Account-to-account (A2A) payments, also known as pay-by-bank, are gaining popularity among consumers.

In the United States, 36% of consumers use this payment method, according to insights detailed in the PYMNTS Intelligence study “Tracking the Digital Payments Takeover: Consumer Familiarity Controls Account-to-Account Payment Growth.”

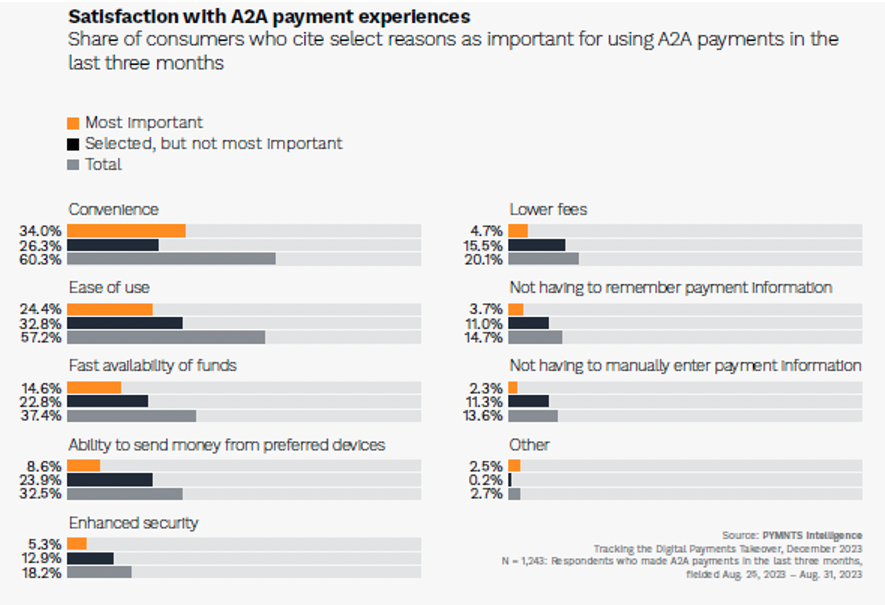

Convenience also plays a role in consumer satisfaction with A2A payments, particularly in peer-to-peer (P2P) use cases, according to the study. Platforms like PayPal, Venmo and Cash App provide user-friendly experiences, leading to high satisfaction rates among more than 60% of A2A payment users.

Another benefit of A2A payments is their simplicity and ease of use. By bypassing traditional card networks and intermediaries, users can avoid sharing sensitive financial information, reducing the risk of fraud.

The speed at which funds become available and the ability to send money from preferred devices are also factors for consumers. Over one-third of respondents prioritize getting their money quickly, while another 33% consider using their preferred devices for sending money vital in their decision to use A2A as a payment method.

A2A payments are typically processed in real time, which allows merchants to not only receive funds immediately, but also improve cash flow and minimize the risk of bad debt. This immediacy also enhances customer engagement, as merchants can offer discounts or rewards for A2A payments, making it easier for customers to check out online.

Other factors consumers prioritize for using A2A payments include lower fees (20%), heightened security (18%) and the convenience of not needing to recall payment details (approximately 15%), the study found.

Generational preferences also play a role in A2A adoption. Millennials, who are more inclined toward digital platforms, are at the forefront of adopting A2A payments, especially for P2P transactions and online shopping.

On the other hand, baby boomers and seniors show the least interest and often claim a lack of understanding about A2A payments. To drive broader use, targeted adoption initiatives tailored to different generational groups could be implemented.

Incentives also prove to be influential in shaping consumer behavior. The study revealed that 41% of consumers who did not use A2A payments in the 90 days before participating were willing to switch if payment platforms introduced incentives such as discounts or rewards. This suggests that targeted campaigns with monetary incentives could drive adoption across different age groups.

While there are barriers to wider A2A adoption, such as a lack of consumer familiarity and generational differences in awareness, targeted campaigns and incentives have the potential to drive market penetration and increase A2A transaction volumes, ushering in a more seamless and efficient financial landscape.