Paying for purchases in installments is a classic concept in retail, with legacy offerings such as Christmas layaway plans helping consumers manage their spending for decades. Modern iterations, such as credit card installments and buy now, pay later (BNPL) plans, are for every season.

Paying for purchases in installments is a classic concept in retail, with legacy offerings such as Christmas layaway plans helping consumers manage their spending for decades. Modern iterations, such as credit card installments and buy now, pay later (BNPL) plans, are for every season.

Consumer use of BNPL and credit card installment plans has risen in recent years as price increases and economic uncertainty have increased the value of financial tools that help consumers manage cash flows. Many retailers and credit card issuers offer installment plans, which can come with rewards programs, high credit limits and ubiquitous in-store availability. BNPL has emerged as a credit alternative, serving consumers who cannot qualify for a credit card or those seeking the lowest possible interest rates.

These are some of the findings detailed in “Tracking the Digital Payments Takeover: What BNPL Needs to Win Wider Adoption,” a PYMNTS and AWS collaboration. This report examines consumer interest in deferred payment plans, including credit card installment plans and BNPL. We surveyed a census-balanced panel of 3,140 consumers in the United States between June 13 and June 21 to discover what features they expect from deferred payment plans and to learn how BNPL can meet these expectations and reach the usage rates of credit card installment plans.

Other key findings from our study include:

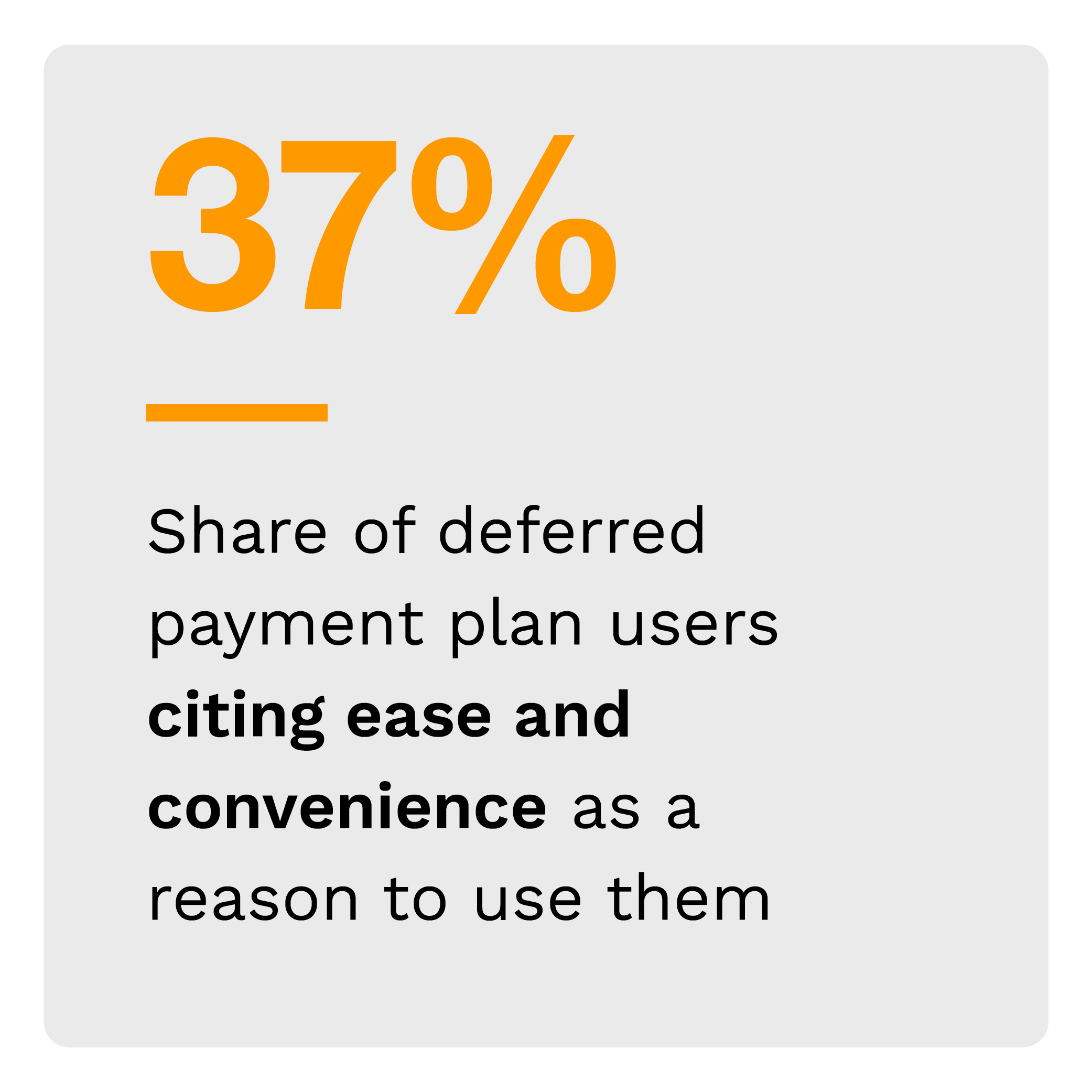

Consumers using deferred payment plans want BNPL options as easy and convenient as credit card installments.

PYMNTS’ research finds that 28% of consumers have used deferred payment plans such as BNPL or credit card installments in the last three months. Consumers report using deferred payment plans for three reasons: The plans are convenient, provide a financial cushion and enable them to buy more. Consumers expect to access these features from BNPL as much as credit card installment plans.

Consumers pay for all types of products with deferred payment plans, with BNPL slightly behind credit card installment usage across all product types.

Deferred payment plans have been normalized for all types of purchases — and BNPL usage is generally a bit behind credit card installments. PYMNTS’ data finds that 67% of consumers used credit card installment plans to finance grocery purchases in the last three months, and 56% did the same with BNPL. We found similar trends for other product categories as well.

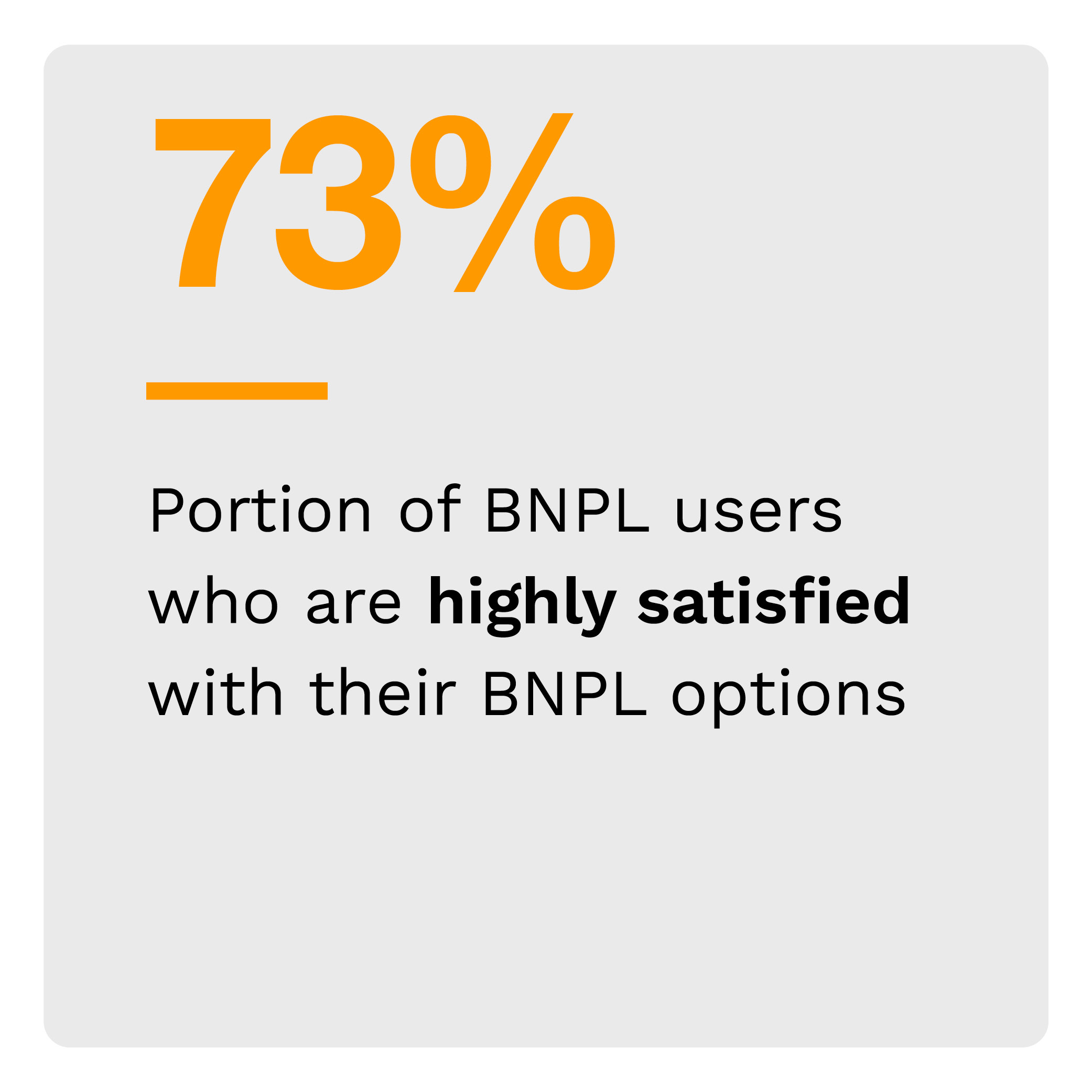

Consumers who use BNPL are highly satisfied with their BNPL options and are increasing their use of BNPL.

Three-quarters of BNPL users are very or extremely satisfied with their BNPL options, and this trend does not vary significantly by provider. Low-income and younger consumers are less likely to be highly satisfied with their BNPL options, however. This contrasts with millennials and higher-income consumers, who are largely satisfied with their options.

Our data shows that these consumers want the advantages that credit card installment plans can offer. However, to reach new customers and fully unlock BNPL’s retail potential, providers must meet consumer demands for wide availability, reward programs and higher credit limits. Download the report to learn more about how consumers are using installment payment plans.

See More In:

Amazon Web Services, AWS, BNPL, buy now pay later, credit cards, Digital Payments, Finance, financing, installment payments, Main Feature, News, PYMNTS News, PYMNTS Study, Retail, rewards programs, shopping, Tracking the Digital Payments Takeover