United States consumers who quickly adopted digital-first payment tools such as mobile wallets or touchless debit and credit cards during the pandemic are holding fast to their use today.

The value of global contactless payments alone has already experienced growth of nearly 50% in the past year, for example, increasing from $1.7 trillion in 2020 to $2.5 trillion in 2021.

This is prompting financial institutions (FIs) to reexamine their current offerings to meet the demands of today’s digital-first customers, contributing to rising interest in open banking technologies among financial players. The swifter payments and easier data sharing that open banking enables are quickly becoming necessary for banks — as well as merchants and even historically paper-based entities such as insurers — to stay competitive. Considering exactly how open banking could enable these organizations to match customers’ expectations and grow loyalty should therefore be a top priority for banks, businesses and insurers over the next several years.

In the latest U.S. Open Banking Tracker®, PYMNTS analyzes how consumers’ and businesses’ payment expectations alike have shifted in the past year, as well as how this has affected the interest in and adoption of open banking in the U.S. It also takes a closer look at how open banking is likely to progress in the market given such trends.

Around the Open Banking Space

Around the Open Banking Space

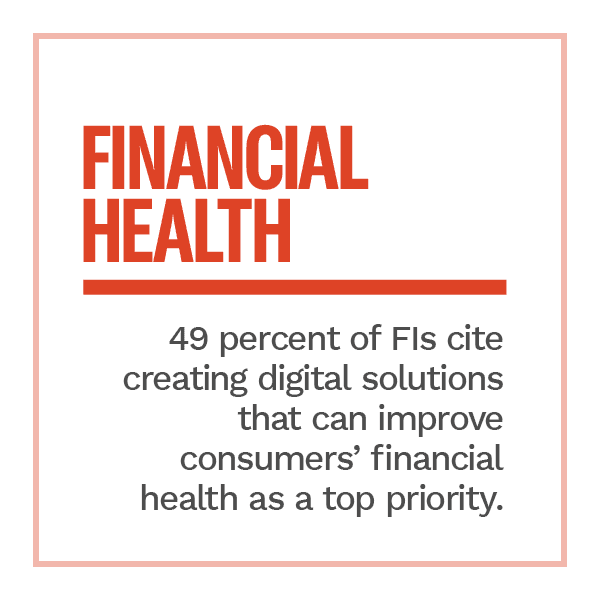

Consumers today are expecting more out of their relationships with their banks, meaning FIs must find ways to stand apart from their competitors to keep them engaged. One study found 41% of individuals want more personalized banking experiences, for example, including access to tailored financial advice such as how to better save money. This means banks must be able to have instant access to consumers’ financial data to be able to provide such advice. Meeting consumers’ growing demand for transparency and control over their finances will require the use of open banking, making such technologies of higher interest to banks.

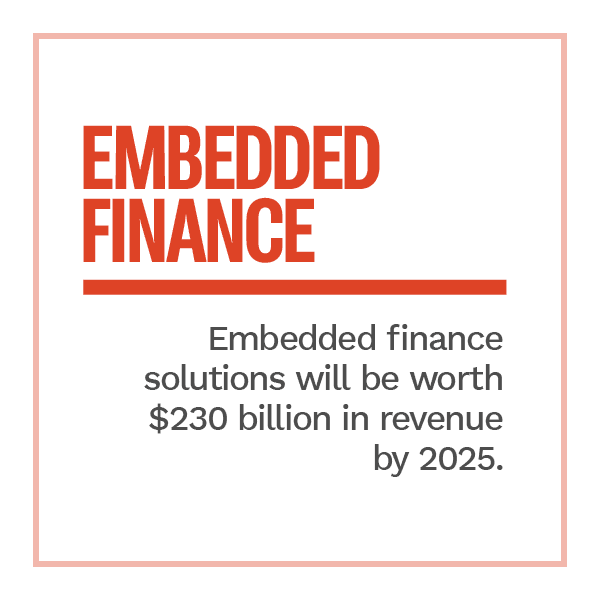

Integrating with open banking application programming interfaces (APIs) can also allow banks as well as businesses to implement new payment tools that enable speedier transactions, as well as personalize their customer experiences. This includes tools such as embedded finance solutions, which use APIs to nestle payments directly into mobile apps or websites for ease of use, for example. The value of embedded finance solutions is expected to grow rapidly over the next four years as their benefits become more apparent to financial entities, rising from a $22.5 billion valuation in 2020 to approximately $230 billion by 2025. Analyzing how they could incorporate such tools into their own offerings should be a key area of focus for banks and businesses moving forward.

Open banking could also provide FIs with a growing opport unity to gain the loyalty of small- to medium-sized businesses (SMBs) as well as consumers. One study found SMBs represent a $370 billion collective opportunity for U.S. banks, with many of these companies seeking out payment services that allow them to accept and receive payments more conveniently. Providing next-generation payment solutions as well as tools that can help SMBs manage their invoices and other payment processes more efficiently could allow FIs to generate lasting loyalty, making the adoption of open banking solutions critical.

unity to gain the loyalty of small- to medium-sized businesses (SMBs) as well as consumers. One study found SMBs represent a $370 billion collective opportunity for U.S. banks, with many of these companies seeking out payment services that allow them to accept and receive payments more conveniently. Providing next-generation payment solutions as well as tools that can help SMBs manage their invoices and other payment processes more efficiently could allow FIs to generate lasting loyalty, making the adoption of open banking solutions critical.

For more on these and other stories, visit the Tracker’s News & Trends.

How Insurers Can Tap Open Banking to Smooth Payment Frictions

Both consumers and businesses alike are beginning to anticipate easy and near-instant payment experiences wherever they go, putting increased pressure on companies still largely reliant on manual payment processes — such as insurance firms — to innovate.

Integrating open banking APIs could help entities such as insurers support the digital, seamless payment methods their clients increasingly want, but there are still a few obstacles that may hold insurers back from doing so, explained Adriana Hastings, treasury management director for Huntington Bank.

To find out more about how open banking technologies could help insurers and merchants ease payment pain points, visit the Tracker’s Feature Story.

Deep Dive: How Open Banking Could Aid Insurers’ Digitization Efforts and What Is Holding Them Back

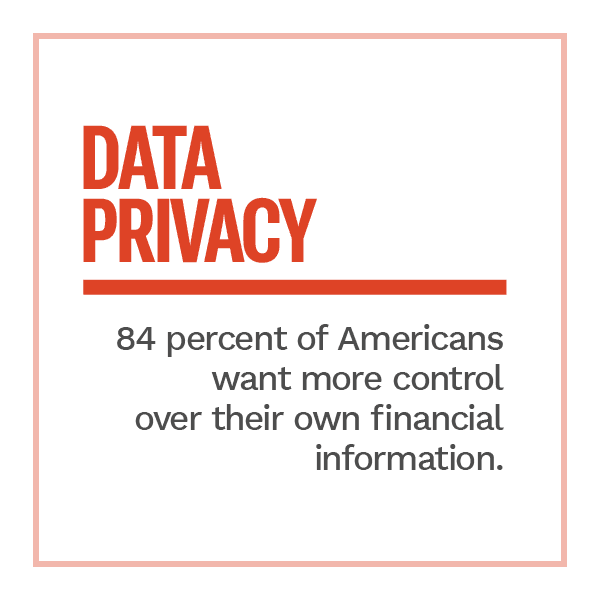

Open banking is steadily expanding within the U.S., but several questions still remain for how it wil l take shape, not only for banks and businesses but for other entities such as insurers. Debates are still ongoing regarding how data privacy and security should be treated, for example, as well as precisely how money can be moved via APIs as open banking technologies become more widely familiar. Answering these questions is swiftly proving critical for banks and insurers, however, as consumers come to expect speedy and seamless payment experiences no matter the use case.

l take shape, not only for banks and businesses but for other entities such as insurers. Debates are still ongoing regarding how data privacy and security should be treated, for example, as well as precisely how money can be moved via APIs as open banking technologies become more widely familiar. Answering these questions is swiftly proving critical for banks and insurers, however, as consumers come to expect speedy and seamless payment experiences no matter the use case.

To learn more about how open banking could benefit insurers as they look to digitize payments and other processes, visit the Tracker’s Deep Dive.

About the Tracker

The U.S. Open Banking Tracker®, a PYMNTS and Endava collaboration, examines how open banking developments are affecting U.S. retail payment trends and future developments.