Item-level receipt data provided by the right financial institution (FI) or FinTech can be a valuable merchant tool for customer engagement. It can offer fraud solutions, streamline expense management, monitor consumer spending behavior and be used for card-linked loyalty programs. With the latter, retailers and merchants can deliver hyper-personalized rewards offerings at a category or even product level.

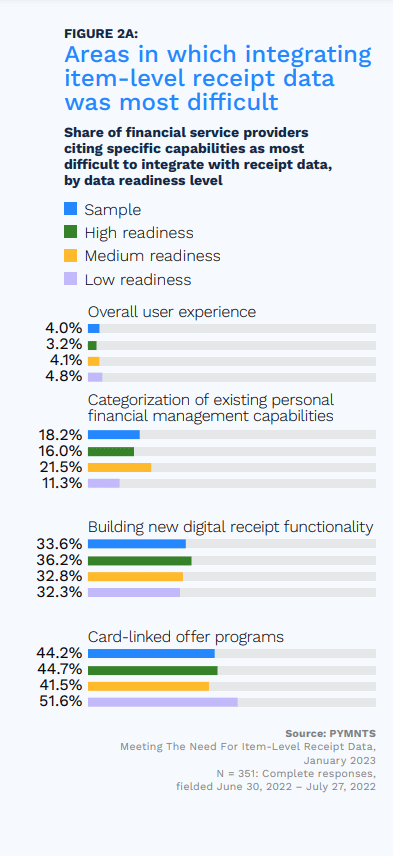

The latest PYMNTS/Banyan collaboration, “Meeting The Need For Item-Level Receipt Data: How Integration Enables Innovation,” noted that among all these features, using item-level receipt data within a card-based loyalty strategy seems to be the hardest for most FIs and FinTechs across all readiness levels to fully integrate — even more challenging than building new digital receipt functionalities.

Data readiness — the degree to which firms are prepared to utilize this valuable data — makes a clear difference in firms’ interest in implementing receipt data for loyalty offers. PYMNTS’ data reveals that 64% of firms with high data readiness are very or extremely interested in using receipt data for loyalty and shopping offers. In comparison, 5% of firms with low data readiness and 21% with medium data readiness say the same. In other words, firms well-positioned to reap the benefits of item-level receipt data are most likely to want to do so. These banks tend to be large, as 55% of big banks cite high readiness, compared to 28% of banks with assets less than $25 billion who say the same.

There is a similar correlation in the FinTech sector between assets and readiness, with 50% of large sector players being highly data ready and a scant 8% of firms with annual revenues below $25 million claiming the same. FinTechs are more likely to view integrating item-level receipt data into preexisting card-linked offerings as most challenging than FIs, at 46% versus 40%, respectively.

In an interview with PYMNTS’ Karen Webster, Jehan Luth, CEO of the FinTech Banyan, explains the importance of integrating card-linked offers with item-level receipt data. “I think card-linked offers have been a rather blunt instrument in a retailer’s marketing toolkit. One of the biggest reasons it’s a blunt instrument is because as a retailer, I cannot drive traffic to certain items. Instead of traditional loyalty offerings that may not be consumer-personalized, the overlaying of SKU-level data or item-level data in rewards and offers makes card-linked offers a much more versatile and powerful tool in the toolkit for retailers. Now I can drive traffic to certain categories within the store, or certain items within a store.”

Candy manufacturer Mars is one example of item-level receipt data being used this way. In October, Mars announced a partnership with the rewards app Fetch. The resulting program allows participating consumers to earn points towards company products when customers send in pictures of their receipts that include Mars products. Through program participation, Mars can gain a range of insights into their customers’ behavior, such as the time of day these purchases are usually made and what other items may also be bought alongside Mars products.

Tech-forward merchants seeking to innovate their card-linked loyalty offers may consider seeking a financial partner who doesn’t find the tools they need too difficult to integrate.