Fraud is top of mind in tech — especially in payments — and not just because of the collapse of crypto trading firm FTX.

FinTechs promise to disrupt traditional financial services and through digital conduits at scale, also seek to speed up money movement, in real time, across a range of seamless, streamlined customer experiences.

But along with the promise lies some peril. These digital upstarts are increasingly in fraudsters’ crosshairs, and the bad actors are getting away with huge sums of money.

In the report “The FinTech Fraud Ripple Effect,” done in collaboration between PYMNTS and Ingo Money, we found that the average U.S. FinTech loses $51 million to fraud every year, or about 1.7% of its total revenue.

That’s an average. The impact is even more keenly felt by smaller FinTechs, as small firms lose 57% more revenue to fraud than large firms, with the average small firm losing 2.2% of its annual revenue to losses incurred by fraud.

Twice the Friction

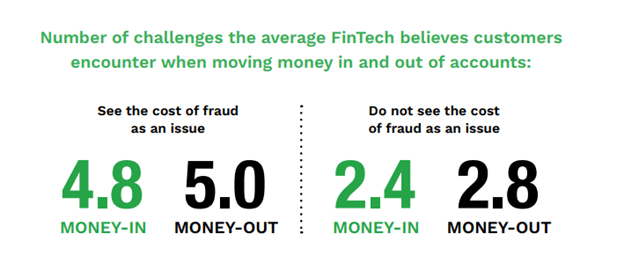

Fraud can and does have knock-on effects well beyond a diminished top line — diminishing the end user’s experience, too. PYMNTS/Ingo found the lack of fraud and risk controls is creates roughly twice the amount of friction for consumers. That’s because the transactions get dragged out, delayed, or perhaps even declined amid the need to do fraud checks or analyze the legitimacy of users. The FinTechs struggling with fraud (where the cost of that fraud is an issue) displayed 4.8 types of friction when depositing money into their accounts, far outpacing the 2.4 seen by those who do not grapple with fraud costs.

Friction is the Customer’s Enemy

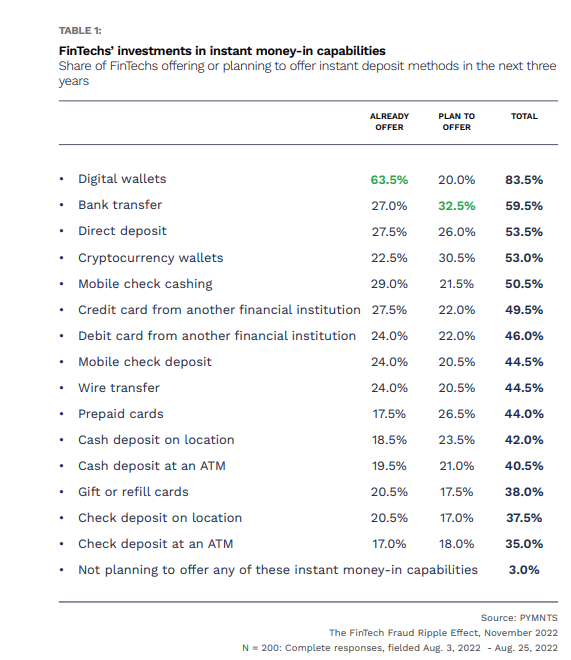

FinTechs are nothing if not ambitious and are cognizant of what their consumers want, especially when funding accounts. By way of just two examples, instant cryptocurrency wallet deposits and in-store cardless cash withdrawal options are near the very top of FinTechs’ innovation wish lists, with 31% planning to invest in the former and 28% planning to invest in the latter in the next three years.

The chart below details the broad range of instant deposit methods on FinTechs’ roadmaps – and, thus, the broad range of “money in” options on offer.

The frictions are especially apparent in “money-in” activity, tied to funds flowing into accounts, such as deposits.

The frictions are especially apparent in “money-in” activity, tied to funds flowing into accounts, such as deposits.

Almost one in five — 19% — of FinTechs grappling with fraud said that a friction point lies with guaranteeing good funds and moving them into accounts in a speedy manner; Security issues give rise to friction for 16% of those firms, and there are high fees and transaction limits too.

Advanced technologies may solve some of those frictions — and improve the customer experience. As noted in this space earlier in the year, Ingo Money CEO Drew Edwards has noted that frictions and fraud have limited issuers’ ability to offer accounts to the entirety of their traditional consumer bases.

In just one example, check services might be made available to direct deposit customers who have been through at least two pay cycles with the FI. That demographic tends to be less than 30% to 40% of the account base, Edwards has told PYMNTS.

Against that backdrop, the company earlier this year announced the availability of its Inbound Digital Transfer and Risk Services. The service uses device-related attributes spanning the location in which a transaction is happening, the consumer’s behavior when they’re interacting with the site or the app, and account-related details to stop fraud risk at the initial moments of engagement with the FinTech — streamlining and securing the “money-in” experience.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More