Financial institutions (FIs) have generally found fraud and financial crime to be continually more sophisticated. The rise of digital banking and ever-faster digital payment methods have accelerated this phenomenon. As a result, banks have had to elevate their systems and processes to find ways to stem the growth in fraudulent transactions — and the resulting uptick in financial losses.

FIs are increasing investments and deployments of machine learning (ML) and artificial intelligence (AI) to combat growing fraud. Forty-eight percent of FIs are adding or will add new technology in the next year — especially the largest banks. FIs using these technologies already recognize them as powerful tools in stemming fraudulent transactions. Those currently using ML or AI technologies suffered, on average, 30% fewer transactions that resulted in fraud losses in the last 12 months than those that do not use these technologies.

These are just some of the findings detailed in “The State of Fraud and Financial Crime in the U.S.,” a PYMNTS Intelligence and Hawk AI collaboration. This report examines the state of fraud and financial crime FIs experienced in 2023 compared to 2022, including the rising costs of fraud and what actions they have taken to mitigate it. Researchers collected 200 responses from executives working at FIs with assets of at least $1 billion between March 29 and June 16.

Respondents also participated in PYMNTS Intelligence’s 2022 survey on fraud experienced by FIs. In 2022, all sampled FIs had assets totaling more than $5 billion. In 2023, sampled FIs included 108 FIs with assets totaling more than $5 billion and 92 FIs with assets between $1 billion and $5 billion. Respondents were executives with deep knowledge and leadership responsibilities in the following areas: fraud and risk operations, fraud strategy or fraud analysis.

Key findings from the report include the following:

Key findings from the report include the following:

More than 40% of banks in the U.S. experienced increased fraud relative to 2022 figures — resulting in more fraudulent transactions and double the amount of fraud losses.

Fraud remains a top challenge, even as fraud rates have remained stable for many FIs in 2023 relative to 2022 figures — a year in which nearly three-quarters of FIs experienced increased fraud. Approximately 55% of sampled institutions report that all fraud measurements remained constant in 2023 versus 2022, while roughly 44% of FIs report that all fraud measurements increased in 2023.

While misuse of account information is still the leading type of fraudulent activity, each FI lost nearly half a million dollars on average related to scams alone in 2023.

Using the Federal Reserve’s Fraud Classifier Model, data shows that rates of unauthorized fraud surpass authorized fraud for all financial institutions, with 61% of fraudulent transactions coming from unauthorized party fraud — the type of fraud that occurs when external actors take over or compromise credentials to commit fraud. The misuse of account information — consisting of digital payment fraud and physical forgery — remains the leading source of fraud, with each FI losing an average of $1.4 million to the strategy in the last year.

FIs have invested in ML and AI to address the increase in fraud, yet smaller FIs lag in adopting these modern technologies.

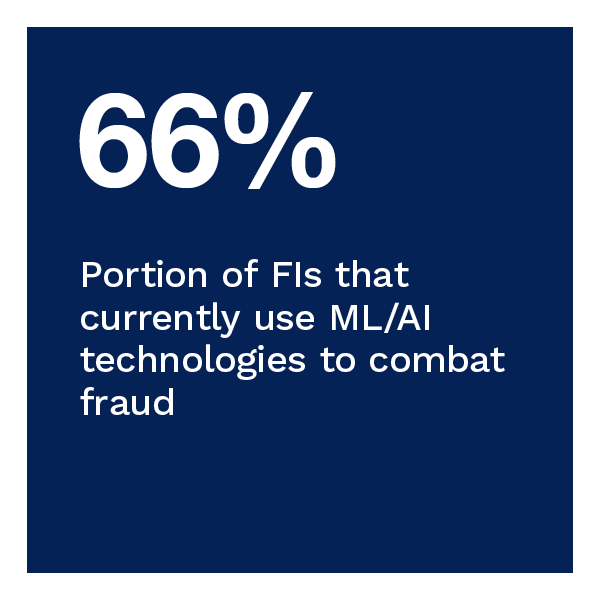

Rules-based algorithms, ML and AI are the technologies most used to combat fraud, especially among larger banks. In 2023, 60% of FIs report using rules-based algorithms to combat fraud, up from 50% in 2022. At least 66% of FIs with more than $5 billion in assets use ML and AI, exceeding the 44% of smaller FIs that do the same. Meanwhile, fraud scores and fraud prevention application programming interfaces (APIs) are falling out of favor, as fewer FIs now report using these technologies: 50% now, down from 65% in 2022.

To win the fight against rising fraud, financial institutions of all sizes need to adopt more sophisticated tools. Download the report to learn how financial institutions use ML and AI technologies in fraud prevention strategies