Is Apple Pay Later Really a Threat to Affirm and Other BNPL Providers?

Apple’s Project Breakout finally broke out a week ago today at Apple’s WWDC. It was then that Apple confirmed what was probably one of the worst kept secrets in payments: it would enter the buy now, pay later (BNPL) space with its own product, Apple Pay Later.

See also: The One Big Thing Apple’s Project Breakout Needs but Doesn’t Have

It didn’t take long for the media to spin into a Pay Later frenzy, with headlines suggesting that the FinTechs in the space — namely Affirm, Afterpay and Klarna — are more or less toast, that Pay Later is (Afterpay owner) Block’s and Affirm’s biggest nightmare.

Somehow even Amazon got clumped into the category of biggest losers as a result of Pay Later. So did PayPal, which of course has had its own BNPL product since the acquisition of BillMeLater in October 2008. Its stock dropped nearly 10% last week.

I’m not sure that any of them have much to worry about from this latest entry into the BNPL space.

In fact, the so-called ‘nightmare’ may end up being Apple’s.

The Pay Later Particulars

Apple, with Pay Later, has the distinction of being about the 80th such player, globally, to vie for a piece of the very hot Buy Now, Pay Later space, not counting what the card networks and FinTechs are doing to activate issuer BNPL options at the online and physical POS.

I’m not exaggerating about being the 80th new entrant — this time last year we were at 67 and counting. Even with consolidation, the number of BNPL schemes globally has skyrocketed over the last two years, including a number of EU BNPL FinTechs that have moved recently into the U.S. market. Add to that the many use-case-specific schemes — for healthcare, travel, home repair, even veterinary services — and installment payments has become the hottest thing in payments since cash-back rewards.

Pay Later will be broadly available to iPhone users in September as an automatic part of the iOS 16 upgrade, accessible to those who satisfy its underwriting requirements and want to use it and Apple Pay to make purchases online or in-app.

Like many FinTech BNPL offerings, Pay Later loans will have a $1000 cap to start, payable in four zero-interest installment payments over six weeks. Goldman Sachs is enabling the issuance of the virtual cards used to pay the merchants which will ride Mastercard’s debit rails. Loan repayment is in the form of automatic withdrawals from a Pay Later accountholder’s checking account via their registered debit card credentials.

Apple plans to lend from its own balance sheet through a separate company, Apple Financial Services. It has a pretty healthy balance sheet from which to lend, which makes the economics of its BNPL proposition attractive, at least in theory. Reportedly at $73 billion last quarter, one could say that its Pay Later “credit facility” is more than 1.5 times the market cap of Block (which owns Afterpay) and 15 times that of Affirm.

Underwriting those Pay Later loans will leverage all of the Apple ID datapoints Apple has amassed from most iPhone users and has access to — analytics related to the behaviors of the billion or so Apple ID users, including their registered payments credentials.

Hold that thought.

The acquisition of U.K.’s Credit Kudos in March of 2022 will also give Apple’s risk teams access to bank data on customer payments flows to further assess creditworthiness in real time. Pay Later loan amounts will be based on Apple’s assessment of the borrower’s credit risk.

See more: Apple Acquires Credit Kudos, UK Data Tool for Lenders

Apple may have a big cash cushion to lend from — but my guess is that it’s probably not enthusiastic about losing a pile of money to the Pay Later experiment, so it will likely proceed with caution. It’s where the decision to go it alone could get a little tricky, especially as the market for credit tightens and consumers feel the inflationary pinch even more — and turn to credit to alleviate those pressure points.

We already see that happening.

The number of credit card revolvers is reportedly back to 2019 levels as consumers spend down their savings and put more of their expenses on cards than they are able to repay with their monthly cash flow.

Read more: More Consumers Letting Card Debt Revolve, Incur Interest

Of particular concern to Apple might be Pay Later’s $1000 spending cap — it could turn off iPhone users who are generally a good credit risk and might be willing to give Apple Pay Later a try. It could also attract those who might not be on such solid financial footing, and for which Apple has little experience underwriting.

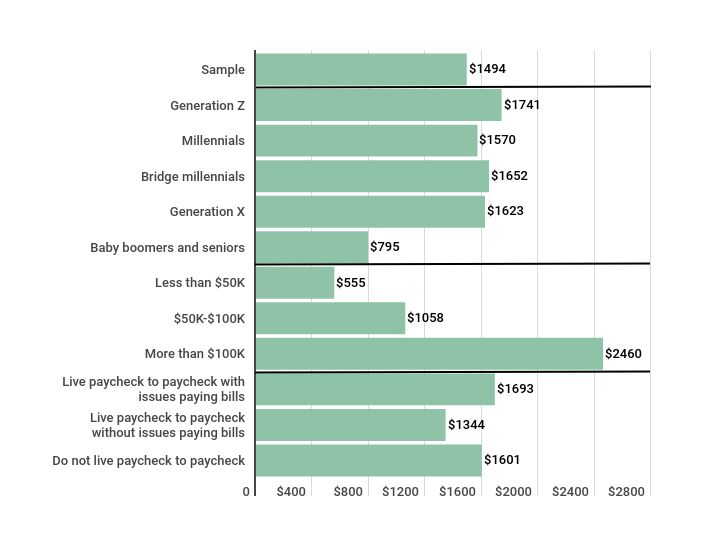

According to PYMNTS May 2022 BNPL research, roughly 8% of all online BNPL users earn more than $100,000 a year and use installments as a way to manage payments for higher-end purchases that average $2,460.

Average BNPL purchase ticket, by demographics

Source: PYMNTS.com. Average amount spent in the most recent retail purchase using BNPL, by demographics Location: United States. 1,353 respondents Referenced Timeframe: 2022-05

Nearly 16% of online Apple Pay users earn more than $100,000 a year — the initial Pay Later proposition isn’t relevant for their high-end purchases.

The BNPL users who fall within the current Pay Later lending limits and who have also used Apple Pay online fall into a different camp. They are largely lower income (earning less than $50,000) Gen Zs and middle- to upper-middle-income millennials ($50,000 to $100,000 a year) who also say they live paycheck to paycheck. Their online retail BNPL purchases average $555 and $1,064, respectively.

The Pay Later Point-of-Sale Pivot

At launch, Apple Pay Later is unavailable for use at the physical point of sale, where most retail purchases are still made. This is probably for two good reasons.

The first is that Apple Pay, overall, has been a real bust in-store.

Pay Later’s September 2022 launch date coincides with the eighth anniversary of the launch of the “groundbreaking” payment alternative to plastic cards Apple execs said Apple Pay would become in-store.

See also: Apple Pay At 7: Big Fish In A Small And Shrinking In-Store Mobile Wallet Pond

PYMNTS has been tracking Apple Pay adoption and usage in store consistently and methodically since it launched in 2014. Nearly eight years later, the best thing anyone can say is that Apple Pay’s growth in-store is stagnant.

Read more: Apple Pay Adoption Stats

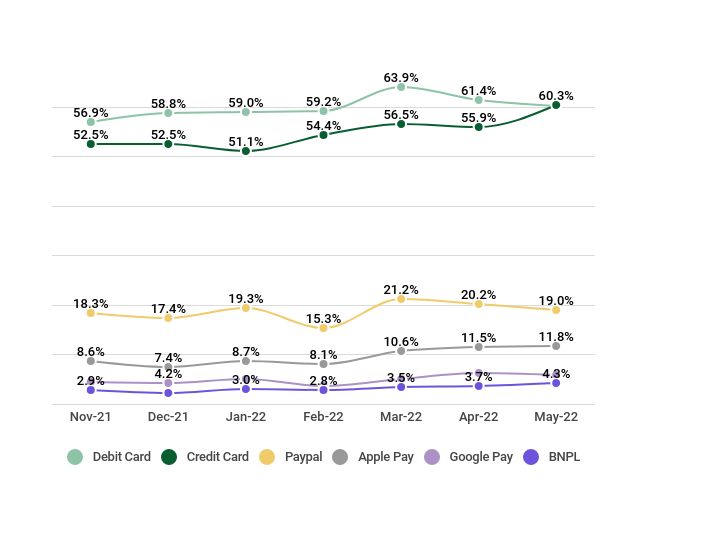

Ninety-four percent of Apple Pay users who could use Apple Pay to make a purchase — meaning they have an iPhone and are in a store that accepts it — don’t.

According to PYMNTS’ May 2022 Consumer Digital Payments Study, 37 times more consumers used debit cards, 29 times more consumers used credit cards and about twice as many consumers used PayPal instead of Apple Pay to make a retail purchase in the store in the last 30 days.

Payment method usage for in-store purchases

Source: PYMNTS.com. Share of consumers citing to have used select payment method for in-store purchases on the last 30 days Location: United States. 2,200 respondents monthly Referenced Timeframe: 2021-11 to 2022-05

Read the study: Digital Economy Payments: How Consumers Pay In The Digital World

The second likely reason is the current kerfuffle over Apple’s refusal to open their NFC chip to rivals, in particular PayPal. Activating Pay Later at the point of sale would likely throw gasoline on that regulatory fire, since PayPal’s inability to use the NFC chip on iPhones for in-store purchases would now include its own competitive BNPL products.

Giving up in-store for Pay Later isn’t really giving up that much, all things considered.

Apple is placing its Pay Later bets online and in-app, hoping that it will give Apple Pay the spark it was never able to get in-store.

It’s not entirely clear that will work.

The Pay Later Market

To start, Apple Pay’s total addressable market is the 51% of U.S. consumers with iPhones who use them to make retail purchases online and in-app. That then gets divided by the fraction of sites that accept Apple Pay for payment and the fraction of iPhone users who use (or want to use) Apple Pay to checkout.

That makes Pay Later’s addressable market the credit-worthy fraction of the fraction (iPhone users) of the fraction (who want to use Apple Pay to make a purchase) of the fraction (where Apple Pay is available for iPhone users who want to use Apple Pay) of consumers eligible to use Pay Later as a payment option.

Minus the big fraction of consumers who shop at Amazon and Walmart/Sam’s Club, where Apple Pay isn’t accepted.

According to the latest PYMNTS Amazon/Walmart retail and consumer spending data, Amazon now captures 3.4 percent of all consumer spend in the U.S., and just about half of online sales. Walmart has 2.8 percent of consumer spend.

Read further: The Walmart/Amazon Whole Paycheck Matchup

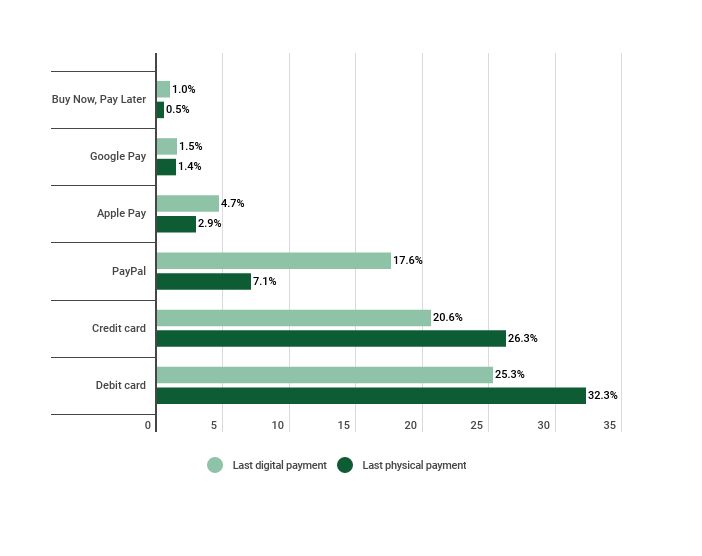

According to PYMNTS’ May monthly Digital Payments study, 1.1 percent of consumers used Apple Pay to make their last online retail purchase, compared to 26.8% who used debit cards, 42.8% who used credit cards, and 12.2% who used PayPal. According to PYMNTS data, more consumers used BNPL options (1.9%) than Apple Pay to make an online retail purchase in May.

Share of transactions, by payment method

Source: PYMNTS.com.

Share of consumers citing to have used select payment method in their last purchase

Location: United States. 2,659 respondents

Referenced Timeframe: 2022-05

See the study: 19M More Consumers Went Online to Bank, Buy and Pay Bills in May 2022

Then there’s the in-app opportunity.

Similarweb ranks Shein, Amazon and Walmart as the three most downloaded shopping apps. Only Shein enables Apple Pay — in addition to PayPal, Klarna, Afterpay and Zip, and not in that order on the checkout page.

Both Amazon and Walmart enable BNPL through their partnerships with Affirm, Amazon exclusively with Affirm. Walmart enables PayPal online and in-app (and with it Pay in 4). Amazon is currently working with PayPal to enable Venmo cards as a registered credential in the Amazon Pay wallet.

That’s a pretty big chunk of the online and in-app retail market for which Pay Later isn’t even an option.

In other words, Apple Pay Later can’t be used at any of the physical places where people can now use other BNPL alternatives, and it can’t be used at a big swath of of the online and in-app places that drive retail spend and where people can now use other BNPL alternatives. Where it can be used, it may be one of many installment payment choices, and those other choices may be more familiar to customers who have encountered and used them at most of the other places they shop.

This begs the obvious question: Why would someone who likes using BNPL opt to use Apple Pay Later rather than one of the BNPL options that has wider acceptance and they’ve probably already tried and used?

That makes Apple’s current challenge quite similar to what it faced in-store eight years ago: convince iPhone users, who don’t use Apple Pay very much today, that Pay Later is a better alternative than what they’re using now at the places that accept Apple Pay today.

That may not be easy.

A not-yet-released PYMNTS study conducted in May 2022 of 1353 U.S. BNPL users finds that 79% of current BNPL consumers plan to continue using a BNPL option for retail purchases in the next 90 days, and 40% of them say they will plan their shopping around their ability to use BNPL to pay.

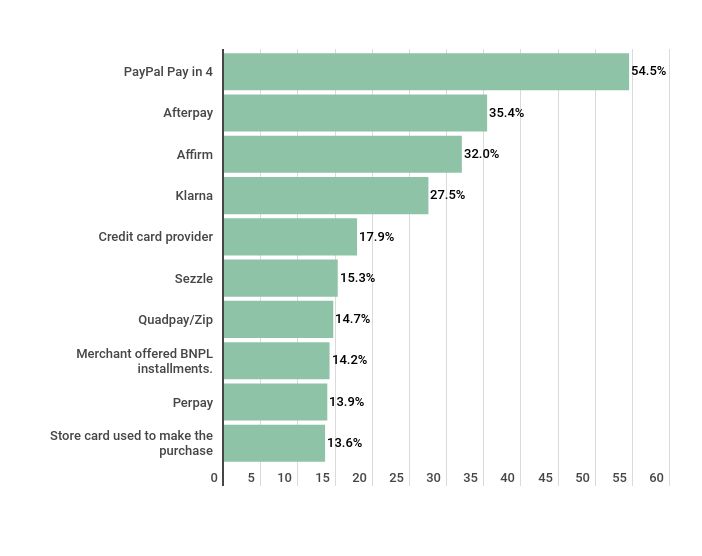

According to this same study, PayPal (at 55%), Afterpay (at 35%), Affirm (at 32%) and Klarna (at 28%) and bank-issued credit cards (at 18%) were the providers cited by BNPL users as those they use to make online retail purchases.

Most popular BNPL providers for online purchases

Source: PYMNTS.com.

Share of BNPL users citing to have used select providers to make a BNPL purchase in the last 3 months

Location: United States. 624 respondents

Referenced Timeframe: 2022-05

Could Apple, with Pay Later, find its edge in-app, a channel that is increasing in importance and usage? In May of 2022, PYMNTS finds that almost as many consumers made their last retail purchase using websites (15.4%) as in-app (14.7%)

Apple ID is the credential used by iPhone users to access all of Apple’s services, including the apps in its App Store. My experience is that the apps that use Apple ID facial scan to open present two checkout options: Apple Pay and the generic checkout button. As more apps enable that option for the convenience of the consumer, it could create more of an in-your-face incentive for in-app users to give it a try.

That could also raise a few eyebrows.

Which brings me to the Pay Later Pandora’s box that Apple may have just opened.

The Big Questions

The Pay Later announcement, at best, suggests it’s little more than an experiment for Apple to dip its toe in the very popular BNPL waters.

As it does, it could alienate all of the issuers whose cards are provisioned in their wallet today — who never really liked having to pay the Apple Pay tax in the first place — all of whom have their own BNPL plans.

It will also do little to endear themselves to the FinTechs, including Afterpay and Affirm, whose virtual cards are and can be added to the Apple Pay wallet for payment online, in-app and in-store.

Diving into BNPL also means getting access to the invitation-only CFPB’s BNPL club as they aggressively dig into the area. It will be interesting to see their reaction to Apple Pay’s BNPL entrance, especially given that it’s Big Tech’s first foray into the consumer lending space.

Related: CFPB’s New Rules for BNPL Could Come by Year’s End

This is the same CFPB that is also concerned about how Big Tech uses consumer data. It’s possible they will have more questions about how Pay Later will use the Apple ID data to provide services to Apple Pay users

Another question is whether the same Big Tech “self-preferencing” prohibitions in the EU, which are also present in Sen. Klobuchar’s proposed antitrust legislation, could extend to financial services products, including Pay Later. Regardless, that could limit how Apple decides to incent iPhone users to try Pay Later, and how Pay Later presents itself inside of the apps in the App Store.

Pay Later is also launching at exactly the point in time that the market is literally eviscerating BNPL FinTechs over concerns that their business models weren’t engineered for an economic downturn and high interest rates: a reasonable concern. That’s even as BNPL FinTechs have years — some more than a decade — of experience lending to their millions of customers. Apple has the balance sheet to buffer losses and few concerns over whether it can access capital to lend, but it will have to balance its tolerance for risk with the potential to to alienate good customers who can’t use the service or are denied loans as it gets its credit risk sea legs under them.

The Last Word

I wrote in April that Apple’s Project Breakout likely launched many Project Breakouts across the payments and consumer lending landscape. It’s probably not a coincidence that we’ve seen the pace of issuer-centric BNPL innovations accelerate over the last several months.

See also: The One Big Thing Apple’s Project Breakout Needs but Doesn’t Have

Apple may believe that Pay Later could ignite Apple Pay — the same way that it appeared to believe that a slick iPhone app was enough to ignite Apple Pay in 2014 at the point of sale.

Then as now, it’s facing the same headwinds that even Apple can’t control: A red ocean of other installment payment alternatives that people can use in lots of places and no compelling reason why people should use a new one that they can’t.