As inflation grows faster than most wages, an increasing number of households are living paycheck to paycheck, having just enough money to make it to the next payday with little to no funds in savings or investment accounts. Even households with high wages can find themselves in this predicament. PYMNTS’ research found that 70% of urban dwellers, who were likelier than the general population to have high wages, lived paycheck to paycheck.

While higher wages are the best long-term solution, providing access to real-time payments could significantly help paycheck-to-paycheck households. This month’s PYMNTS Intelligence examines how real-time payments can help individuals manage their cash flow more efficiently and how employers can deploy instant payroll to reduce financial strain on their workers.

Instant payments give consumers a more accurate snapshot of their financial situations, allowing them to budget better.

Rather than having pending payments or checks waiting for the recipient to cash, money sent via real-time rails is moved between accounts instantly, so consumers know exactly how much money they have to work with at any given moment. This allows them to make better financial decisions and avoid accidentally overdrawing on their accounts, which can incur stiff fines from their banks and drive them further into financial trouble.

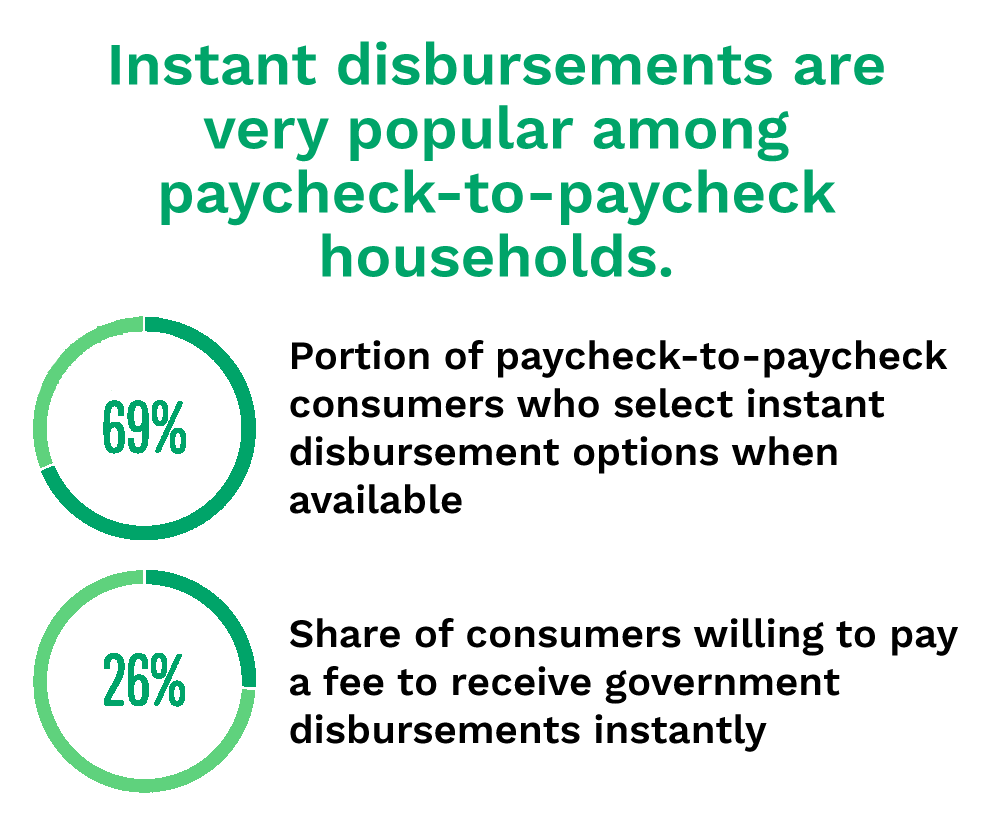

When given the choice, 69% of paycheck-to-paycheck consumers select instant disbursement options. Consumers are more split as to whether the privilege of knowing exactly where their money is and when it will arrive is worth an extra charge. Twenty-six percent of consumers said they would willingly pay a fee to receive government disbursements instantly, for example, but 26% of bridge millennials who prefer instant disbursements would opt out if they had to pay for these payments.

Offering real-time payments to consumers also indirectly benefits the businesses they patronize. Nearly two-thirds of consumers said they would be at least somewhat more willing to continue transacting with a business that is paying them a disbursement if instant payments were free.

Instant payroll makes a major difference for paycheck-to-paycheck workers.

Real-time payments that companies implement to pay their workers can have an even more dramatic effect on paycheck-to-paycheck households by removing pay periods entirely. Earned wage access (EWA) allows workers to withdraw their wages instantly as they are earned rather than waiting for a traditional payday, offering workers much more flexibility to react to sudden expenses rather than undertaking risky options such as payday loans.

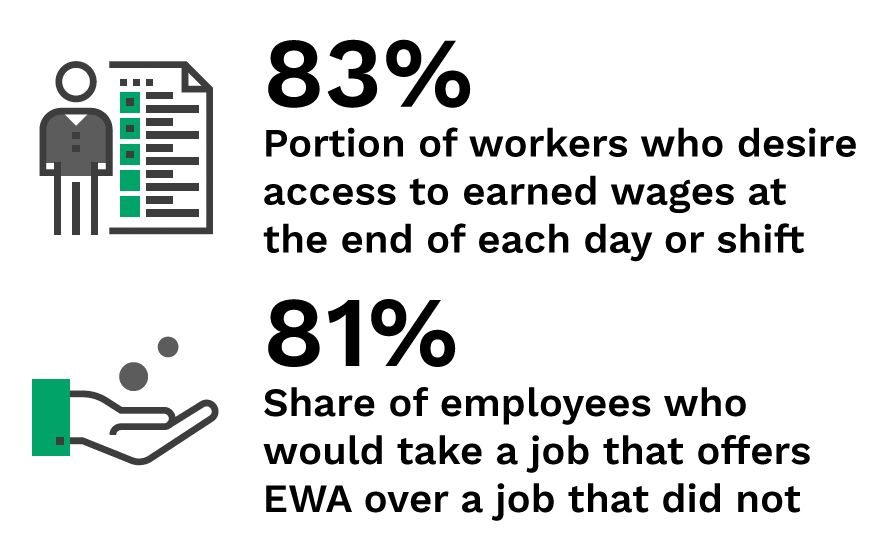

Eighty-three percent of workers said they believe they are entitled to earned wages at the end of each day or shift, while 78% said earned wage access would increase their loyalty to their employers. Most strikingly, 81% of workers would take a job with EWA over a job that did not offer this benefit, meaning that helping paycheck-to-paycheck workers can benefit corporates as well.