In fact, the convenience and ease of use offered by these apps have made them the preferred method of banking for many customers, with the majority of millennials, Generation Z, and Generation X consumers using them as their primary financial tools.

But while digital banking has its advantages, several challenges persist, as detailed in “Why Digital-First Banking Does Not Mean Digital-Only,” the latest report in the Digital-First Banking Tracker® Series by PYMNTS Intelligence and NCR Voyix.

According to the study, applying for mortgages, loans, and conducting major financial transactions are often seen as best done in person, and therefore digital banks need to find a balance between enhancing digital experiences and facilitating human-centric customer interaction to meet the evolving needs and expectations of their customers.

Moreover, the demand for better service and personalized experiences was the driving force behind 25% of customers switching banks last year, according to research from Salesforce, per PYMNTS. Among those who switched, more than half did so seeking better digital experiences, while 39% left in search of enhanced customer service.

Furthermore, despite the widespread adoption of digital banking, customers still harbor reservations about the deployment of artificial intelligence (AI) within financial services. As the study noted, many believe that factors such as data transparency, human oversight, and government regulation are essential to enhance customers’ comfort levels with the use of advanced technologies in the financial services space.

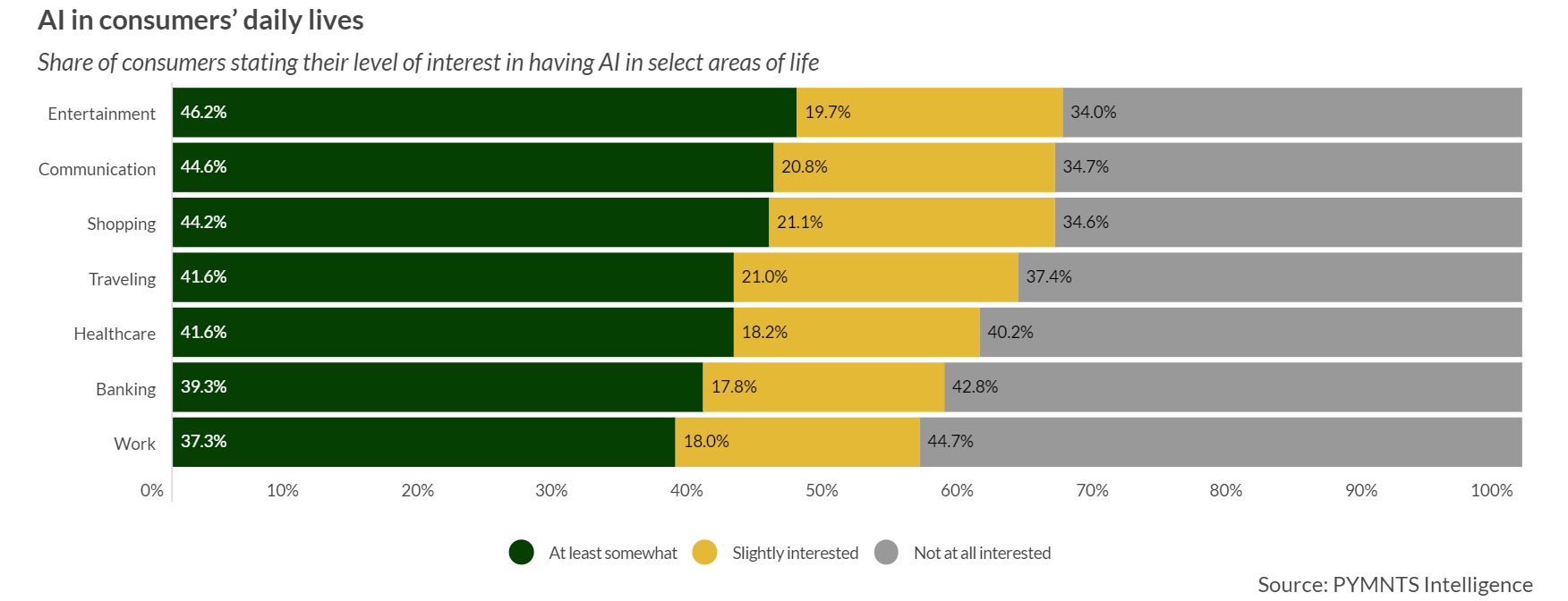

These concerns dovetail with separate PYMNTS Intelligence research that shows that consumers, particularly older generations, remain hesitant about AI’s involvement in certain aspects of their lives, including banking and work-related activities.

In fact, the “Consumer Interest in Artificial Intelligence” study found that only 39% of consumers expressed at least some interest in AI involvement in their banking activities, and this percentage dropped to 28% among baby boomers and seniors.

The report also shines a spotlight on digital friction, characterized by complicated online application forms and processes, which can also lead to customer frustration and prompt them to seek alternatives.

A study reveals that nearly half of customers encountered friction while attempting to open accounts online, with a significant percentage abandoning the sign-up process or choosing to take their business elsewhere. Simplifying and improving the account sign-up process with a human-led approach is crucial for customer retention.

In essence, navigating the evolving financial services landscape and proactively addressing future challenges will require banks to focus on advancing digital experiences, tailor services to individual preferences and strike the right balance between digital innovation and human interaction.

By consistently enhancing their offerings and staying attuned to the evolving needs of their clientele, banks can build lasting customer loyalty and resilience, ensuring not only customer retention but also positioning themselves to thrive in the dynamic digital era.