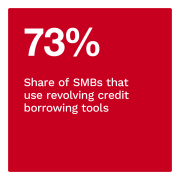

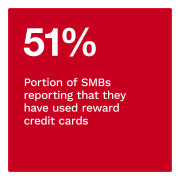

Approximately three-fourths of SMBs are using revolving credit, with rewards credit cards increasingly favored for their versatility and benefits. This underscores the unpredictable nature of SMBs’ financial needs and their strategic responses to market conditions.

Approximately three-fourths of SMBs are using revolving credit, with rewards credit cards increasingly favored for their versatility and benefits. This underscores the unpredictable nature of SMBs’ financial needs and their strategic responses to market conditions.

These are just some of the insights explored in “SMB Borrowing Dynamics: Trends, Tools and Decision Drivers,” a PYMNTS Intelligence and U.S. Bank collaboration. This report examines the complex patterns of SMB borrowing preferences and draws on insights from a survey of 2,668 SMB executives conducted from Oct. 9, 2023, to Nov. 17, 2023.

Other key findings from the report include:

Owner’s generation and annual revenues tend to influence SMB borrowing behavior.

SMB borrowing practices are correlated with a blend of generational influence and how much revenue the business generates. Higher-revenue SMBs tend to use 3.5 borrowing tools, on average, while their lower-revenue counterparts use 2.3, on average.

Data also reveals that SMBs with owners who are part of Generation X or millennials tend to use more borrowing tools than those owned by baby boomers or seniors, or members of Generation Z.

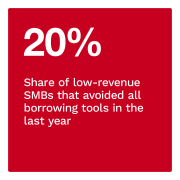

Revenue-size is a predictor of borrowing outlook.

SMBs’ approach to borrowing is significantly influenced by their revenue size, with 20% of low-revenue SMBs avoiding borrowing in the last year. Just 5.1% of medium-revenue and 2.9% of high-revenue SMBs have avoided using borrowing. This pattern underscores the varied levels of comfort with debt across different revenue tiers and suggests lower-revenue SMBs may face additional barriers to borrowing.

SMBs prioritize accessible borrowing tools that are sensible for their financial needs.

Seventy-five percent of SMBs prioritize the accessibility and availability of funds when choosing borrowing tools, emphasizing their fundamental need for flexible financing solutions. Financial considerations are also important for 71% of SMBs as they assess favorable payment terms, lower borrowing costs and even the potential to boost credit scores.

Banks that fail to offer a diverse range of borrowing tools will lose SMB customers to competitors that meet these businesses’ needs. Download the report to learn more about the factors driving SMBs’ use of borrowing tools.

Flexible and accessible borrowing tools are a financial cornerstone for many small to mid-sized businesses (SMBs). PYMNTS Intelligence’s latest study finds that 90% of SMBs have used at least one type of borrowing tool in the past year.

Flexible and accessible borrowing tools are a financial cornerstone for many small to mid-sized businesses (SMBs). PYMNTS Intelligence’s latest study finds that 90% of SMBs have used at least one type of borrowing tool in the past year.