The stressors mount. The savings dwindle. The credit cards offer only slight respite. And there’s not enough on hand to meet the unexpected curveballs life throws, inevitably.

Especially not for the paycheck-to-paycheck consumer.

Readers of this space are no doubt familiar with the fact that a majority of us — now at more than 60% of the adult population in the United States — live paycheck to paycheck. Defined simply, that means all the money that comes in leaves to cover the bills. And there’s nothing left over once the bills are paid.

Not an easy way to live, and downright precarious for significant swathes of the population. Sixty-three percent of the population lives paycheck to paycheck, as PYMNTS’ most recent data show; which is up about 16% year on year, as measured in May. And 23% of consumers say they struggle to pay their monthly bills.

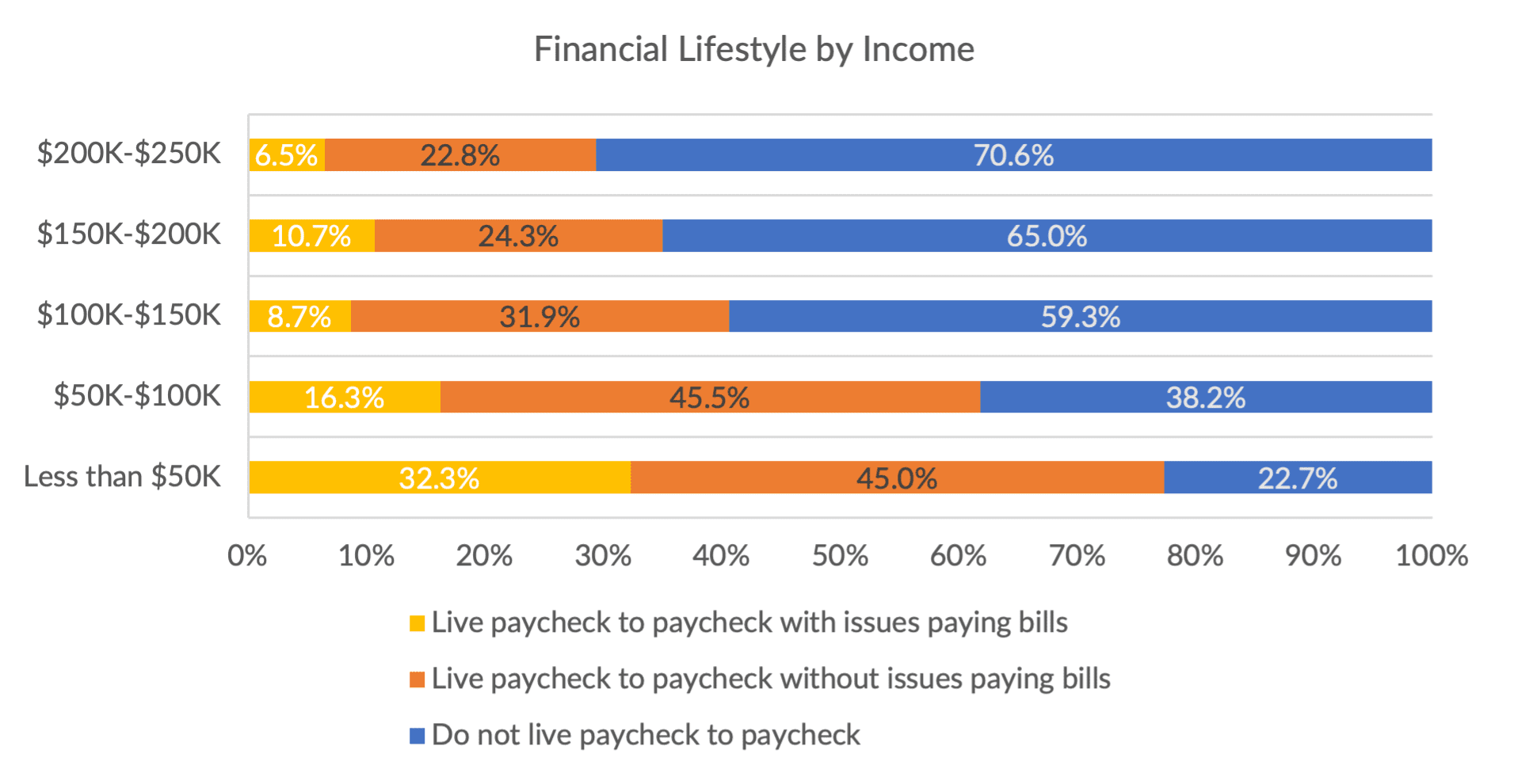

Drill down a bit and the straits become a bit dire depending on income. For those earning less than $50K annually, 32% live paycheck to paycheck with issues paying the bills — a designation that gets narrower the higher the income level.

But it never goes away.

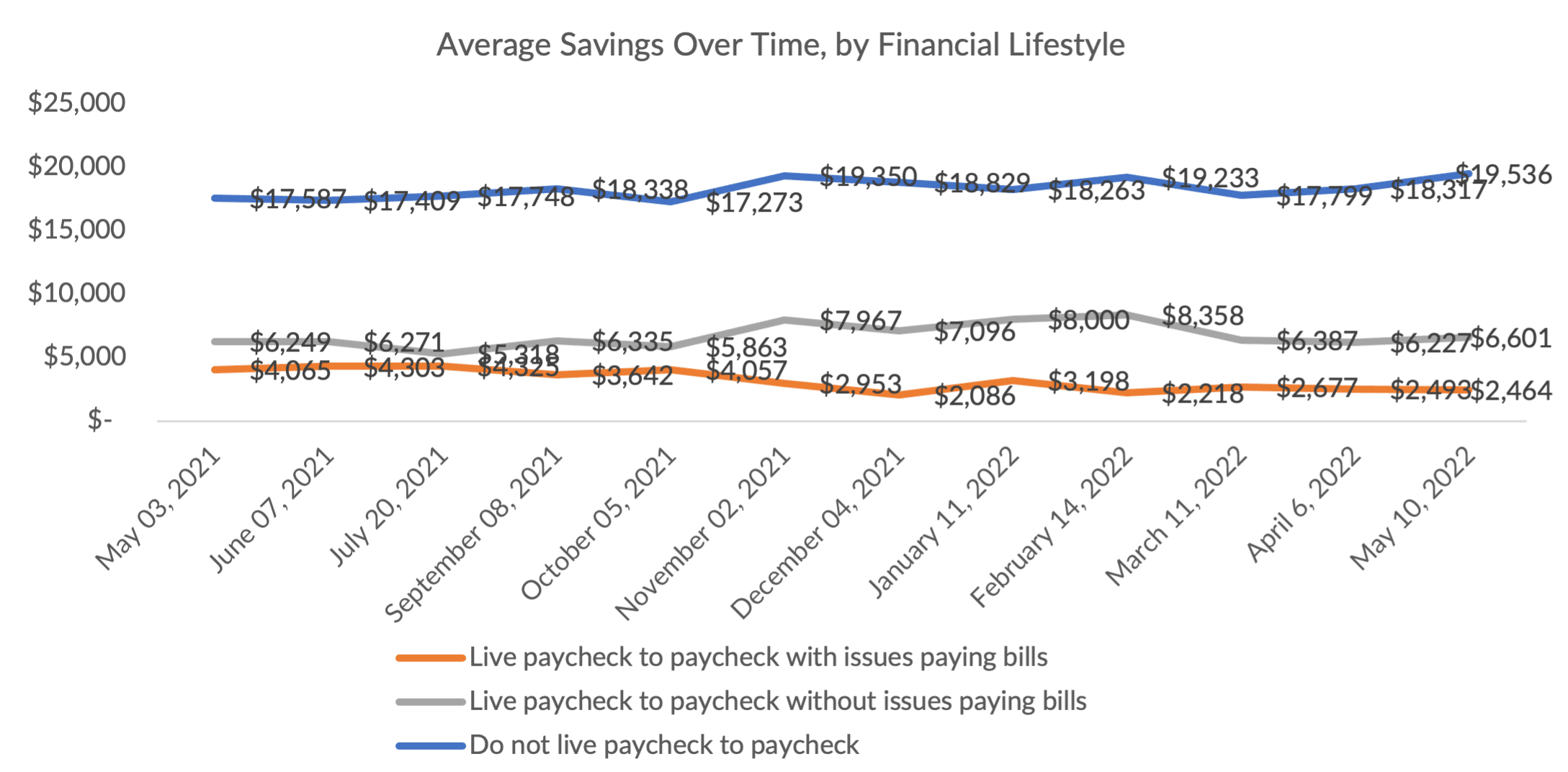

It stands to reason that at least some of the people who are struggling to navigate daily financial life would see some drawdown of the money in the bank accumulated during the pandemic. For the P2P denizens who have issues paying the bills, the depletion is significant: The chart below shows that the current savings is $2,464, down from a peak of more than $4,000.

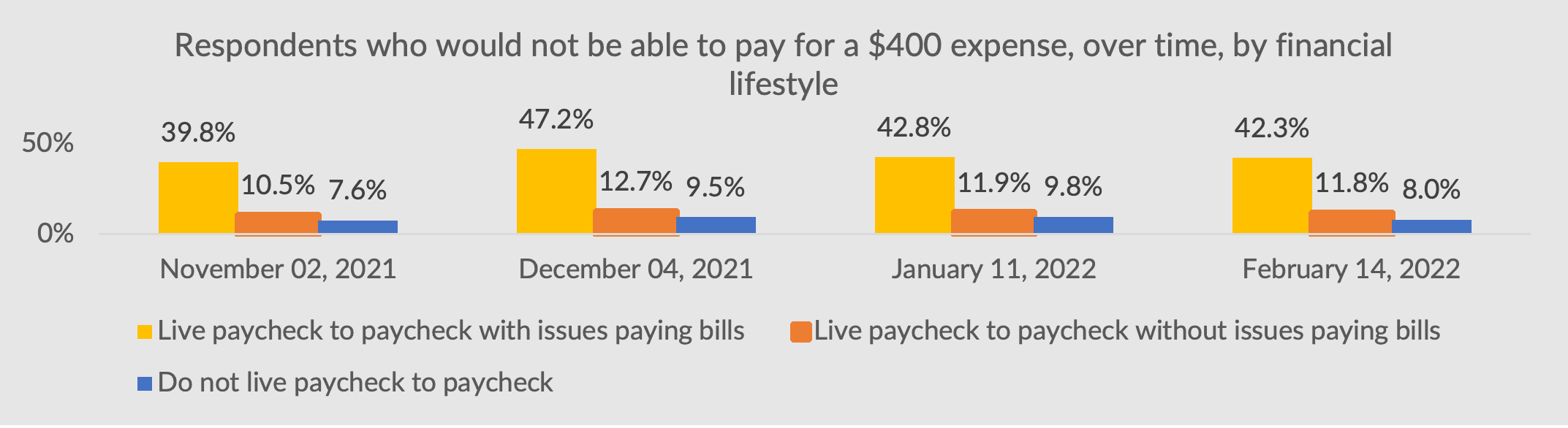

And so, that means too, that as cash slips a bit, the cushions that insulate us from the shocks of life are less, well, inflated than they might otherwise be. The percentage of relatively pressured respondents that would not be able to afford a $400 emergency expense translates to 42% of P2P consumers who have issues paying the bills, up from 40% less than a year ago. Clearly the headwinds are mounting (though the trend is reversed with higher income cohorts), which will have ripple effects throughout the economy.