid reports of staff reductions at some of America’s biggest banks, including JP Morgan, Citi and Wells Fargo, where about 20,000 jobs are at risk due to the impact of high interest rates.

Tech layoffs, which in 2022 were nearly double the figures seen in the sector during the pandemic, continue to persist. Meta, the parent company of Facebook, is planning to trim its workforce, PYMNTS wrote earlier this month. The move follows another workforce reduction initiative at the company, which has already led to the loss of about 21,000 jobs since November 2022.

Nokia also recently disclosed its plans to slash up 14,000 employees, following a nearly 70% decline in quarter profits. Additionally, major tech firms like Robinhood, Qualcomm and LinkedIn have also announced similar job cuts.

With job cuts showing no sign of slowing down across various industries, the need for emergency funds and effective financial planning to handle unexpected expenses is more critical than ever, particularly for consumers living paycheck to paycheck, as noted in the PYMNTS Intelligence report.

By prioritizing savings and implementing sound budgeting strategies, consumers can work towards achieving greater financial stability, enabling them to better navigate planned and unforeseen expenses, especially in the event of job losses or income reductions.