But as noted in a PYMNTS Intelligence research study on “How Credit Insecurity is Changing U.S. Consumers’ Borrowing Habits,” millions of consumers still lack access to this key financial resource as of April this year.

Findings detailed in the joint PYMNTS-Sezzle study shows that about 80 million U.S. consumers, about one-third of the country, are credit insecure — individuals who lack reliable credit access.

Among these credit-insecure consumers, about 25% or an estimated 63.5 million are credit marginalized — individuals who got turned down for credit at least once in the past year, usually because their credit score took a hit or there was a change in their financial situation.

Drilling down into the data reveals that millennials (nearly 47%) and men (61%) make up the majority of this cohort, who are also more prone to having overdue payments on payday loans and high-interest credit builder loans, adding another layer of complexity to their financial struggles.

Bridge millennials — a demographic that encompasses the older millennials and the youngest individuals from Generation X — are next in line, accounting for about 35% of credit-marginalized consumers.

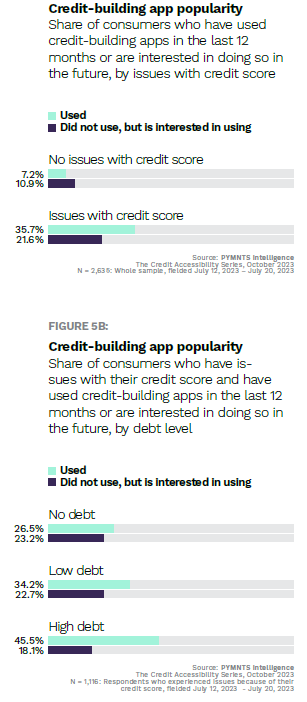

BNPL, Credit-Building Apps and Financial Education

To navigate the challenges posed by the current economic landscape, both credit-insecure and credit-marginalized consumers are embracing various strategies to adapt and thrive.

For the majority of U.S. consumers who do not have a good understanding of how credit scores work or how they can be improved to quality for credit products, BNPL emerges as a transformative tool that can help turn their credit situation around. “A better understanding of how credit works could enable credit-insecure consumers to access safer tools to cope with financial strain and even reverse some of the negative credit spiraling that is so common,” per the report.

However, the fact that only 23% of consumers with low credit scores reported using BNPL and less than 20% used it specifically to improve their credit scores underscores a knowledge gap. Bridging this gap will require improved education and heightened awareness among consumers with low credit scores regarding the potential advantages of using credit products to boost their credit status.

FinTechs and financial product vendors must lead the charge, per the study, exploring effective ways to connect with consumers having low credit scores with user-friendly materials and education on credit building to ease their path to financial stability.

Credit-building applications can also be a useful tool to help consumers tackle mounting debt, improve their financial management skills and credit scores. According to data published in another research study by PYMNTS, nearly 50% of high-debt consumers facing credit score issues have already embraced this tool in the past year, compared to only 7% of consumers without such issues.

Overall, boosting credit scores has significant financial benefits for consumers. Separate research from PYMNTS shows that individual with scores of 579 or less — known as deep subprime credit scores — who can increase their scores to the near-prime range of 620 to 659 can finance an extra $44,000 in purchases and cut interest rates by as much as 24%.