The buy now, pay later (BNPL) space is relatively young.

And a greenfield opportunity would, seemingly, invite a broad range of players, large and small, spanning digital-only firms to traditional banks.

But there’s growing evidence that the market’s competitive landscape is narrowing: Experience matters, as does scale, when bringing new BNPL options to the masses.

Case in point, and a single, recent announcement among many: On Wednesday, PayPal announced its debut of PayPal Pay Monthly, a buy now, pay later (BNPL) offering issued by WebBank. The offering expands on PayPal’s existing installment products and let customers make purchases between $199 and $10,000, dividing the cost into payments over a six-month to two-year period, with the first payment due one month after purchase.

Read also: PayPal Launches Pay Monthly BNPL Offering

The announcement builds on momentum, where PayPal said in its most recent earnings report that it had seen $3.8 billion in BNPL volume in the latest quarter, with 18 million customer accounts opting to embrace BNPL.

And of course, Apple now has joined the fray — an instant juggernaut, where Karen Webster noted that the company is entrant number 80 in the BNPL race. Apple’s decision to supply the loans directly off its balance sheet shows that having a cash hoard could firm immediate heft in BNPL. That’s a big if, of course, which depends on Apple getting some tailwind under Apple Pay.

But the principle remains intact — namely that it takes money to make money, and that banks and Affirm and a host of others may be able to weather the macro headwinds and complexities of underwriting more easily than less-well-capitalized competitors.

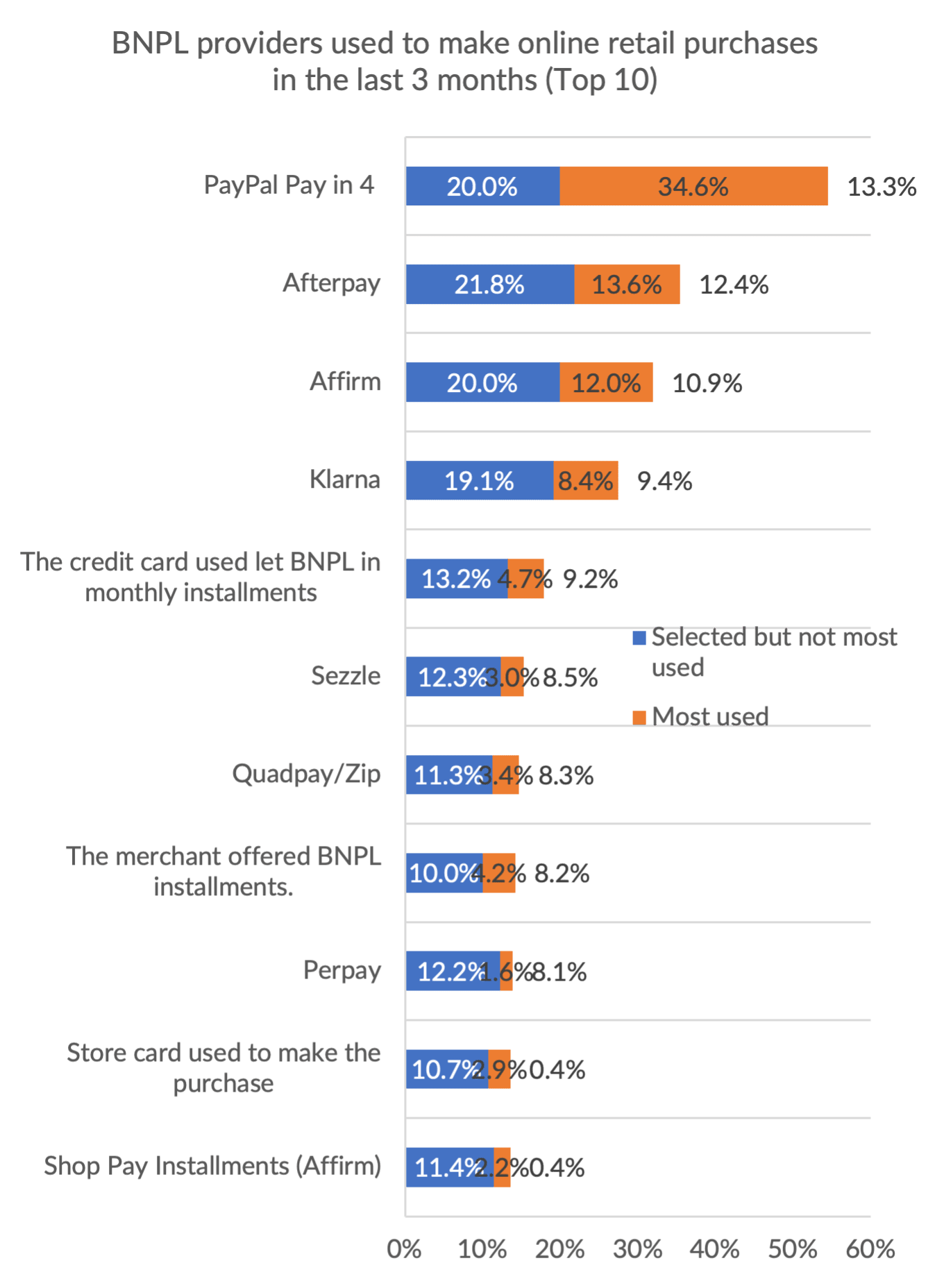

The tilt toward larger providers is underscored by PYMNTS data detailing in-store shopping, across 440 respondents. PayPal, Affirm and others hold sway here.

Source: PYMNTS.com, May 2022, N=624

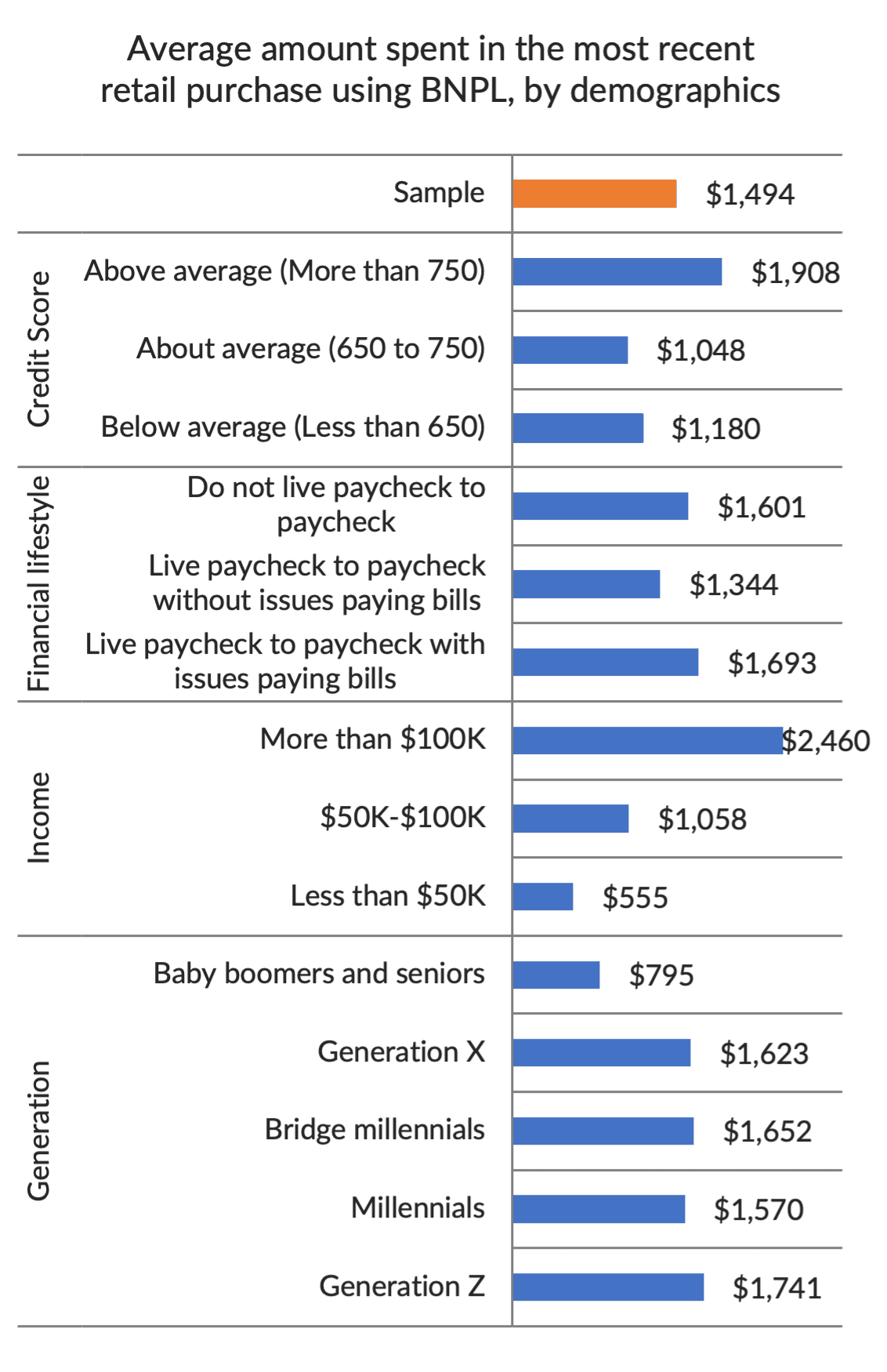

The most recent data collected by PYMNTS, in collaboration with LendingClub, show that the average ticket size stands at about $1,500 — which is well above the minimum “floor” that many BNPL plans offer. The tally increases to more than $2,400 for those who make more than $100,000 annually.

Source: PYMNTS.com, n=1,353, May 2022

The younger generations are the ones turning to BNPL options with fervor, as shown by the size of the loans they are taking on. Generation Z spends about $1,740 via BNPL, which far outstrips the $795 spent by baby boomers and seniors.

If 79% of current BNPL consumers plan to continue using a BNPL option for retail purchases in the next 90 days — as we have found — and 40% of them say they will plan their shopping around their ability to use BNPL to pay, the dry powder is there. The advantage, right now, might lie with companies like PayPal, which has decades of underwriting experience, and which already connect directly with bank accounts. The banks themselves, we should note, have been busy fine-tuning their own BNPL offerings. PYMNTS data show that 70% of consumers would like their banks to offer BNPL, indicating that trust, and a large installed base, can be significant tailwinds to new revenue streams.

As it stands right now, however, the market is bifurcating between a few marquee names (PayPal, Affirm, etc.) … and everyone else.