Sandwiched between millennials and baby boomers (and aged 43 to 58 as of 2023), this demographic, PYMNTS has found, has been most affected by the rising tide of inflation. This is perhaps due to one other sandwiched quality: their double financial duties as caretakers both for children who may not yet be able to support themselves as well as their aging parents or other relatives.

It is likely due to these constraints that Gen X has the highest share of surveyed consumers whose ability to save has decreased year over year, at 37%. And with 43% of Gen Xers serving as their household’s main breadwinner, inflation combined with typical financial stresses and holding the financial responsibility for multiple generations has put Gen X in a precarious position.

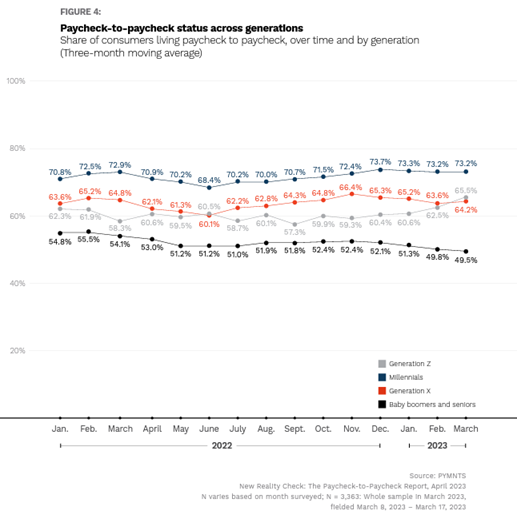

The effects of these stressors may be best illustrated in PYMNTS’ April collaboration with LendingClub, “New Reality Check: The Paycheck-to-Paycheck Report.”

Although one would expect Gen X to have carved out relative financial stability, the above chart illustrates that this generation’s financial lifestyle more resembles Gen Z or millennials than baby boomers and seniors. Members of Generation Z are just starting out in their careers, and it makes sense that around two-thirds would live paycheck to paycheck, but the Gen Z and Gen X lines are fairly intertwined. Moreover, the marker of 64% of Gen X living paycheck-to-paycheck is even potentially a bit misleading, as for most of the time since January 2022, Gen X has demonstrated more financial instability than Gen Z (and thus higher paycheck-to-paycheck numbers). Although theoretically earning more than younger generations in similar employment, it is very likely that their possible increased financial responsibilities may make it much harder for Gen X to get by.

Gen X’s sandwiched status could also be one reason behind their higher share of student loan debt. The generation’s average outstanding loans are $43,438, and payments represent 8.8% of their disposable income. This is much closer to baby boomer and seniors’ average of $44,364 than the next lesser amount, millennial’s $33,173. One reason for this could be that this generation is both responsible for paying off their own lingering student loans as well as possibly subsidizing their own children’s loans.

However, per the Education Data Initiative, Gen X carries an outsized burden of the national student loan debt at 39% of the country’s total. This high national share plus high individual repay amount means extra pressure overall may be put on Gen X as student loan payments are set to resume.

On a broad scale, this could be tough news for retailers and services catering to Gen X needs, as they will presumably soon have even less income to spend with. And although only time will tell what happens with this group in the coming months, the data seems to suggest that Gen X could find themselves cash-strapped longer than other age demographics.