CU members across the United States have gone online to bank and transact, and most have no intention to going back to in-person banking as it was. The result is an unprecedented need for innovative, easy-to-use digital banking options that match members’ new online banking habits as physical branches’ importance wanes.

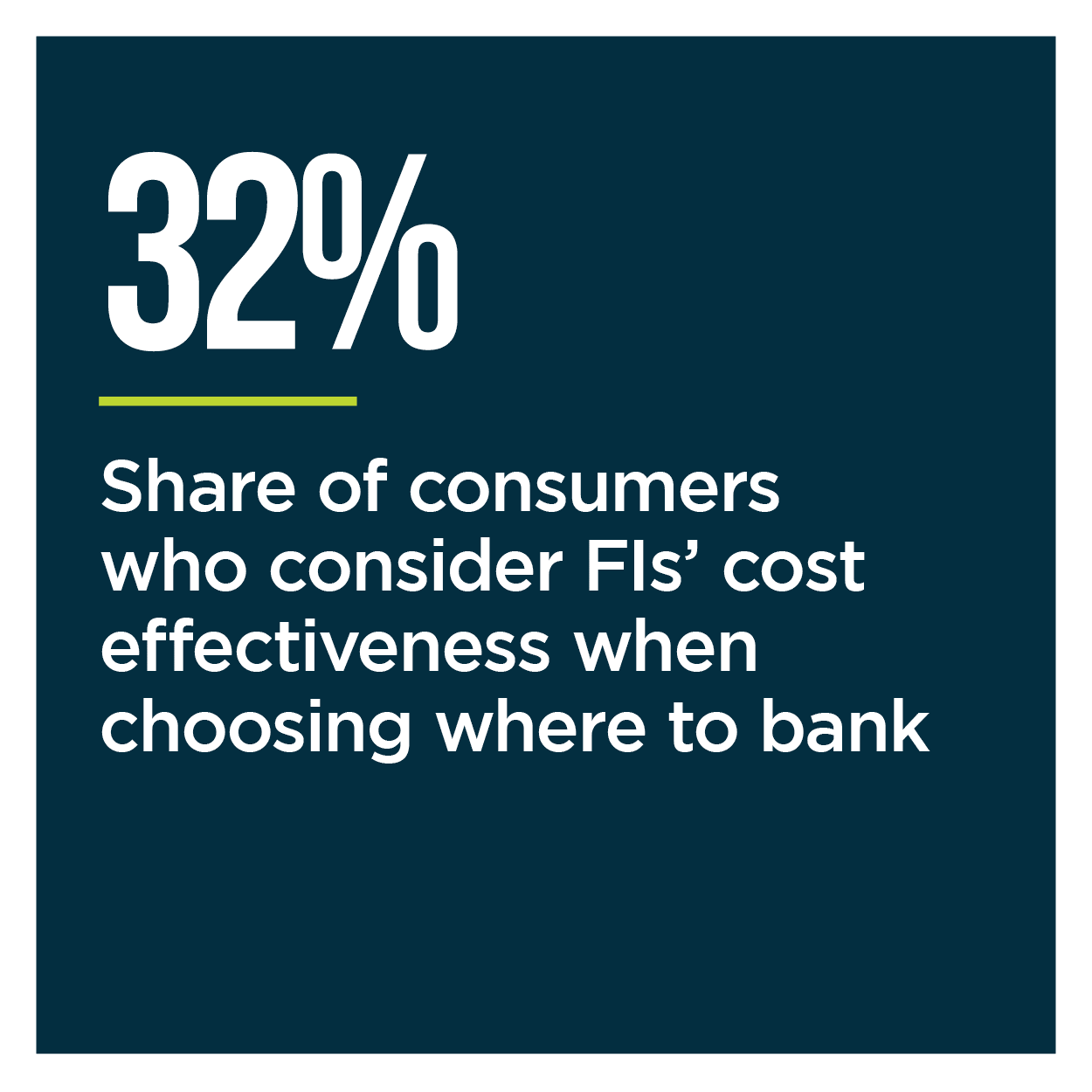

Members are 17 percent less inclined to choose where to bank based on location than they were just two years ago, in fact, signaling a d ire need for CUs to invest in digital capabilities. But are CUs rising to the occasion and delivering the digital innovations that their members need and expect?

ire need for CUs to invest in digital capabilities. But are CUs rising to the occasion and delivering the digital innovations that their members need and expect?

This is just one of the questions that PYMNTS, in collaboration with PSCU, set out to answer in the 2021 edition of the Credit Union Innovation Study. We surveyed a census-balanced panel of 5,239 U.S. consumers, 100 CU decision makers and 50 FinTech executives between April 26 and May 4 to learn how the 16 months prior to the survey changed their expectations regarding their financial institutions (FIs) and whether CUs are meeting their members’ shifting demands.

PYMNTS research shows that most CUs have been rising to the challenge to innovate the digital products and services that their members expect. CU members are more satisfied with CUs’ innovation performances than they have ever been, with 80 percent now saying that they believe their CUs innovate “somewhat” or “very” well.

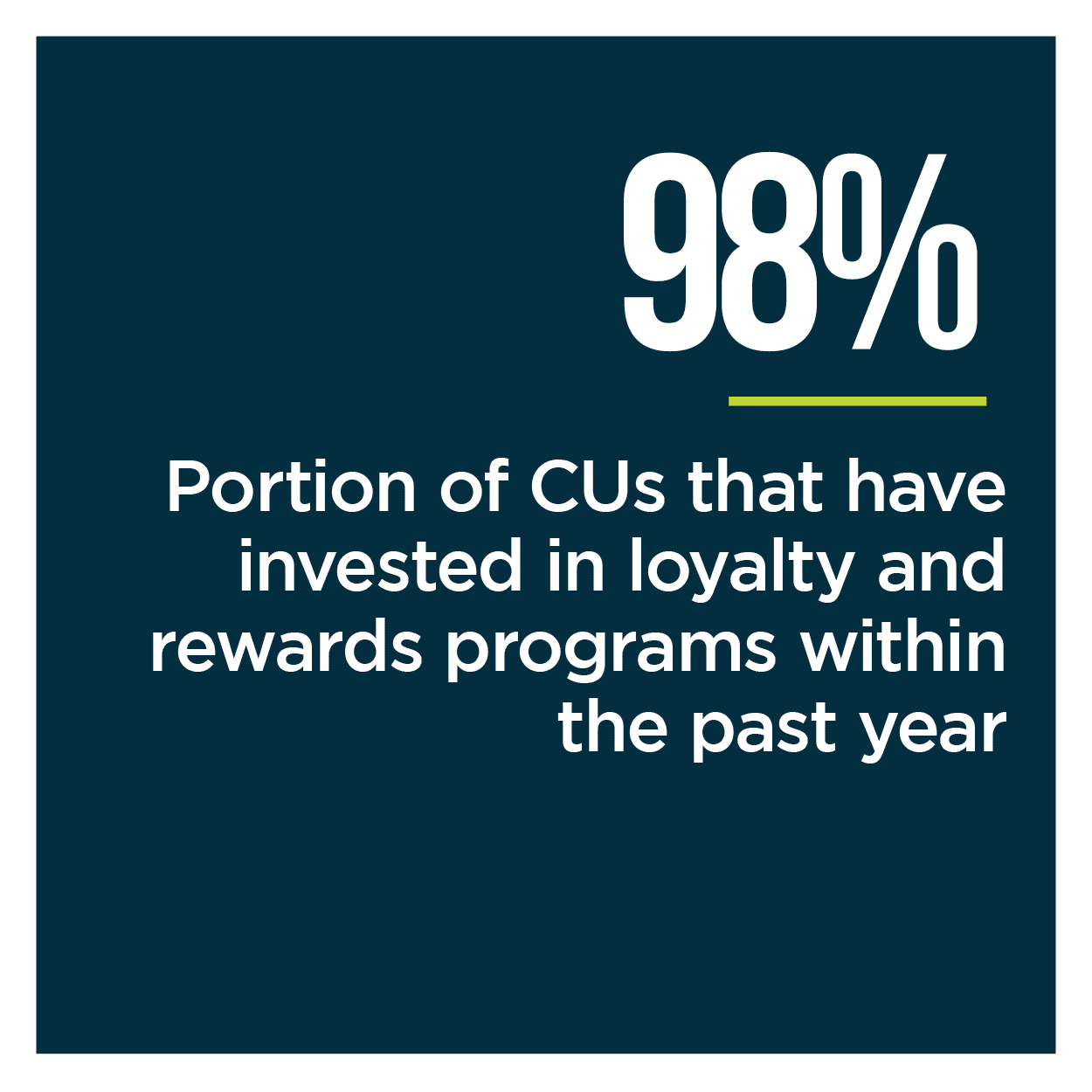

According to their members, CUs are not only rolling out new products and services more effectively, but also investing more in the types of innovations that members want to use. Ninety-eight percent have invested in loyalty and rewards innovations over the past year, for example, and 93 percent have invested in security, authentication and digital identity innovations during that time.

more effectively, but also investing more in the types of innovations that members want to use. Ninety-eight percent have invested in loyalty and rewards innovations over the past year, for example, and 93 percent have invested in security, authentication and digital identity innovations during that time.

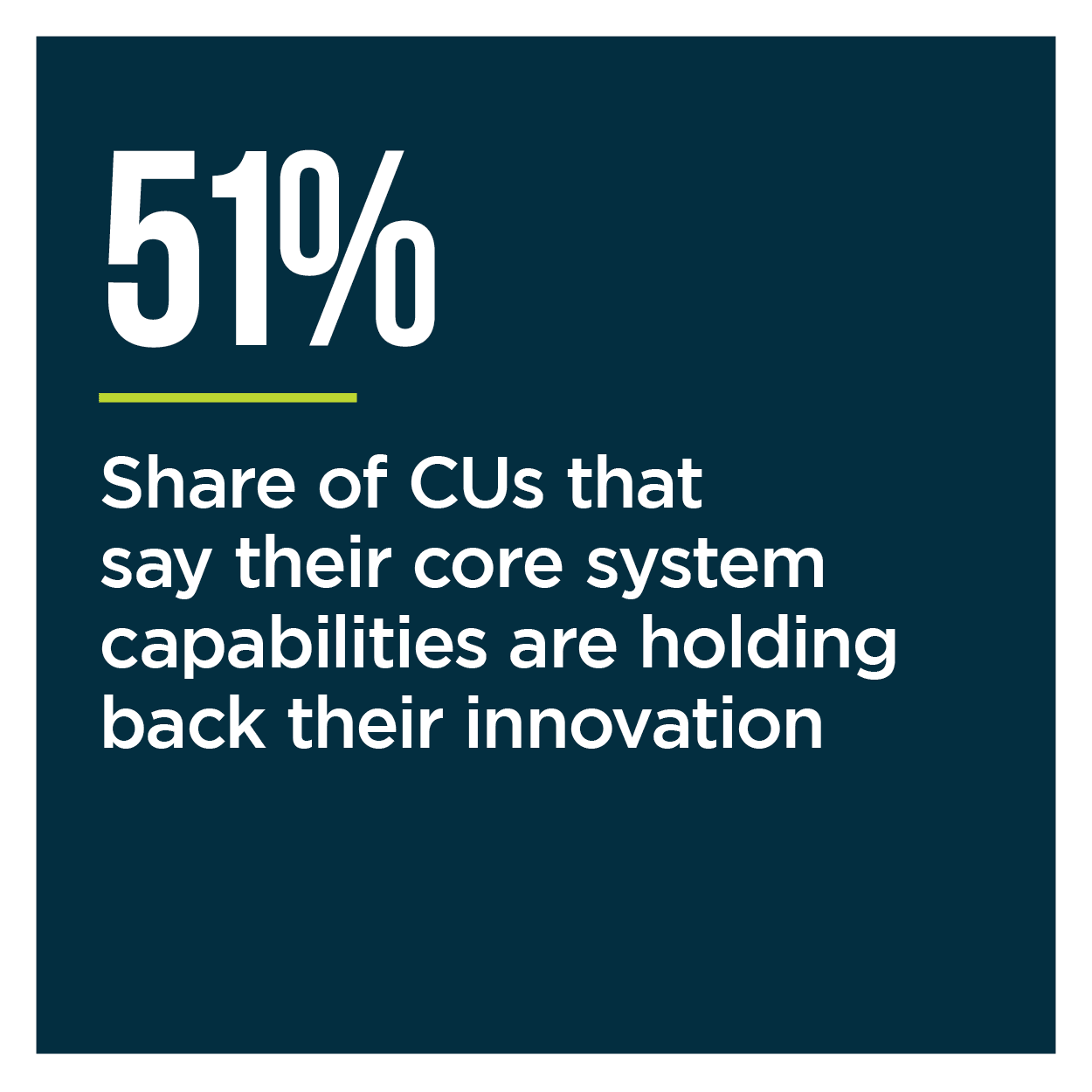

There are nevertheless several key hurdles that CUs must still overcome to realize their full innovation potential, with limited technical capabilities being at the top of the list. Sixty-three percent of CUs say they lack the data analytics capabilities they need to create personalized member products, and 51 percent say their core systems’ capabilities do not allow them to innovate the types of products needed to meet members’ expectations.

These are only of the few factors holding CUs back from innovating as quickl y and effectively as they must to compete in this new, digital ecosystem. The Credit Union Innovation Study provides a more comprehensive overview of how CUs can optimize their innovation effectiveness.

y and effectively as they must to compete in this new, digital ecosystem. The Credit Union Innovation Study provides a more comprehensive overview of how CUs can optimize their innovation effectiveness.

To learn more about the innovation struggles CUs are facing — and what they can do to overcome them — download the report.

The bar on credit union (CU) innovation is higher than ever.

The bar on credit union (CU) innovation is higher than ever.