The expectations of small to midsized businesses (SMBs) regarding payment service providers have never been higher, with owners and employees demanding the same payment speed and convenience they experience everywhere else in their digital lives. In the United States, the only widespread real-time option was The Clearing House’s RTP® network, but that will begin to change with the introduction of FedNow.

The service, which launched July 20, could revolutionize the real-time payments scene in the U.S., with retailers particularly hoping for real-time payments to help their business. This month’s PYMNTS Intelligence examines FedNow’s capabilities and explores its key differences and similarities with the RTP network.

FedNow marks the biggest shakeup in U.S. real-time payments in six years.

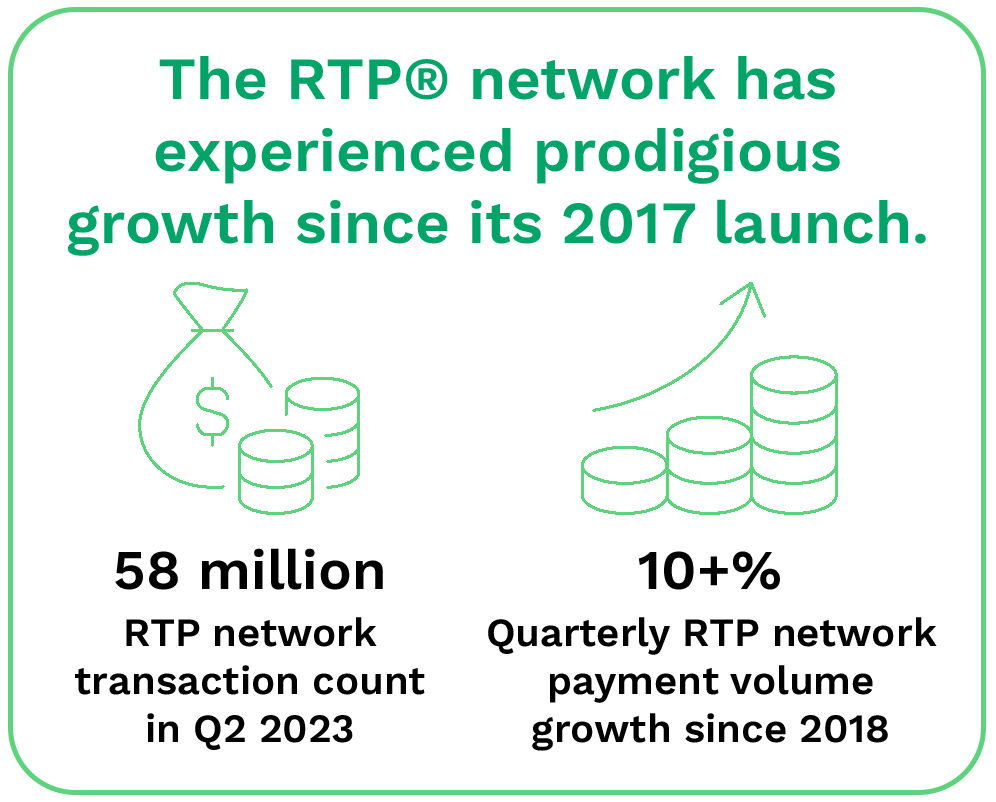

The Federal Reserve plans to introduce FedNow in stages. The July release is expected to provide baseline functionality for services like account-to-account transfers and bill pay, while further functions will be introduced in later updates. The RTP network is already fully functional, as it has been the standard for real-time transactions in the U.S. since its 2017 launch.

Both systems work on a push basis, with transactions being sent by the payer rather than pulled by the payee. This provides a greater level of security from scammers than pull payments, but transferred funds are irrecoverable. Both networks will operate 24/7 year-round, and both allow funds to be transferred instantly from one account to another.

Both networks operate on the ISO 20022 data standard, but the exact nature of the transfer varies slightly. The Clearing House acts as a hub for clearing the payment between accounts on the RTP network and sends settlement instructions to the Federal Reserve, where the actual money transfer takes place. FedNow, meanwhile, has the Fed handle the clearing and settlement directly. From the point of view of the end user, this difference is largely unnoticeable, however.

FedNow and the RTP network differ in several key manners, including limits and costs.

One of the largest differences between the two systems is their transaction limit: FedNow users will have a default limit of $100,000 that they can adjust upward to a maximum of $500,000, if desired. The RTP network, meanwhile, allows transactions of up to $1 million, with a similar option to set lower sending limits if desired.

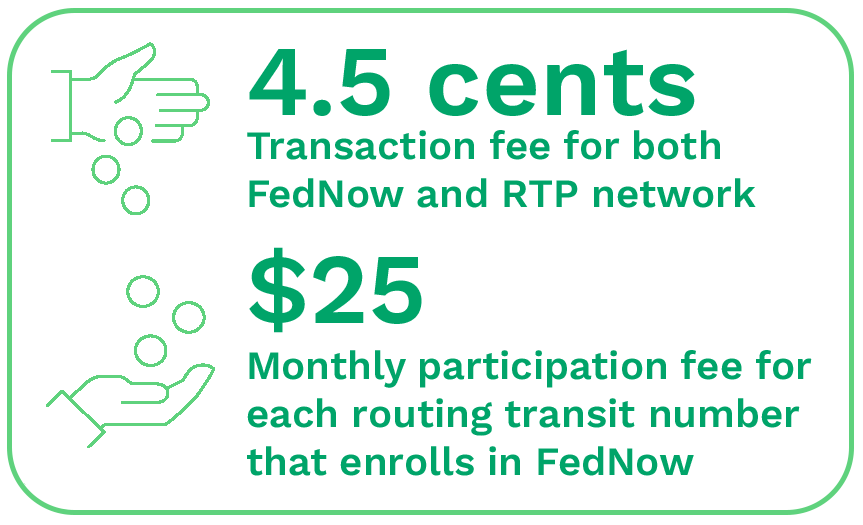

The two systems also have different fees: While both systems charge 4.5 cents per transaction, FedNow charges each enrolled routing transit number $25 monthly for participation — a fee that the RTP network lacks. It will be up to customers to choose which features matter most when picking a system to use, or to determine whether it is worth using both systems for different purposes.