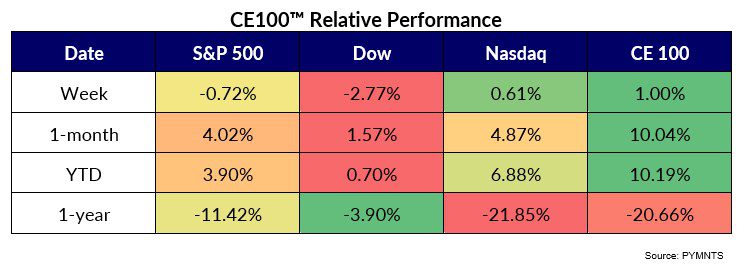

Despite concerns over consumer spending, PYMNTS’ ConnectedEconomy “CE 100” Stock Index gained ground this past week, as it extended its recent run with another 1% weekly advance.

And thus far, year to date, the Index is up 10%, boosted a bit this time around by gains in the “Eat” segment, which surged 3.9%. DoorDash led the segment higher, up nearly 11%.

Starbucks is expanding its U.S. delivery presence, and will be nationwide through DoorDash later this year.

The move, PYMNTS noted, suggests that exclusive partnerships with delivery providers may not make sense anymore for major QSR brands as demand for on-demand options grows across the industry, and especially as PYMNTS data show that 43% order food for same-day delivery from aggregators every month. Domino’s trailed DoorDash’s performance in the “Eats” pantheon with a 3% rally.

Pay and Be Paid Names Pay Off

Payments-focused names also swung to the upside this past week, led by Sezzle, which was up 19.8% and followed by Affirm, which gathered 11%. Those share price increases helped move the “pay and be paid” pillar 2.9% higher.

As reported headed into the new year, Sezzle is now offering its credit-building service Sezzle Up in Canada. Sezzle Up now enables users of Sezzle’s buy now, pay later (BNPL) solution in Canada to opt in to report their payment behavior to credit reporting agencies, which in turn helps users build their credit.

As PYMNTS data has shown, the use of — and interest in — BNPL is growing, which also means that competition is growing, too. BNPL plans from FinTechs such as Klarna and Affirm are gaining popularity as shoppers seek alternative financing to avoid rising credit card interest rates. As for the competitive landscape, PYMNTS research has found that 70% of current BNPL users say they would be interested in BNPL plans offered by their banks.

Slight Gains for the Banking Group

Separately, the banking vertical gained 1.1%, in a week that digested earnings from J.P. Morgan and Citi (down 5.5% and up 2.3%, respectively).

J.P. Morgan’s results showed that, at least for the moment, consumer spending seems resilient, as credit and debit sales volume was up 9% in the quarter, year over year, to $411 billion. Overall, credit card loans were $185 billion, up 9% from the third quarter, indicating at least some appetite (and room) for U.S. households to take on more debt. Citi’s own results showed double digit revenue growth from card spending.

Ally Financial helped boost the sector’s performance, soaring 16%. The bank and automobile loan provider posted results that showed auto net charge-offs rising, but where reserves are, as reported by The Wall Street Journal, enough to cover those losses and where loan yields are rising on the heels of higher interest rates.

Those performances helped offset the slide seen this past week in Goldman Sachs shares. The investment bank — which has seen headwinds in its main street push — saw its shares lose 8.6%.

Goldman Sach’s struggles in consumer lending and cards were detailed in the company’s latest earnings report. The company’s loan book grew — Goldman reported $6 billion in installment loans in the fourth quarter ending Dec. 31, up from $4 billion a year ago. Goldman also reported $16 billion in credit card loans, up from $8 billion in Q4 2021.

But at the same time, the company said its fourth quarter provision for credit losses was $972 million, reflecting provisions related to the credit card and point-of-sale loan portfolios — and said that its Consumer net charge-off rate stood at 2.8%, up 0.5% year on year. The company is seeking to scale its Platform Solutions business toward profitability. As PYMNTS reported, Platform Solutions lost $1 billion in 2021 and $783 million in 2020.

And in news reported at the end of the week, The Federal Reserve is reporting investigating Goldman Sachs’ consumer business, Marcus. The Fed is reportedly looking into the bank’s oversight of the consumer business, its management and governance, and its handling of customers’ problems.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More