In a move designed to bring the value and convenience of payments to software platforms to the U.K., market, WePay is setting up shop across the pond.

Today (July 26) the firm announced its expansion into the United Kingdom, venturing beyond North America (the U.S. and Canada), with a focus on payments services that have been in place at firms across crowdfunding providers such as FundRazr and business solutions such as Infusionsoft. The firm said in its release detailing the expansion that it has also opened new offices in both London and Providence, Rhode Island, focused respectively on business development beyond the U.S. and customer service.

In an interview with PYMNTS, Bill Clerico, the co-founder and chief executive officer of the firm, said that the branching out into the U.K. represents a natural extension of some larger trends in the payments industry. Those, Clerico observed, includes the fact that “the platform movement knows no boundaries – it’s one where we’ve identified that technology is fundamentally reshaping our economy everywhere.”

Clerico emphasized that small businesses of all types – and in every geography – are using cloud software and online marketplaces to grow their businesses. That need, he says, is fueling the growth of software and platforms designed to help those SMBs maximize their chances of success, whether that SMB is a hairdresser, a dog sitter, or a consultant.

These platforms help these SMBs handle the minutiae of taxes, payroll, and any number of core business functions. “Platforms help small businesses do everything from acquire customers to keep their books,” Clerico explained.

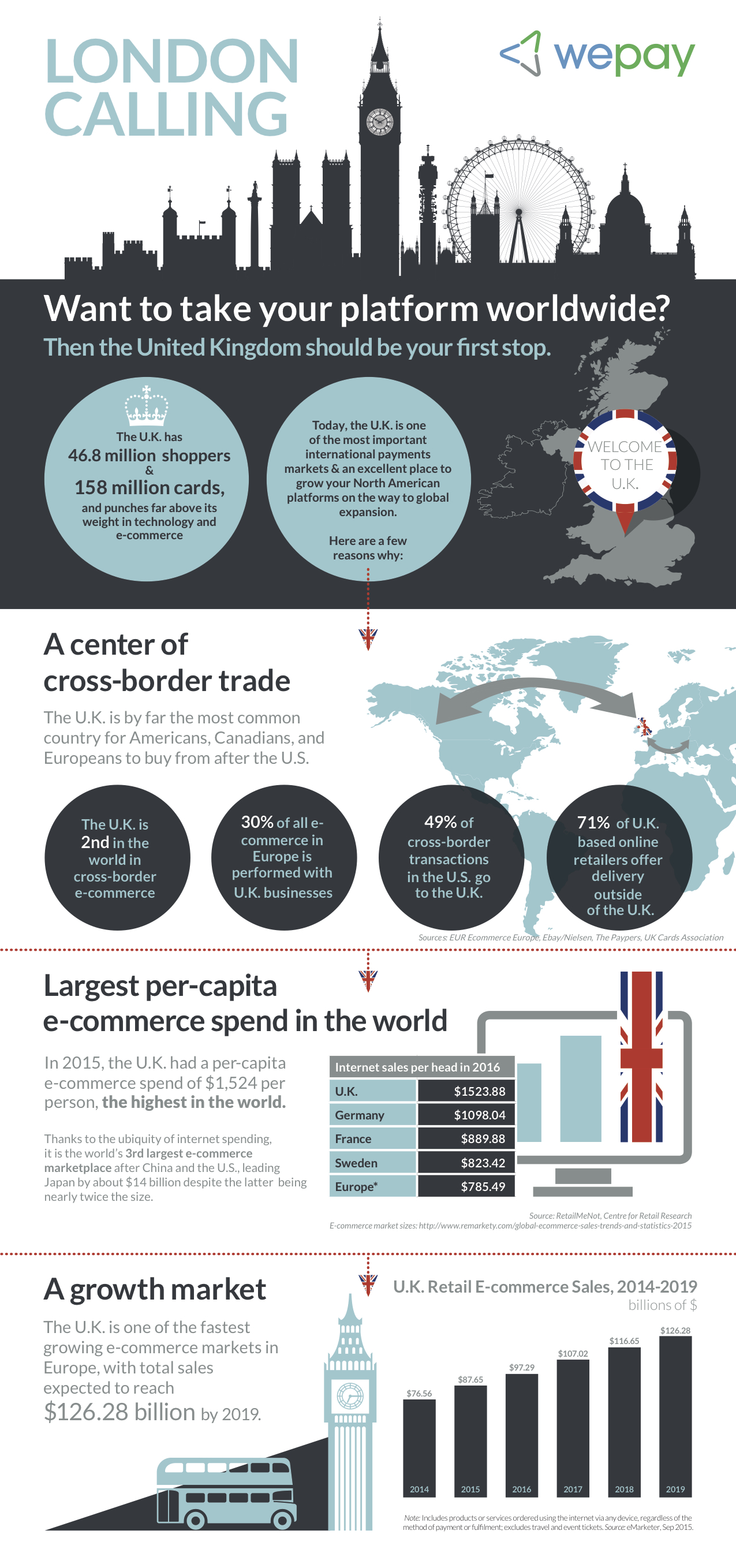

As the third largest digital economy in the world, Clerico said, the U.K. is particularly well-positioned to take advantage of that platform movement. The added attraction comes with its prominence in the FinTech scene, the U.K.’s relatively advanced use of credit cards and its standing as the fifth largest overall economy in the world. The commonality of language doesn’t hurt, either.

And WePay’s role? To help those platforms make the move across the pond without having to worry about the mechanics of actually getting there. The reality of platform economies is that the commerce that comes from them is very localized. A U.S.-based platform has to enable payments in every market in which they operate.

“A lot of platforms,” noted Clerico, “started in Silicon Valley,” which means that they may run into difficulty expanding outside of Silicon Valley when it comes to payments. WePay, he remarked, can enable those platforms to enter the U.K. and also work with small businesses there that might want to take advantage of that platform opportunity.

“Our work is on the back end,” noted Clerico, “and is not visible to our customers and that is where we wanted to be.” But to gain entry into the nation, he said WePay had to first work with several U.K. and E.U. regulators in order to be licensed and then get set up to process payments. Then WePay had to gain approval of existing operations from both Visa and Mastercard.

“Finally,” said Clerico, “we had to localize the application and support the right currencies … all this comes into the backend [so that we give our customers a] couple of simple new API fields.”

So for example, a service provider works with a client locally, and this is a way to get merchants onboard and comfortable with platform services, as the initial focus is on acceptance above anything else, to start.

As for the looming impact of Brexit, added Clerico, “the short answer is it has no effect. We are launching in the U.K., we are licensed in the U.K. … and so there is no impact.”