Instant payments are quickly growing in popularity in the United States and abroad, but their adoption has often been hampered by a need to interface with customers’ preferred financial institutions (FIs). Customers are then faced with a difficult choice: abandon their current bank in favor of one with instant payments capability, or remain with their preferred FI and suffer through slow and obtrusive legacy payment systems.

Open banking can offer the best of both worlds, allowing instant payment providers to connect with any bank’s application programming interface (API) and meet customers where they are. This month, PYMNTS examines how open banking can accelerate real-time payments implementation, as well as how open banking regulations in the U.S. and Europe are affecting real-time payments in these regions.

Open Banking Unlocks Innovative Payment Services

Open banking makes all bank APIs free and accessible to third-party FinTechs and payment providers, allowing the latter to customize their services easily to fit with any bank on the market. These third parties include instant payment providers that use systems such as the RTP® network or Single Euro Payments Area (SEPA) Instant, for example. Open banking thus places the decision to leverage real-time payments into customers’ hands rather than requiring the bank to decide unilaterally whether or not to enable real-time payments.

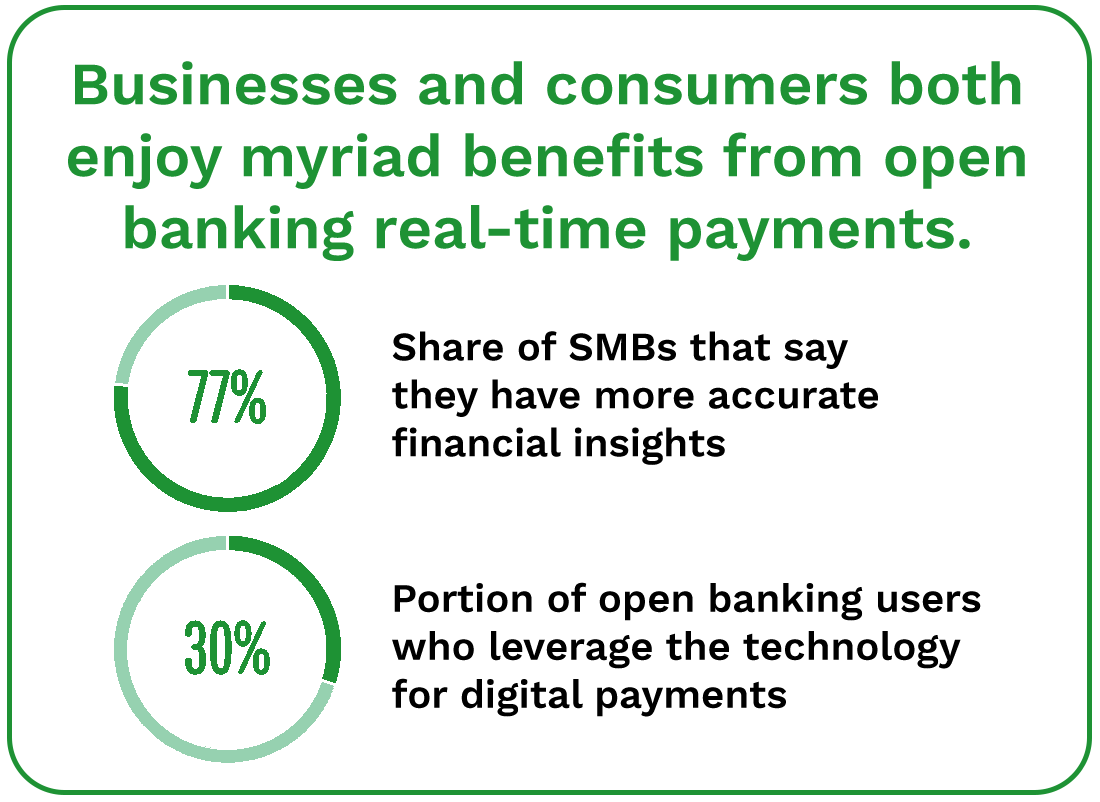

The benefits of offering real-time payments via open banking protocols are obvious to the end user. A survey found that 77% of small -to medium-sized businesses (SMBs) had more immediate and accurate insights into their current financial status as a result of using these services. This is because having payments made in real time means that account information does not have to wait for wire transfers to be completed or for checks to clear.

The same study found that 30% of open banking users leverage this technology for payments, and 6% use it for both payments and data analysis. The six months leading to March 2022 saw 21.1 million open banking payments, up from 6.1 million the year before, driven in large part by the added convenience of real-time transactions. While the benefits of open banking-enabled real-time payments seem self-evident, the regulatory environment enabling these implementations varies greatly on either side of the Atlantic.

EU, UK and US Open Banking Regulations Could Lead to Different Outcomes

The United Kingdom is no longer part of the European Union, but its Open Banking Standard largely mirrors the EU’s Second Payments Services Directive (PSD2) regulation. The nine largest retail banking providers have been ordered by the British government to implement open banking protocols — with six of them completing this directive so far — along with dozens of banks in the rest of Europe. These open banking regulations are expected to interface with the EU’s SEPA Instant Credit Transfer to make instant payments a reality for millions, regardless of their preferred FI.

Open banking regulation is currently in limbo in the United States, with a proposed open banking rule from the Consumer Financial Protection Bureau (CFPB) currently held up due to privacy concerns. While the White House has publicly urged the agency to accelerate its open banking protocols, privacy advocates argue that Big Tech would have too much access to customers’ personal bank data. It currently remains to be seen if and when the open banking protocol will come into effect and how it will impact real-time payments in the U.S.