Consumers conducted nearly everything from their grocery shopping to making mortgage payments virtually over the past 17 months, and their newfound comfort with digital banking features is not likely to dissipate even as brick-and-mortar branches fully reopen.

Individuals are changing the way they interact with their financial institutions (FIs) more broadly — including credit union (CU) members — asking for more digital support, although not abandoning in-person experiences at brick-and-mortar branches yet.

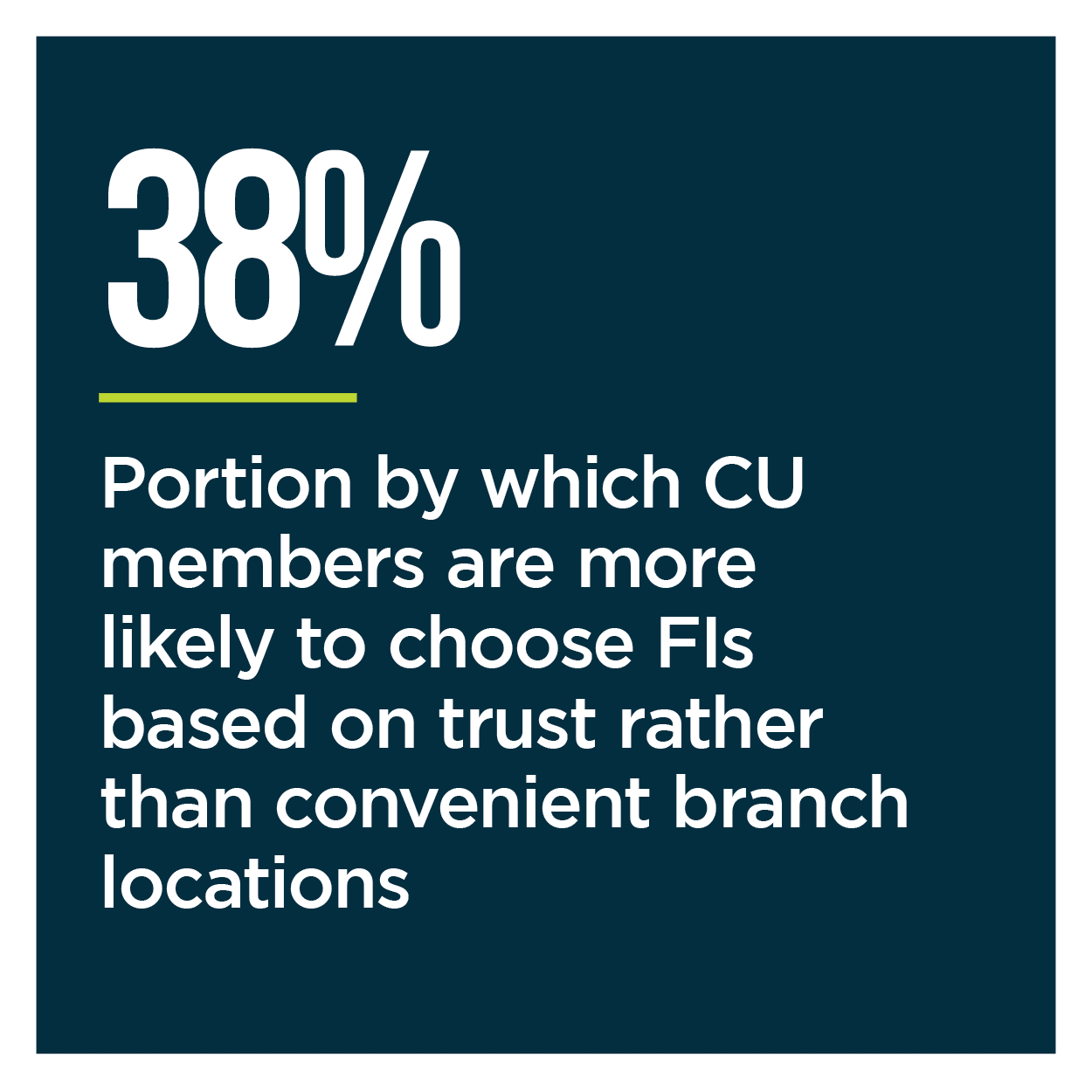

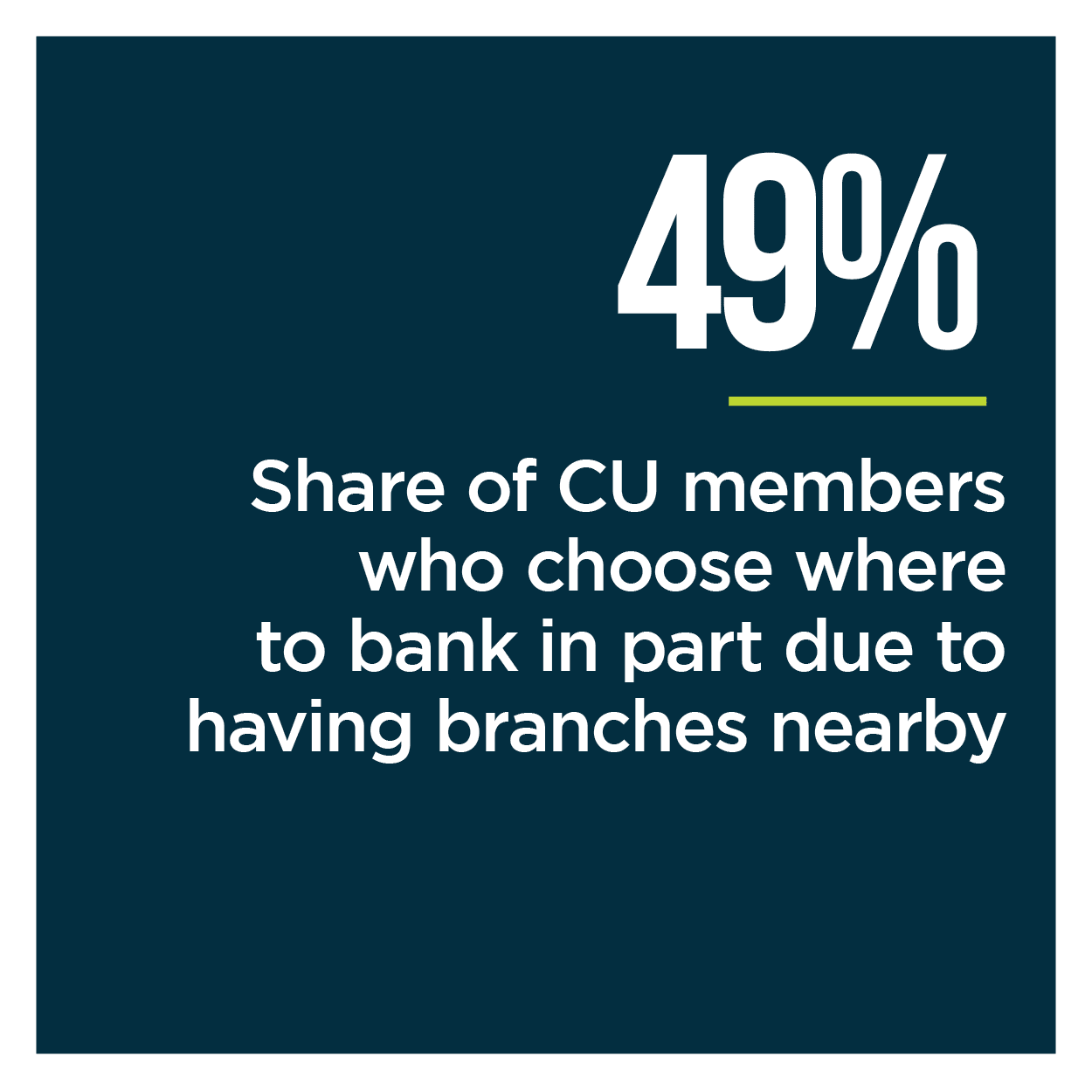

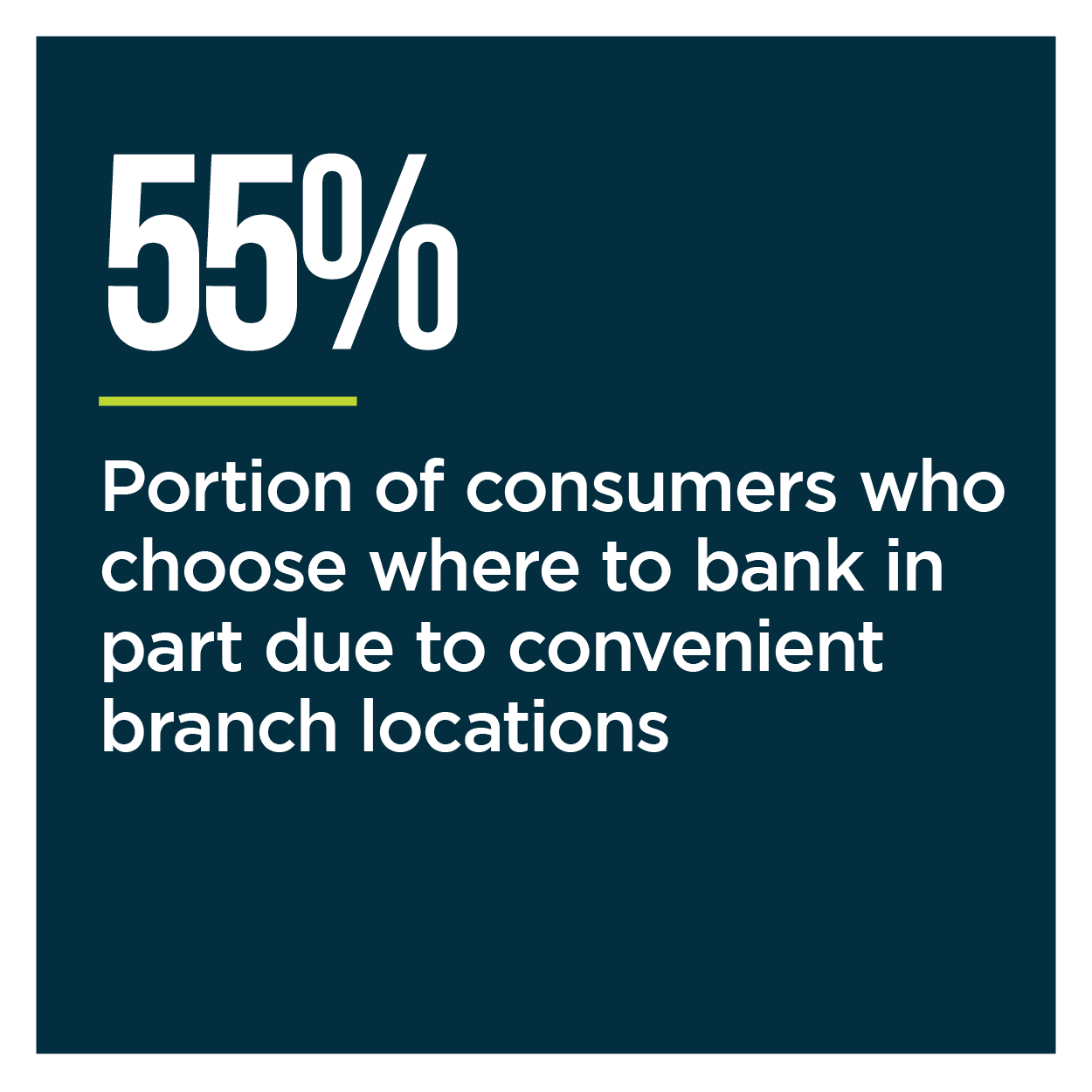

PYMNTS data showed that while online banking figures are rapidly expanding, CU members still want physical branches to be easily accessible should they have the desire to conduct banking tasks in person. Forty-nine percent of CU members choose their financial entities based on whether branches are conveniently located for them, indicating brick-and-mortar branches still play an integral role in the financial lives of many. The continued migration to digital tools may mean that members are expecting to bank at branches a little differently, however.

In the latest “Credit Union Tracker®,” PYMNTS more closely examines how the pandemic impacted members’ banking habits, especially concerning brick-and-mortar branches, and what this means for CUs’ brick-and-mortar branch strategies. It also analyzes what tools and technologies may prove critical for CUs as they look to innovate both their branches and their digital channels.

Around the Credit Union World

Consumers worldwide have shifted their banking habits, turning to digital tools not only to make routine deposits or check their account balances but to make payments at physical retailers. CUs in multiple markets are therefore moving to adjust both their online and brick-and-mortar tools for a world where the use of cash or other manual payment methods is slimming down. The Canadian Interior Savings Credit Union has moved away from accepting cash at one of its branches, for example. The move was prompted by the growing number of members who are tapping self-service or fully-digital products to make payments and conduct banking activities. This could give the CU an advantage over competitors as members continue to migrate to such tools and payment methods.

CUs are also moving to develop innovative digital services for their customers as they also move to redesign branches, creating services to entice new members as adoption of mobile and online banking increases. Lumin Digital, a PSCU company, announced a partnership with Consumers Credit Union for a pilot of a digital account opening product, for example. The feature will enable potential members to apply for accounts and to onboard virtually, as well as support digital payments once the onboarding process is complete. Member onboarding can be finalized in less than five minutes, according to statements by Consumers CU, including identity verification of the applicants.

Creating both seamless digital banking tools  and supporting accessible branches is becoming more critical for CUs in the United States, especially as the country’s regulators take a closer look at how to expand financial access to historically underserved communities. Approximately 6% of U.S. households remain unbanked, a population that still remains highly dependent on branches for their financial needs. The U.S. House Financial Services Committee convened in July to consider a proposal that would broaden field of membership (FOM) restrictions for CUs to create more space for unbanked or underbanked consumers. The move would allow federal CUs to expand FOMs to such communities, an effort that could potentially help stimulate future financial inclusion.

and supporting accessible branches is becoming more critical for CUs in the United States, especially as the country’s regulators take a closer look at how to expand financial access to historically underserved communities. Approximately 6% of U.S. households remain unbanked, a population that still remains highly dependent on branches for their financial needs. The U.S. House Financial Services Committee convened in July to consider a proposal that would broaden field of membership (FOM) restrictions for CUs to create more space for unbanked or underbanked consumers. The move would allow federal CUs to expand FOMs to such communities, an effort that could potentially help stimulate future financial inclusion.

For more on these and other stories, visit the Tracker’s News & Trends.

How the Pandemic Changed Credit Unions’ Brick-and-Mortar Branch Strategies

Branch-based banking has been on the decline, leading many executives to question their continued role in the financial world. Many individuals are now conducting routine payments or banking tasks online rather than visiting their chosen FIs or CUs in person, but the branch — if carefully designed — can still occupy a key space in members financial lives.

BECU has built 16 new branches for its nearly 1.1 million member base since 2016, for example, with only two of their 60 branches overall staffed with tellers. The rest use “consultants” who can provide members with advice, while daily banking tasks can be handled online or via mobile app, explained Travis Simpson, the CU’s senior vice president of contact centers and wealth.

To learn more about why CUs must change their brick-and-mortar branch approach to meet the needs of today’s members, visit the Tracker’s Feature Story.

Deep Dive: Why CUs Should Implement Self-Service Features to Meet Digital-First Members’ Changing Branch Needs

The adoption of digital banking tools skyrocketed in 2020, with consumers and businesses alike tapping online channels first and foremost to fulfill their banking needs. This has led to a corresponding decline in the use of brick-and-mortar branches — following existing trends — but this does not mean individuals want to give up their branches entirely. Most consumers still indicate the desire to live within 15 minutes of a bank branch, for example. Retaining the loyalty and engagement of CU members at such branches requires financial entities to think differently about how they are designed and what tools may prove useful to today’s digital-first consumers, however.

To learn more about how integrating self-service technology into their branches can help CUs engage digital-first members, visit the Tracker’s Deep Dive.

About the Tracker

The “Credit Union Tracker®,” done in collaboration with PSCU, is the go-to monthly resource for updates on trends and changes in the credit union industry.