From time to time, most small and medium-sized businesses (SMBs) find themselves having to borrow money to meet short-term needs or unexpected expenses. But as PYMNTS Intelligence recently reported, many SMBs — especially those earning modest revenues — avoid borrowing whenever possible.

One of the key takeaways in PYMNTS Intelligence’s “SMB Borrowing Dynamics: Trends, Tools and Decision Drivers,” a report completed in collaboration with U.S. Bank, is that the smaller the business, the less interested it seems to be in using credit.

The report, which draws on insights from 2,668 SMB executives, revealed 90% of SMBs had to turn to at least one borrowing tool in the previous year. For most (73%), revolving credit products — such as credit cards and lines of credit — fit the bill. Nearly 34% tapped into buy now, pay later purchase options and 30% used merchant loans.

But the report also showed that approximately 10% of all SMBs avoided borrowing altogether last year, including 3% of those earning $10 million or more annually. So too did approximately 5% of middle-revenue firms (those earning at least $1 million but less than $10 million). Meanwhile, nearly 20% of businesses earning less than $1 million a year bowed out of borrowing altogether last year.

What was the reason for this reluctance to use any borrowing options?

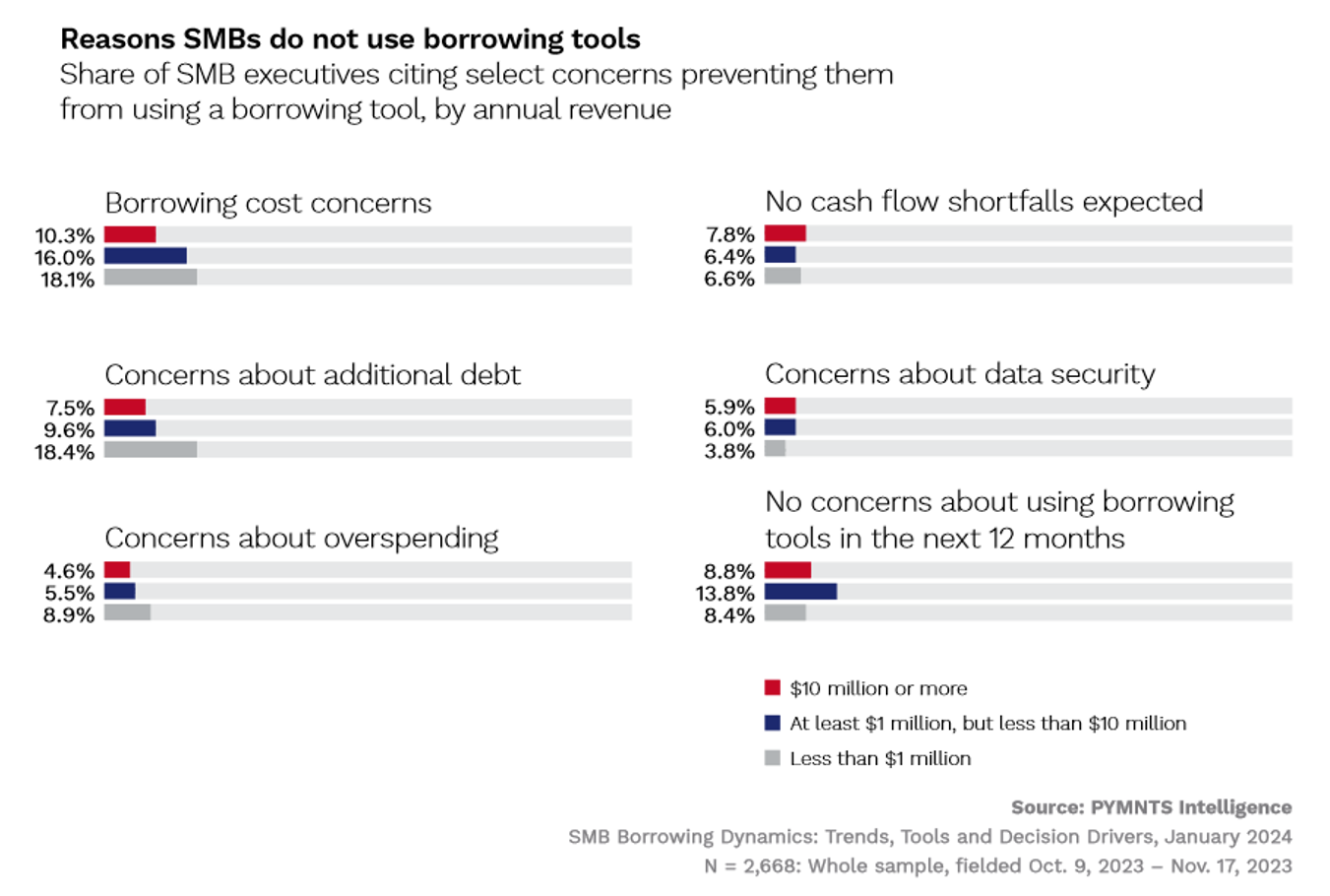

Overall, “SMB Borrowing Dynamics: Trends, Tools and Decision Drivers” found borrowing costs are a concern for 34% of all SMB executives we surveyed. But, as the accompanying figure above illustrates, borrowing costs were a significant disincentive for 16% of middle-revenue companies and 18% of low-revenue SMBs. And the cost of borrowing was only one concern. Ten percent of middle-revenue SMBs also said they preferred not to take on any additional debt last year, which was also a motivator for 18% of low-revenue companies.

Some good news: a handful of SMBs that were able to operate on budget last year with no need for emergency cash injections. Nearly 8% of high-revenue SMBs said there were no cash flow shortages — meaning there was no need to borrow. The same held true for 6.4% of middle-revenue companies and 6-6% of low-revenue SMBs. The rest, though needed some form of cash support, and — for financial institutions hoping to work with SMBs — low-cost, revolving borrowing tools appear to be the best bet.