Credit unions (CUs) are well-suited to the unique needs of small businesses which struggle to find the services they need through other financial institutions (FIs), such as small loans with less return for lenders. Overall, members already have a high interest in business lines of credit through their CUs, and CUs can also leverage their  reputations for personalized service and high member satisfaction rates to attract small business owners. Coupled with better terms and services tailored to small business needs, the strengths of CUs fit well with the growing banking needs of small businesses.

reputations for personalized service and high member satisfaction rates to attract small business owners. Coupled with better terms and services tailored to small business needs, the strengths of CUs fit well with the growing banking needs of small businesses.

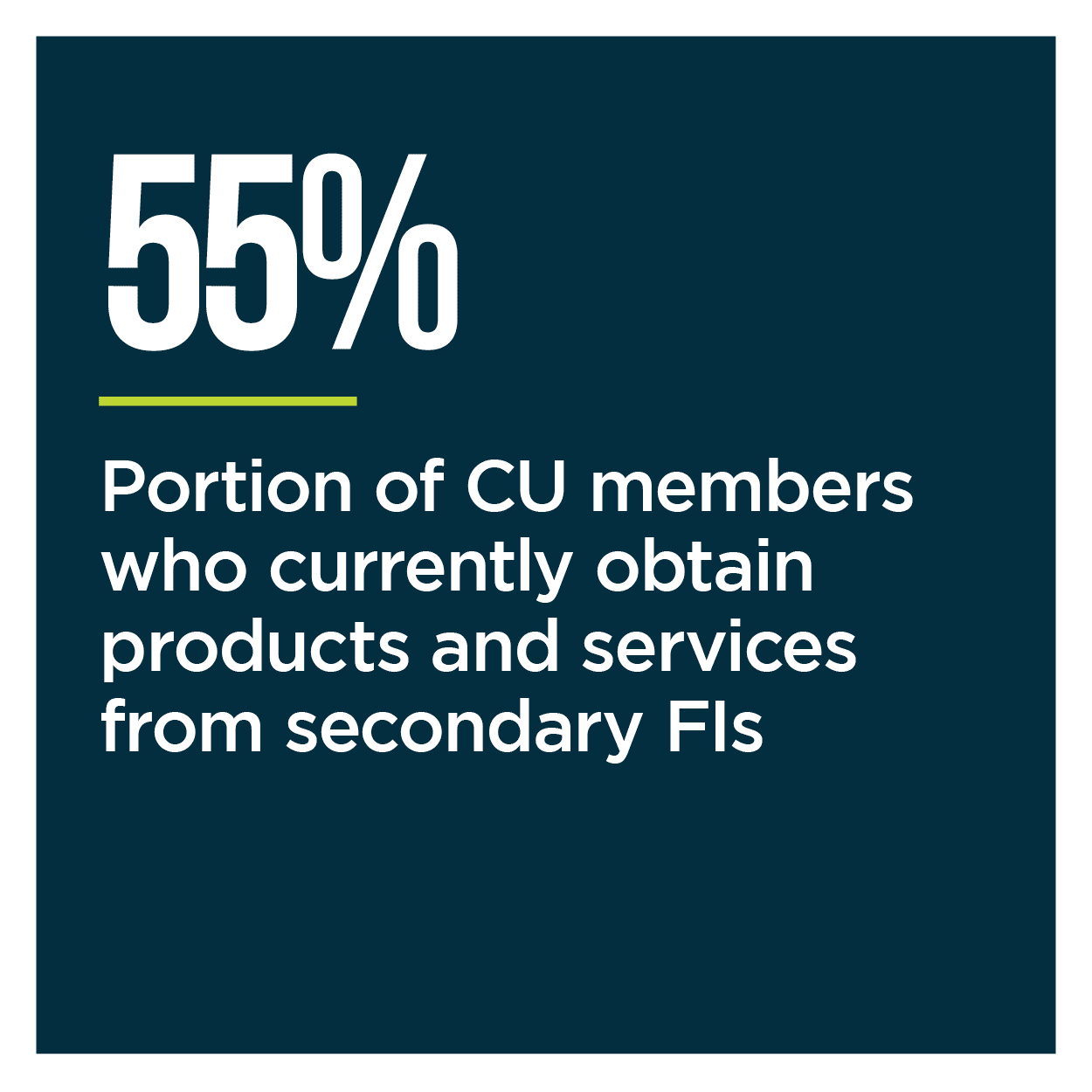

The challenge for CUs is in taking what they have and augmenting it with digital banking tools that add to — rather than replace — the special relationship CUs have with their members. Digital banking is important to consumers, as the pandemic has forced even those who have resisted digital experiences in the past to familiarize themselves with the convenience of online and mobile. Forty percent of adults would change FIs in pursuit of a better digital experience that gives them more functionality. Already, 11% of CU members are looking for products from FIs that offer better online account management than they can get through their CU.

The latest edition of the “Credit Union Tracker®” examines how CUs can make the most of digital banking technology to ensure they are offering members the best possible services while still retaining the personal touch that sets CUs apart from other FIs.

Developments From Around the World of Credit Unions

New York state has opened its Excelsior Linked Deposit Program to CUs, making it easier for them to offer low-interest loans to small businesses. Under the program, New York provides funding to enable a lower interest rate for the first four years of a small business loan. The state deposits the loan amount with the CU, accruing interest at a lower rate. The program intends to is to bridge “equity gaps” that prevent traditionally marginalized communities from starting and developing small businesses.

New York state has opened its Excelsior Linked Deposit Program to CUs, making it easier for them to offer low-interest loans to small businesses. Under the program, New York provides funding to enable a lower interest rate for the first four years of a small business loan. The state deposits the loan amount with the CU, accruing interest at a lower rate. The program intends to is to bridge “equity gaps” that prevent traditionally marginalized communities from starting and developing small businesses.

Around the world, CU membership grew 29% in 2020, according to a study from the World Council of Credit Unions. Across 118 countries, CUs now have more than 375 million members. The significant increase was attributed to digital initiatives and pandemic-driven financial assistance drawing in new members, as well as ongoing efforts to ensure existing members are retained.

Heading into the holiday season, consumer habits showed signs of both optimism and uncertainty. The October PSCU Payments Index attributed a decrease in credit card delinquency and an average rise in credit scores, in part, to government stimulus payments distributed in relation to the pandemic. At the same time, credit spending increased 16%, while debit spending was also up 13%, despite supply chain interruptions. The cost of living is also rising, with increased inflation and rising commodity prices.

For more on these stories and other CU developments, check out the Tracker’s News and Trends section.

Truliant Federal Credit Union on Combining Personalized Service With Digital Banking

Small business owners may not receive the personalized service they want from larger FIs, and the loans they need may even be too small to make it worth the time of those organizations. Credit unions are well-suited to fill that need.

Small business owners may not receive the personalized service they want from larger FIs, and the loans they need may even be too small to make it worth the time of those organizations. Credit unions are well-suited to fill that need.

In this month’s Feature Story, Jeff Hibbard, senior vice president of digital experience and business transformation for Truliant Federal Credit Union, discusses how CUs can find a balance in providing in-person services and digital self-service to meet the unique needs of small businesses in the communities they serve.

Deep Dive: Meeting Small Businesses’ Lending Needs

Despite consistently ranking well-above other FIs in terms of borrower satisfaction and being positioned prominently in their communities, CUs tend to have one of the smallest shares of total small business loans. As small businesses flocked to apply for Paycheck Protection Program loans during the pandemic, just a fraction of those loans were taken out through CUs.

This month’s Deep Dive delves into how CUs can position and present themselves to attract more business banking, both from within and without their membership.

About the Tracker

The “Credit Union Tracker®,” a PYMNTS and PSCU collaboration, examines the latest trends and developments shaping the CU space and how CUs can attract and retain small business consumers.