Main Street small and medium-sized businesses (SMBs), which faced challenges during the pandemic and managed to stay afloat, are aiming to stabilize their finances in the current inflationary market conditions. According to PYMNTS Intelligence, these businesses require assistance in meeting their financing requirements to steer clear of closures and prepare for expansion.

“Main Street Health Survey Q2 2023: Credit’s Key Role in SMBs’ Plans,” a PYMNTS Intelligence and Enigma collaboration, draws insights from a survey of 514 SMBs with brick-and-mortar shops in commercial districts across the United States to assess which resources business owners are planning on using to meet their businesses’ financial needs.

According to the report’s findings, nearly half (48%) of these enterprises intend to increase their reliance on financing in the coming year, while those that have access to business credit sources are planning to further increase their credit usage.

Additionally, Main Street SMBs with limited access to cash are less likely to anticipate revenue growth. However, those with access to business credit sources are planning to increase their credit usage, with an expected average increase of 72%.

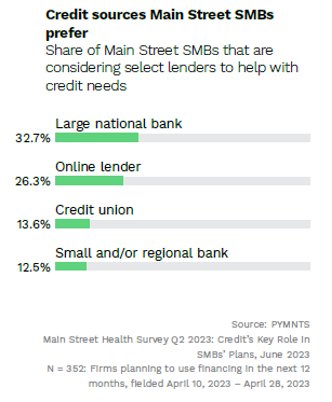

When it comes to the type of lenders being considered, approximately one-third of Main Street SMBs are considering large national banks like Bank of America, Wells Fargo and JPMorgan as their preferred source of credit, surpassing other lenders such as online lenders, credit unions, and smaller regional banks. Specifically, 26% are considering using online lenders, followed by credit unions (CUs) and smaller regional banks which stand at 14% and 13%, respectively.

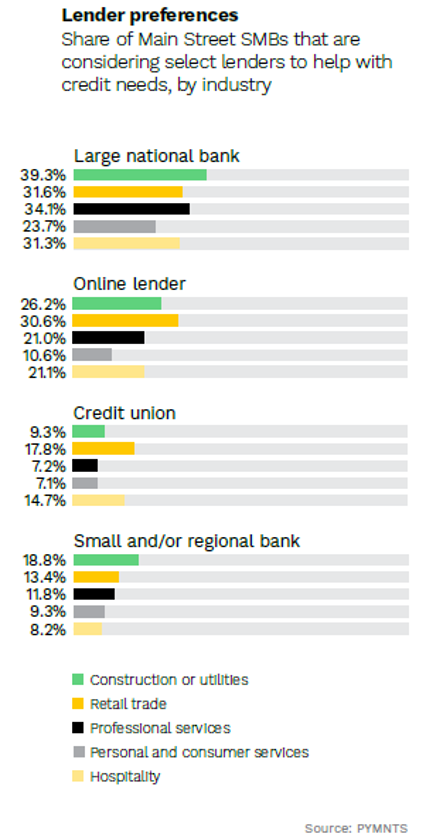

Examining the data by sector shows a similar trend. Among the five sectors studied — construction/utilities, retail trade, professional services, personal and consumer services and hospitality — Main Street SMBs consistently favor large national banks as their top choice when assessing lenders to support their credit needs.

“These preferences indicate the level of familiarity and trust that SMBs place in different types of financial institutions — and regardless of the type of industry, large banks hold the advantage,” the study noted.

While additional funds can provide advantages, Main Street SMBs contemplating utilizing more credit must be cautious of potential disadvantages such as high interest rates and opaque loan processing fees.

The survey found that most Main Street SMBs are not aware of or familiar with alternative financing options beyond traditional lenders. This lack of awareness may be attributed to their focus on day-to-day operations or their inability to qualify for other financing options.

The report also reveals variations in financing preferences across different SMB segments. Construction firms are more likely to consider using multiple sources of financing compared to businesses in consumer services. Retail trade SMBs are most likely to consider applying for credit with online lenders and credit unions.

Ultimately, access to credit and financing plays a crucial role in the viability and growth of Main Street SMBs. In fact, businesses with greater access to cash and financing sources are less vulnerable to business closures and more likely to expect revenue growth. This scenario underscores a key opportunity for lenders to earn the trust and confidence of Main Street SMBs, given that almost half of these businesses intend to increase their reliance on credit in the foreseeable future.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More